As it happens, there were no discernible hurricane effects in the durable goods release, and the data were uniformly positive. Headline durable goods orders data registered a 2.2% increase in September on top of a +0.1% revision to August. Net of the volatile transportation equipment sector, orders for other durable goods were up 0.7% in September on top of a +0.2% revision to August.

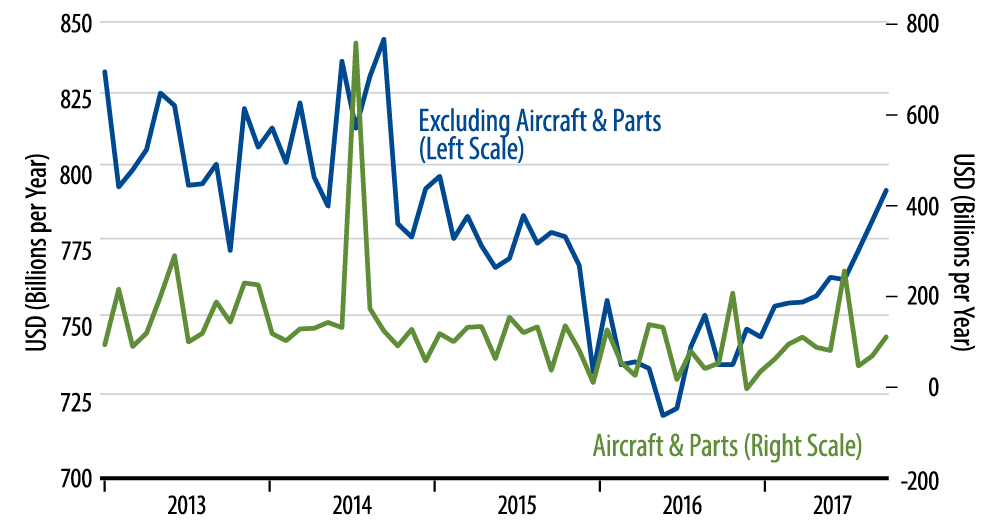

These gains were largely driven by continued improvement in capital spending. Orders for nondefense capital goods excluding aircraft rose 1.3% in September, with a +0.1% revision to August. The accompanying chart shows recent behavior for capital goods orders. Capital goods orders have been on the rise since the middle of 2016, and, if anything, the gains have picked up speed in recent months.

(Meanwhile, you can also see in the chart that the outsized gains in aircraft orders—up 63.5% non-annualized in September—are merely a continuation of random month-to-month swings in this aggregate, which is why we exclude it from durable goods and capital goods data, in order to get a less distorted read.)

In last week’s comments, we were downbeat about the manufacturing sector in general. While factory activity has improved this year, the gains had ebbed in the months leading up to the hurricanes, and even the prior, stronger gains in manufacturing were driven largely by strong capital spending and inventories, and the inventory gains are likely ephemeral. In sum, we were skeptical as to how long capital spending could single-handedly drive manufacturing higher.

Well, the September data certainly indicate that the capital spending upsurge has not flamed out yet. Meanwhile, note that for all the recent gains, capital orders levels are merely back to where they were two years ago. This observation could break either way. There may be lots of potential for further gains in CAPEX, or it may be that now that we have re-attained late-2015 levels, CAPEX goes flat from here. The outcome of this issue will be a prime driver of the state of the US economy going forward.