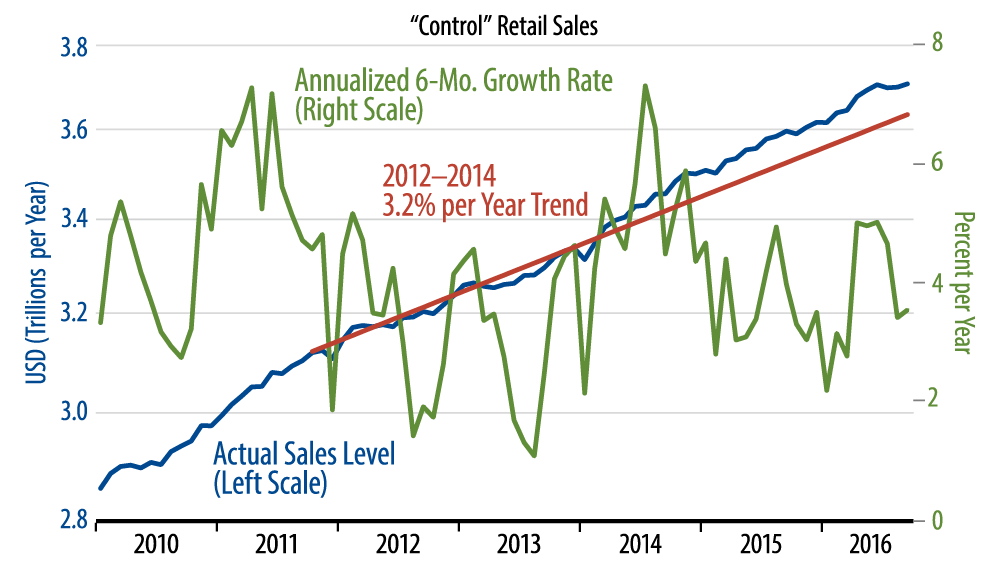

Our “control” measure, sales excluding vehicles, building materials and gasoline, rose a tepid 0.2%, with a 0.1% downward revision to August. This was better than the -0.2% and 0.0% changes for July and August, respectively, but not by much. For 3Q16 over 2Q16, control sales showed 1.1% annualized growth, compared with 3.1% growth over the past 12 months.

In 2Q16, the economy grew weakly (1.4% real GDP) despite strong gains in consumer spending. In 3Q16, consumer spending gains were much more modest, and we believe overall GDP growth will be similarly soft. Softer consumer spending growth will likely be partially offset by better vehicle production and less of a drag on inventories, but capital spending and construction activity looked to have declined in 3Q16, and most other indicators looked softer than in 2Q16.

Within store groups, September sales were weakest at department stores and electronics/appliance stores. Gains at furniture, building material, apparel, grocery and book stores served only to offset or partially offset declines in preceding months. Nonstore (online) retailers showed further sales growth, but even here, growth over the last four months has been at only a 3.1% annualized rate, after this sector enjoyed 20.5% annualized growth over the first five months of the year. Retail sales of motor vehicles continued to inch up, but here too, sales growth was slower than previously (2.6% annualized growth year-to-date, compared with 6.7% growth in 2015).

All in all, the consumer is holding in relatively well, but there is no sign of the spark that some expected would drive an economic growth rebound in second half 2016.