2015年04月06日時点

March payroll jobs data came in especially weak last Friday, with private-sector jobs up only 129,000 from February. Also, January/February growth was revised down by 59,000, so that the March jobs level was a scant 70,000 above last month's announcement for February.

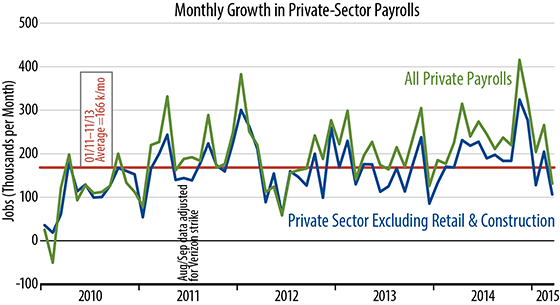

A common theme in the financial press has been: what happened to the economy in 1Q15 to slow job growth down? This question presumes that the strong job growth of late-2014 was the norm and the recent data the aberration. It is just as plausible to argue that late-2014 was the aberration with recent data just the reversal (payback) of previous news that had overstated ongoing growth.

Thus, as the accompanying chart shows, January-March job growth was indeed much slower than that of November-December, but it was right in line with growth trends in place prior to November 2014. In this chart, it is the November-December data that look out of place.

There was also a noticeable move up in job growth in the spring of 2014. However, that move was itself payback for especially weak job growth in December 2013 and January 2014. The polar vortex restrained growth in the dead of winter, but the economy caught up when the weather thawed. Through the last five years there were similar swings up and down, with all those swings eventually reversed.

So, the problem with the analyses in the financial press might be that they take the November-December spurt as a real phenomenon, rather than a temporary bulge. In any case, that bulge has been largely reversed with the last three months' data.

We can abstract from all the swings-weather-induced and otherwise-by looking at data across the last 16 months. From that perspective, job growth has averaged 235,000 per month. This is an improvement from the 209,000 average of the preceding 16 months, but not a huge one. It corresponds to an acceleration of 0.2% in job growth per year. On net then, the pace of labor market expansion has improved some, but not a whole lot, and we take all these data as being consistent with our forecast of ongoing, steady GDP growth in the 2.0%-2.5% range.