The pundits we’ve heard this morning are emphasizing the upward revisions to August and dismissing the soft September gains as hurricane-related. Fair enough. However, a month ago, August’s job gains were nice, but there were much bigger downward revisions to July than the upward revisions announced today for August. And we didn’t hear any mention of revisions a month ago, either.

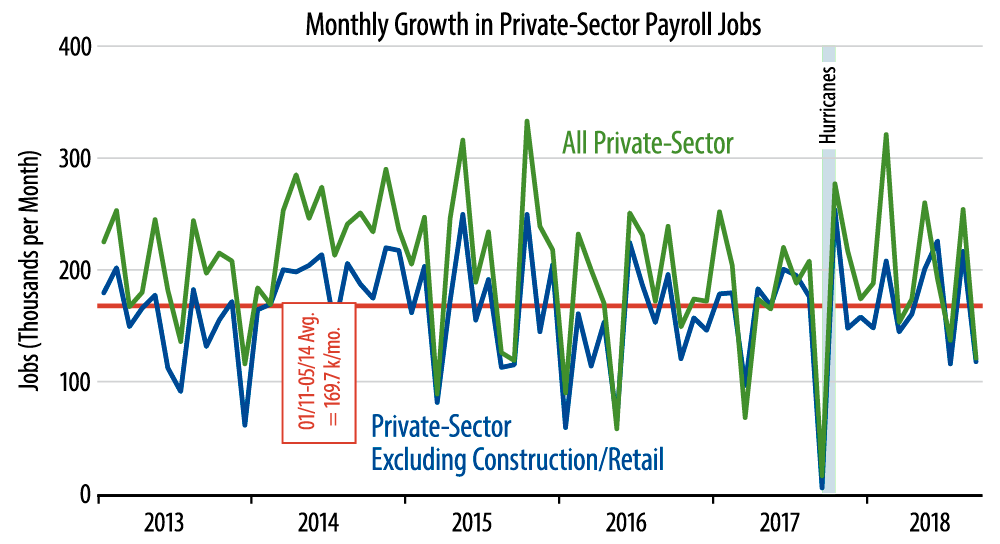

As for the supposed hurricane effects, the Bureau of Labor Statistics’ (BLS) comments on the jobs data this morning stated that while Hurricane Florence did indeed occur "during the September reference period...response rates...were within normal ranges." In other words, no clear evidence of hurricane effects. Meanwhile, look at the September data in the chart.

September 2018 job growth, while relatively low, was not outside the range of monthly fluctuations seen over the past few years. In comparison, the hurricane effects in September 2017 were quite clear, as also marked in the chart, with jobs essentially unchanged in September 2017 from August and an October gain that made up for the extremely weak September print.

So, it is far from clear in the chart that there were noticeable hurricane effects. If there were, they would be offset with a much stronger October gain a month from now, and we can then adjust the story accordingly. In the meantime, we point out that market analysts have been quick to apply positive spin to these data, ignoring the downward revisions a month ago, instead fixating on upward revisions this month and asserting the existence of hurricane effects on the September 2018 data when BLS commentary and visual inspection fail to indicate such.

No, the economy is not faltering. However, as we’ve stated here before, with construction sectors stalling, service sectors slowing, and manufacturing growing nicely but steadily, we just don’t see the acceleration in economic activity that the bond bears assert is occurring.