So, does today’s news move the needle for the consumer? Not really. Last month, we cautioned that as weak as the August news sounded, the underlying sales trends were still pretty steady. By the same token, even with the stronger news this morning, the underlying trends remain steady.

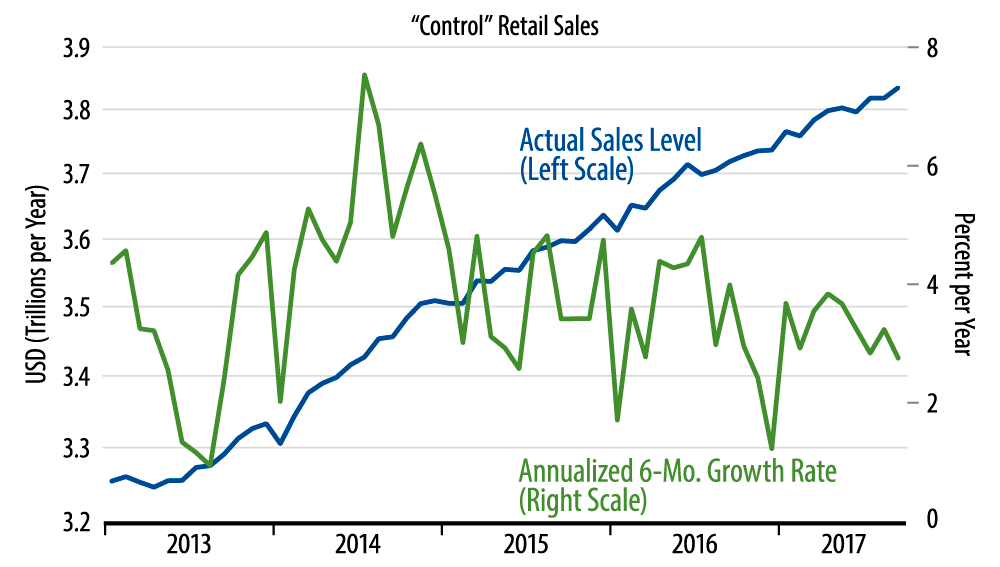

The August news suggested a possible, incipient softening trend. Today’s news proves that possible softening to have been a mirage, but it doesn’t point to any possible strengthening. As seen in the accompanying chart, sales levels (blue line) show no deviation from preceding trend lines, and underlying growth rates (green line) are down from where they were six or 12 months ago, but only slightly. Last month, our headline warned about being “fooled by randomness.” That admonition is just as relevant today, though in the opposite direction.

Car sales are the main reason that total sales rose more sharply than control sales. Sales at motor vehicle dealers rose 3.6% in September, but that followed a 2.1% decline in August. Average August and September vehicle sales together, and the result is 0.4% below July sales levels. In other words, the September vehicle sales gain merely offset especially weak (model year changeover) sales in August. Underlying vehicle sales still look to be flat in dollar terms and declining in unit terms.

So, where in these data are the hurricane effects? Good question. Last month, it seemed that the August sales levels could have been held down by Hurricane Harvey’s hitting the Texas coast on August 25. Today’s data show that any such effects were minor and temporary. The fact is that as immense a human tragedy as these storms are, they generally have little effect on aggregate US economic data, last week’s job report being the glaring exception to that rule.