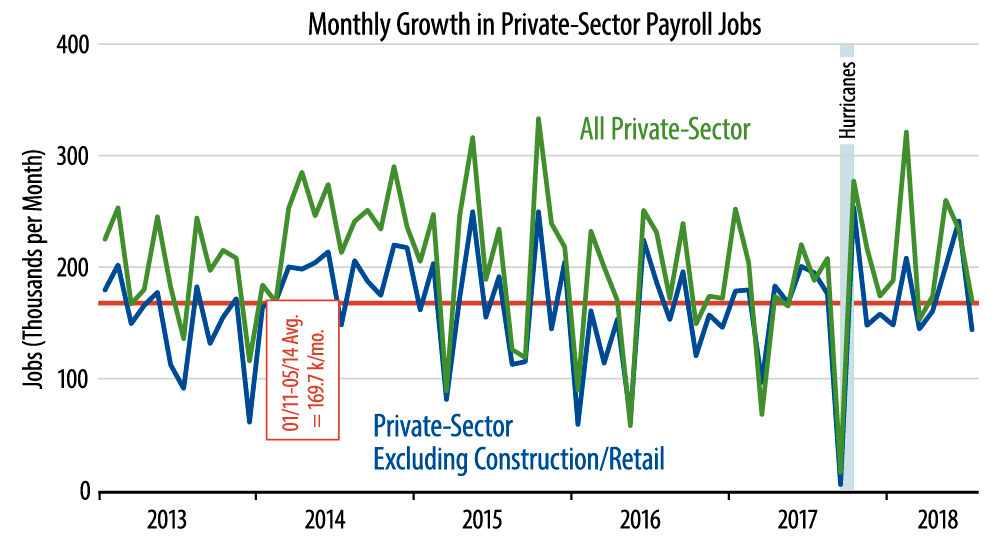

While other analysts have been extolling the low unemployment rate, our take has emphasized the fact that actual job growth has been slowing for most of the past two years. (How can the economy be accelerating when job growth is decelerating?) The July payroll data buttress that take, with job growth last month again back below the 2011-15 pace, after two above-average gains in May and June (see chart). Meanwhile, those bullish on the economy can focus on the admittedly strong May/June data. We’ll have to wait on the data for August and after to determine which is the trend going forward.

Meanwhile, wage data were similarly mixed, with hourly wages for all workers rising 0.26%, but wages for nonsupervisory workers up 0.13%, corresponding to annualized rates of increase of 3.2% and 1.6%, respectively. We have always paid more attention to the latter measure, arguing that it is nonsupervisory workers that actually get paid by the hour, whereas for the supervisory workers included in the all-worker measure, hourly wages are at best a guess. Still, there are differences of opinion here.

There is no debate about the fact that job growth has been strong in manufacturing, and that sector added another 37,000 jobs in July. July was the first month fully spanning trade war fears, and it appears that manufacturers generally were not concerned enough with those issues to cut back on hiring. Of course, the soft overall July job gains alongside strong factory gains indicate that service-sector job growth continues to slow.