2014年10月30日時点

Most of the data underlying the GDP estimates are available ahead of time, so only rarely does the actual release of GDP surprise us. Today’s news of 3.5% 3Q14 growth was somewhat above expectations and slightly above our own forecast of 3.2% growth. The details within the report, rather than the headline number, were the real surprise.

Expectations were for tepid growth in consumer spending and strong growth in business equipment investment, foreign trade, and motor vehicle output, moderated by a slight decline in inventory investment. We indeed got tepid growth in consumer spending (up at a 1.6% annual rate excluding vehicles) and strong gains in vehicle output (up at a 22.4% rate) and foreign trade (exports up at a 10.3% rate).

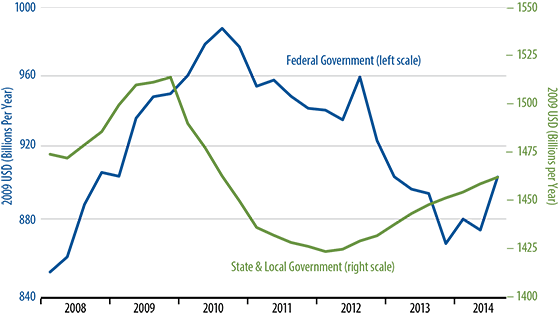

However, equipment investment grew at only a 7.7% rate, about half of what was expected. The really big surprises were gigantic increases in government purchases of services opposite a larger-than-expected decline in inventories. Federal government purchases of services rose at a 13.6% rate, after having declined steadily for the previous four years, and this component alone boosted 3Q14 growth by 0.7 percentage points. (See chart.)

Virtually all of those increases occurred in defense purchases, so the 3Q14 bulge there might be “September spending”: utilizing the appropriated budget before it disappears with the new fiscal year. It may also reflect the military ramping up outlays to cope with ISIS.

Looking ahead, while the conflict with ISIS continues, defense purchases are unlikely to rise as rapidly in the future as we saw in 3Q14. Similarly, 3Q14 auto production was boosted by an especially short model-year changeover, and the 3Q14 export gains also look tenuous, given worries over growth abroad and generally sluggish export trends prior to 3Q14.

As we all know, consumers account for most of GDP, and, again, growth there remains tepid. Average GDP growth for the year-to-date is exactly 2.0%. With more subdued data likely in 4Q14 for vehicles, exports, and defense purchases, it would not be surprising to see 4Q14 GDP growth come in around that average 2.0% rate.