Private-sector payroll jobs rose by 102,000 in March, with the February level revised downward by 17,000. (This is net of a -50,000 revision to January job growth and a +33,000 revision to February growth.) Our preferred jobs measure, private-sector jobs excluding construction and retailing, saw a 121,000 gain in March, with its February level revised downward "only" 3,000.

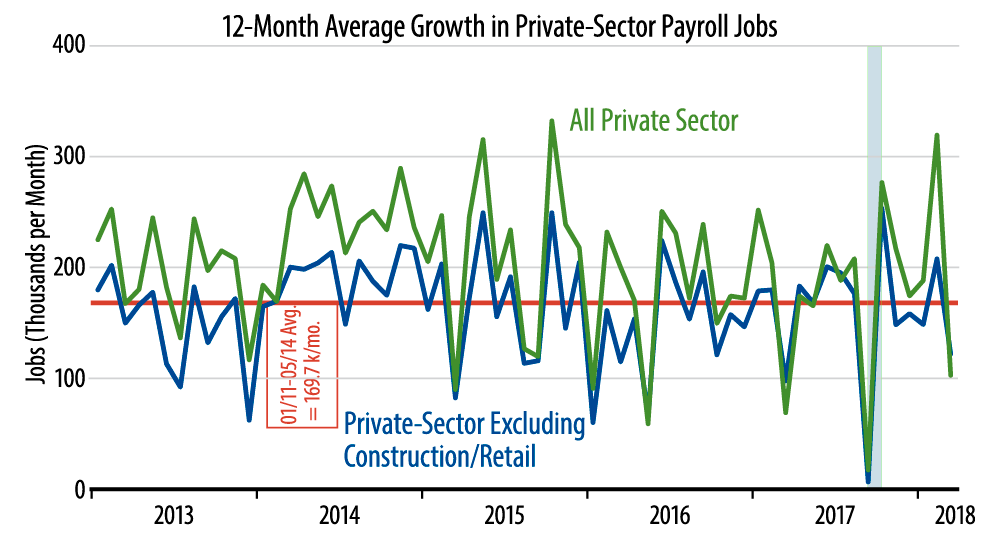

This latter measure now shows growth of 208,000 in February, so its average pace for the last two months is 165,000, about equal to its 170,000 average pace of 2011–15. In other words, underneath all the wailing and gnashing of teeth, underlying job growth has been about average over the last two months, after somewhat below-average readings in the preceding five months.

Despite all the claims about an improving economy, job growth over the last two years has been distinctly slower than what we saw in 2014 and 2015. Once again, maybe we are at or near full employment, but we are not seeing any pickup in growth. Full employment and improving growth are not the same thing.

It is the case that factory-sector job growth has improved over the last two years. That continued in March, with factories adding 22,000 jobs, 11,000 of them for production workers. That better growth in factory payrolls has been fully offset by slower growth in service-sector jobs.

Our grouse against the February jobs report last month was that a large chunk of the headline job gains came in construction and retailing, which are extremely volatile this time of year. Well, construction and retailing pulled back only a bit in March, with construction declining 15,000 on top of a -8,000 revision to February and retailing declining 4,000 on top of a -6,000 revision to February. So, the apparently spurious gains announced last month for these sectors were only partially reversed with today's data.