How can a -17% drop be good news? When it was preceded by big upward revisions to previous data that brought January’s gain to +19.1% on top of a 10% upward revision to December’s level. It is as simple as that.

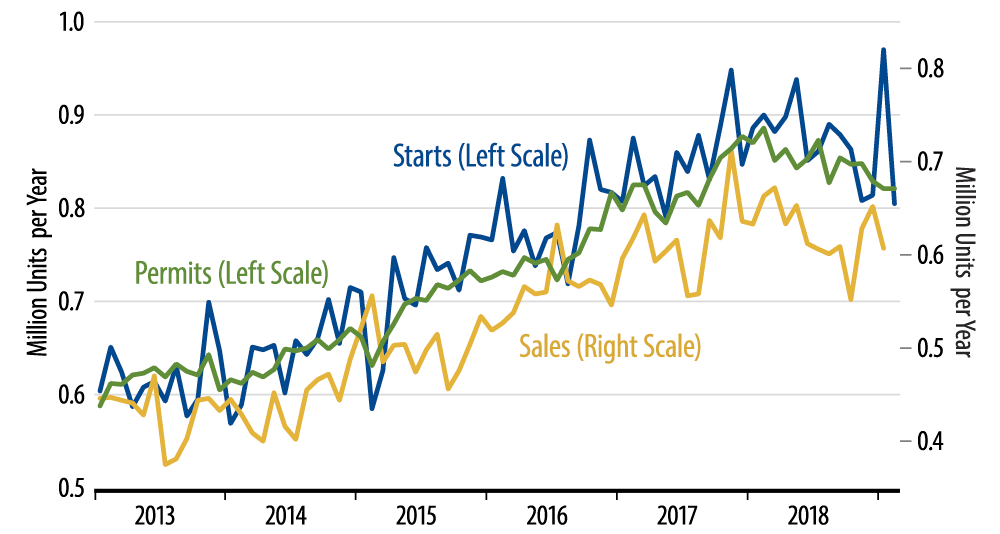

One look at the accompanying chart tells you most of what you need to know. Despite the sharp February decline, single-family starts look to be stabilizing, if anything, recently, after a year of declines. Average the last three months together, and you get a level well above where it looked like we were heading through the October and November data.

Remember, again, we have been tracking starts data that had been declining for a year. The relevant question for homebuilding was whether housing would drop off the table or stabilize, albeit at a level below those prevailing in 2017 and 2018. Our guess was the latter.

Other analysts have only lately noticed an inventory build-up in new single-family homes. We have been tracking that build-up for over two years. We thought it would result in homebuilders cutting back on construction rates to get housing supply back in line with housing demand. That has indeed happened.

However, as you can see from the sales line in the chart, underlying housing demand has held in pretty well even as builders have cut back over the last year. Once starts levels have dropped a bit more, to allow builders to finally reduce inventories—rather than merely slowing their growth—starts can stabilize and even bounce a bit.

In other words, we perceive homebuilding to be going through a necessary "correction" that will allow starts to stabilize later this year. The growth we saw through late-2017 was unsustainable, but that does NOT mean that housing is dropping off a cliff this year. Lower levels of homebuilding will indeed restrain GDP growth, but not so much as to threaten recession.

Six months ago, Street consensus overstated the strength of the economy as well as the Fed’s propensity for tightening. Presently, market sentiment has swung too far in the other direction. We don’t see an immediate threat of recession. If the Fed does ease this year, it will do so to prevent an inverted yield curve, not because of present weakness in the economy.