2014年10月3日時点

In our business, a 250,000 monthly job gain is terrific, a 200,000 gain is so-so, and a 150,000 number is weak, so the markets are understandably upbeat about the 248,000 increase announced today. But notice that the markets wax and wane over swings in the data on the order of 50,000 per month. The level of payroll jobs is 130 million, so the market’s threshold of excitement amounts to changes on the order of 0.036% per month.

By way of perspective, the US Census Bureau professes measurement error in its housing data of ±1.5% per month. While the Bureau of Labor Statistics does not announce any measurement-error magnitude for its data, let’s assume it would be similar to those of the Census. The implication is that the markets are fomenting over changes that are about 1/40th the size of likely measurement error. Tempest in a teacup, anyone?

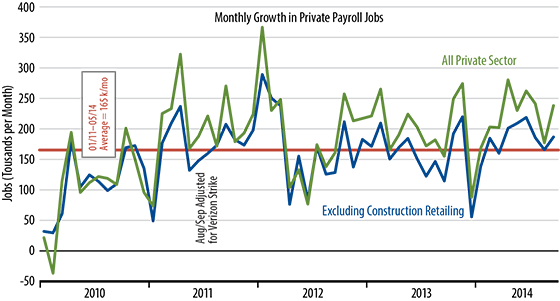

Sure, we track the monthly data, just like everyone else, but we try not to get too excited about any one month's numbers. Looking at the totality of recent years' data, as per the accompanying chart, the picture looks like one of largely steady job growth. This month's numbers looked better and last month's numbers looked not as good, but nothing we have seen this year looks demonstrably different from the fluctuations of the last four years.

So, there is no hard evidence indicating that the underlying pace of job growth has recently accelerated, in which case, there is no support from these data for the contention that the pace of economic growth has recently picked up. The remaining question is whether the underlying pace of job growth-220,000 to 225,000 per month-represents a poor, mediocre, or favorable rate of growth.

Our fallback indicator for this question is the employment rate: the civilian adult employment-to-population ratio. This ratio held steady in September at 59.0%, the same level as the last four months. It is up from 58.6% at the end of 2013, but still lower than the 59.4% rate in place at the June 2009 trough of the 2007-09 recession and far below the 62.7% rate in place at the outset of the recession. So, there is some underlying improvement in the labor markets taking place, but we have a long ways to go yet. If anything, Federal Reserve Chair Yellen is understating the economy’s need for further improvement in the labor markets..