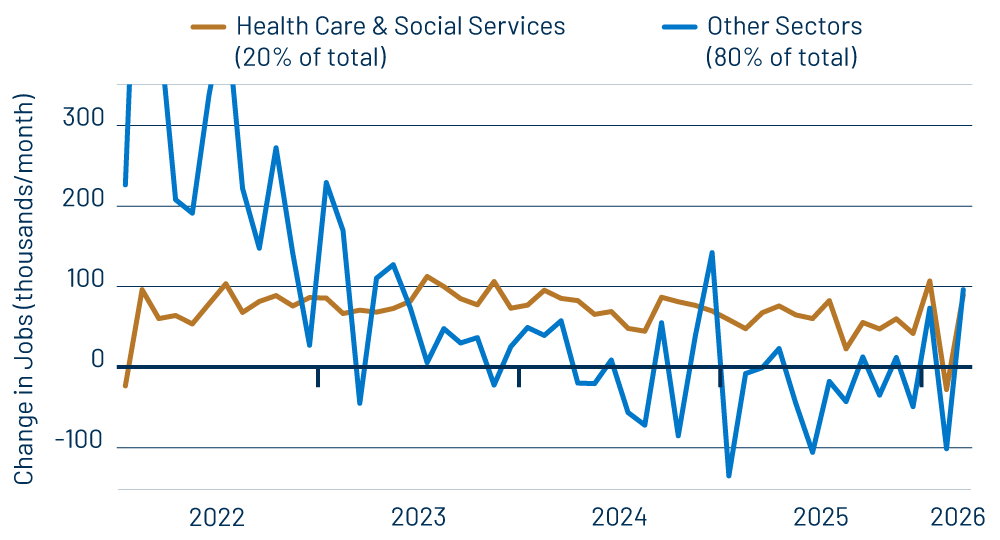

Private-sector payroll jobs rose by 186,000 in March, with only a very slight, -9,000 revision to February jobs data. When the weak February jobs data were released a month ago, we cautioned that the weakness most likely reflected the effects of a strike in the health care industry and blizzards that buffeted the East Coast. The stronger gains for March, then, are mostly a reversal of those effects.

As you can see in Exhibit 1, health care sector jobs were unusually soft in February, thanks to the strike. After the strike ended in March, health care job growth rebounded. Similarly, outside health care and social services, the February weakness was more than offset in March, indicating that severe winter weather depressed February hiring and workplace attendance.

Beneath the month-to-month noise, we detect a trend toward better job growth recently. For private sectors outside health care and social services, the ups and downs of the last three months average out to a monthly gain of 23,000 jobs in 2026. That compares to a -10,000 average monthly loss over 2024 and 2025.

No, that is not boom-like growth, nor even healthy growth, and the fact remains that most of the net growth in private-sector jobs is coming from health care and social assistance, sectors that are heavily dependent on government outlays, rather than on private-sector activity. Still, there is some improvement apparent outside health care.

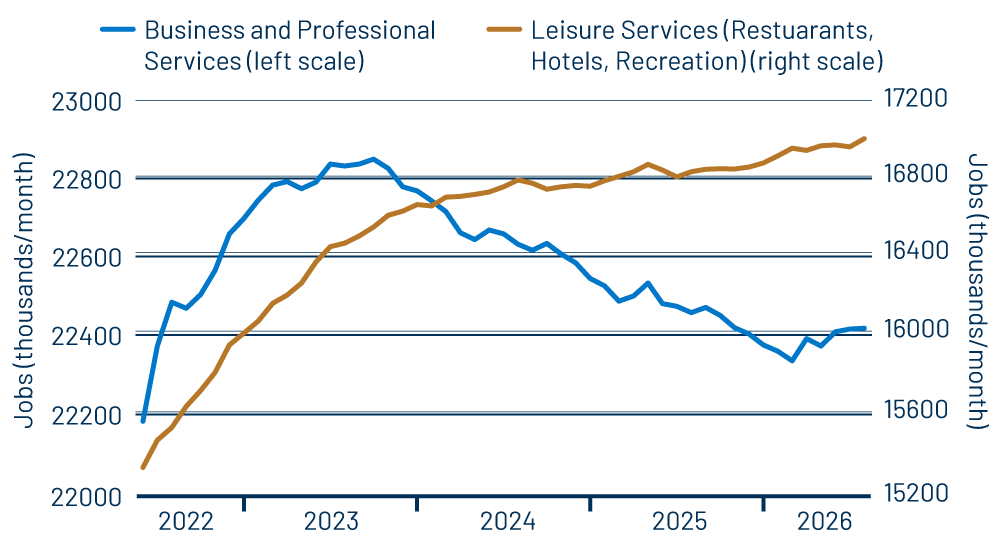

Exhibit 2 provides a good perspective on this improvement. The chart compares jobs in the professional and business services sector versus those in leisure (hotels, restaurants, venues). Professional and business services had been shedding jobs on net since early-2023, but have shown job growth since October, a swing of about 23,000 jobs per month to the good. Meanwhile, leisure sectors completed their post-Covid jobs recovery around early-2023 and have shown mostly steady job growth since then.

So, business-related sectors have shown some improvement lately, while consumer-oriented sectors show only slow, steady growth that is dominated, again, by health care and social services. This is in consonance with the overall economy. As we have emphasized in these posts, after languishing over 2023 and most of 2024, the manufacturing sector has rebounded over the last 18 months, thanks mostly to strong growth in capital spending. Recent months’ performance of business services jobs suggests that the better tone in manufacturing is spilling over to business services.

In summary, job growth is hardly booming, but improvement has to start somewhere, and we have seen such nascent improvement in manufacturing and, more recently, in business and professional services. We don’t expect much boost to consumer spending from the tax cuts, but perhaps we will see improvement there driven by other factors. In any case, the February job lull indeed looks to have been ephemeral, driven by the labor strike and winter weather, and underneath the noise, job growth is improving modestly.