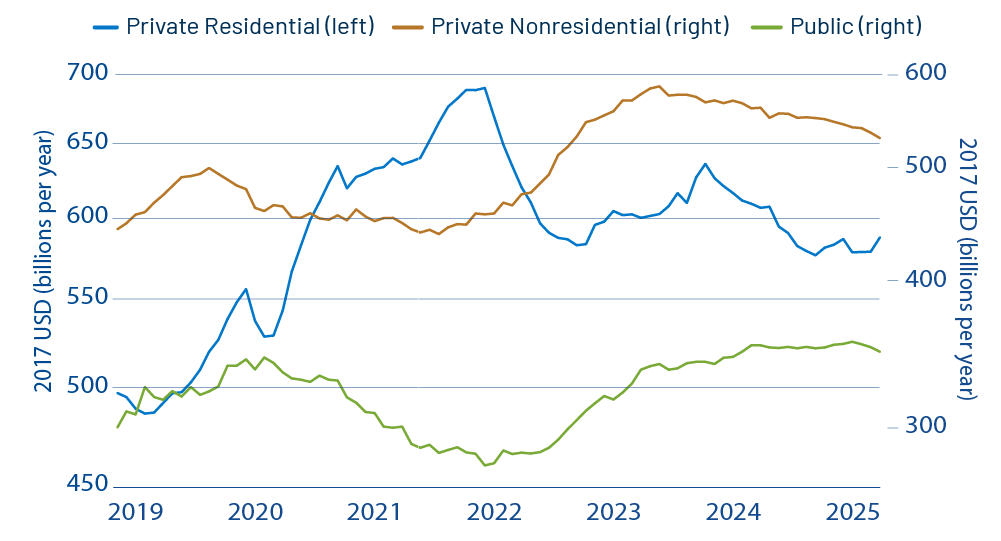

Construction spending rose 0.3% in nominal terms in December. After allowing for rising construction costs, real construction spending was likely flat. This is a slight improvement from the declining trend that we have seen across the board in real construction activity since early 2024, as Exhibit 1 makes clear.

In that chart, we split construction activity into three major components: residential (housing), nonresidential (business investment) and public (government). We’ll discuss each.

Since the pandemic, real construction activity for such traditional sectors as office, retail, communications, lodging, amusements and even transportation (airports, etc.) has been in relentless decline. Over 2022 and 2023, government programs (the CHIPS Act, etc.) unleashed a sharp expansion in construction of manufacturing capacity, and that was abetted by explosive growth in data center construction (AI). Those booms offset ongoing declines elsewhere.

However, manufacturing construction peaked early in 2024. While it remains at elevated levels, the ongoing declines in other nonresidential construction sectors have reimposed a decline in overall nonres construction. Data center activity continues to rise, but it is just not large enough to carry the nonres sector by itself. Meanwhile, government construction rose in tandem with the boom in manufacturing construction and has similarly gone flat since early 2024.

Which brings us to housing. The pandemic and its after-effects are dominant undercurrents here as well. The Covid-induced flight to exurbia drove a boom in new-home activity, with prices jumping in response. Sharply rising mortgage rates following Federal Reserve tightening in 2022 combined with the higher prices to vastly reduce affordability of new homes. Yet, homebuilders continued at elevated construction levels into 2022, despite plunging new-home sales from late-2020 on.

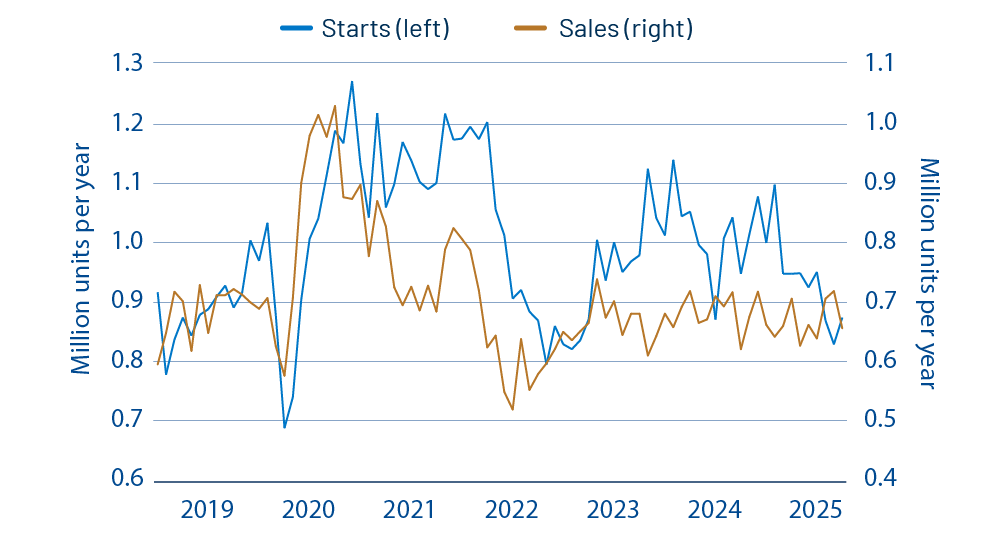

We have been dealing with a glut of new homes ever since. The good news is that this glut finally seems to be getting absorbed. New-home sales have not bounced meaningfully, but construction of new homes has finally been reined in to levels consistent with current demand, as seen in Exhibit 2, so that inventories of new homes are stabilizing. Granted, new-home inventories remain at very high levels, and housing starts may have to fall further to actually reduce inventories, rather than merely stabilize them.

Still, first things first. It is encouraging to see housing start levels more in line with new-home sales. Meanwhile, residential construction cost inflation slowed dramatically in 2025 and actually went negative in 4Q25. If that leads to further declines in new-home prices, a resulting rise in new-home sales would reduce the chances of further declines in residential construction activity.

Another interesting development in the new-home market is that buyers are shifting their focus to homes that are already completed. Prior to 2020, homes under construction or not yet started invariably accounted for more than 60% of total new-home sales. The pandemic changed that, and sales of non-completed homes have been declining ever since. Currently, sales of completed homes account for more than 60% of new-home sales, a total switch from pre-2020s norms.

It would seem that with housing affordability such an issue presently, buyers are understandably reluctant to commit to a home that is not yet available for occupancy. This shift should not materially affect builders’ profit margins, but it might make them more hesitant to ramp up construction in anticipation of strong demand.

Bottom line, we think Covid factors continue to weigh on construction activity. Until manufacturing output is booming more strongly than recently, we are not likely to see further increases in manufacturing construction, and other nonres sectors are still in post-Covid decline mode. Public construction likely will be constrained by government budget problems. Housing construction could stabilize in the months to come, but it is unlikely to rise meaningfully until both mortgage rates and new-home prices are substantially lower than current levels. If the US economy is going to grow strongly this year and next, that has to come from the manufacturing and services sectors, not from construction.