Today’s trading was auspicious, with releases on both consumer inflation (CPI) and retail sales for the markets to chew on. Bond market pricing so far today has been favorable in response, with bond prices up prior to the releases and up further after the news.

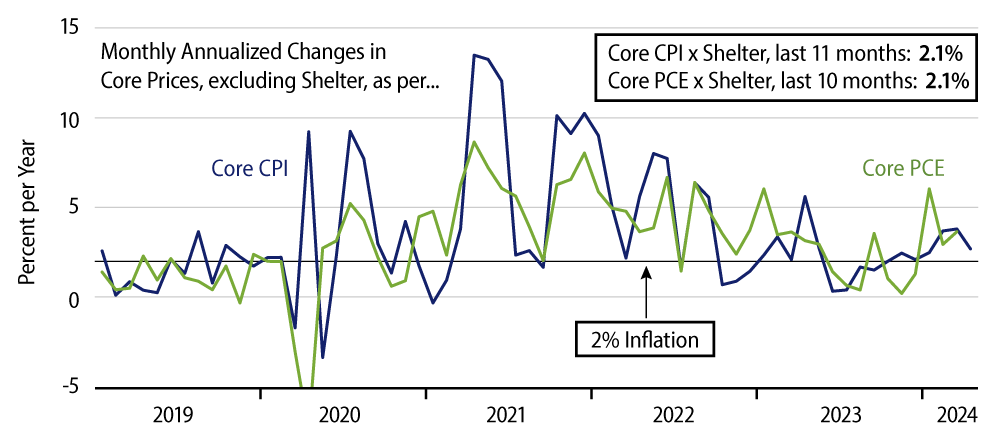

The April CPI showed an increase of 0.31% month-over-month (MoM), while the core CPI rose 0.29% MoM. Given Federal Reserve (Fed) Chair Jerome Powell’s remarks about potentially distorted shelter inflation data, we have been tracking a measure of core inflation that excludes shelter costs. That measure rose 0.22% MoM. These gains translate to annualized rates of increase of 3.8%, 3.6% and 2.7%, respectively.

Obviously, all these rates of price gains are above the Fed’s 2% inflation target. However, they are moves down from what was reported for inflation in February and March. Also, there were some incipient signs of moderation in the aforementioned shelter cost measures. So-called homeowners’ rents were reported as rising at a 5.2% annualized rate in April, with tenants’ rents rising at a 4.3% rate. Both of these were moderately lower than the 6% readings these measures had been giving off since last summer.

We are not quite back to the Fed’s comfort zone for inflation, but there was some renewed progress there, and so some light at the end of the tunnel. Actually, for the last 11 months, core CPI inflation less shelter has proceeded at an annualized rate of only 2.1%. So, if the progress of the last year is merely sustained and shelter prices start behaving, the Fed’s goals will be achieved.

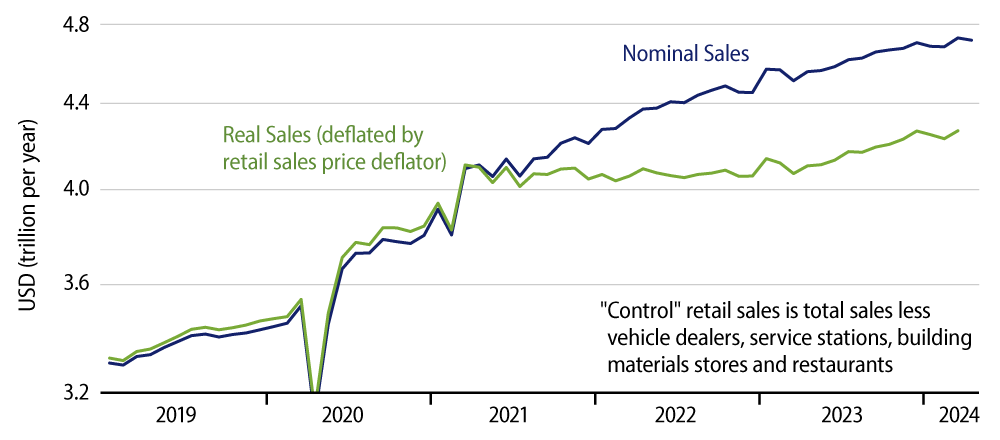

The retail sales news was more impressive. Headline retail sales were unchanged in April, from a March sales level that was revised down by -0.4% from last month’s estimate. For the closely watched “control” sales measure, sales declined by -0.3%, on top of a whopping -0.6% revision to March.

After having tread water for two years, retail sales saw vibrant growth from Spring through Fall of 2023. That pickup was a big factor behind the faster GDP growth seen last year. After softish retail prints for January and February, the March release last month suggested that the retail sales spurt was continuing in 2024. Today’s news puts the kibosh on that. In real terms, control sales have been roughly flat for the last four months (-0.7% annualized growth), after having grown at a 6.6% pace in the preceding seven months.

Softer growth in consumer spending on merchandise was a major factor suppressing GDP growth in 1Q, and it is now looking as though we will see similar results in 2Q. The recent sales slowdown is especially conspicuous and interesting for nonstore sales (online vendors). Nonstore vendors had seen average annual growth in real sales of 7.4% over the three years following the end of 2020, but their sales have gone flat since then (actually declining at a -2.4% annual rate since December). Could even the Amazon run dry?

Sales were also declining in recent months in real terms for most other store types, the only exception being electronics. Apparently, consumers are eating out a bit less and reining in online shopping, but still buying those smart phones!

All in all, these data leave a summer Fed rate cut in play. We will likely have to see further progress on inflation and nothing explosive from job growth or consumer spending, but after the payroll release two weeks ago and the CPI and retail news today, a summer rate cut is a much better bet now than it was in late-April.