Private-sector payrolls rose only a slight 49,000 jobs in June, and there was an equal-sized, -50,000 revision to May private-sector jobs estimates. The revision within restaurants & bars alone was larger than the total net revision for all private-sector jobs, as May employment estimates for restaurants & bars were marked down by -58,000 jobs, and on top of that revision, the sector was reported to have lost -33,000 jobs in June.

Recall from our post on June 5 that we thought there were likely flukes in the strong May payroll report, namely very strong (+48,000) job gains at restaurants & bars in May. We saw no preceding improvement in restaurant sales that would have justified such a jump. Other analysts thought the increase reflected World Cup hirings. So much for that explanation. The strong restaurant job gains reported last month are now fully gone from the data, with restaurants & bars now showing a net decline in jobs over the last three months and essentially no change for the year to date.

This perspective is important, because it casts a different light on the data for both May and June. A month ago, other analysts were fretting that May job data were so strong that they would push the Federal Reserve (Fed) toward tightening. That previously reported 120,000 May gain in private-sector hiring was only 72,000 apart from what we saw in restaurants & bars, and June’s “measly” 49,000 gain in private-sector hiring becomes a more respectable 82,000 gain when restaurants & bars are abstracted from. Meanwhile, the once “strong” May private-sector job gain is now only 87,000—and just 67,000 outside of restaurants & bars.

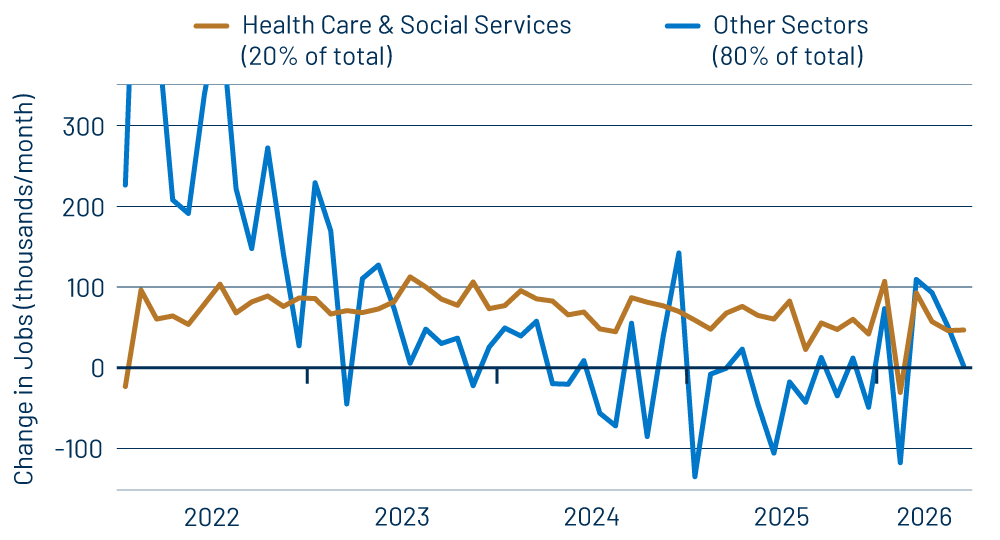

Neither month’s job gains are cause for alarm in either direction, especially when one recalls that the government-dependent sector, health care & social services, continues to account for more than half of private-sector job growth (even though it accounts for only 20% of private-sector jobs). Yes, the near-zero June change in private jobs outside of health care & social services becomes a more healthy +35,000 gain. The 2026 job gains are an improvement over what we saw in 2024 and 2025, but in our view don’t represent outsized growth that would concern the Fed.

Meanwhile, wage gains remained restrained. For 2026 to date, both the all-worker and production-worker measures of average hourly wages show annualized growth right at the 3.5% rate that is consistent with the Fed’s 2% inflation target.

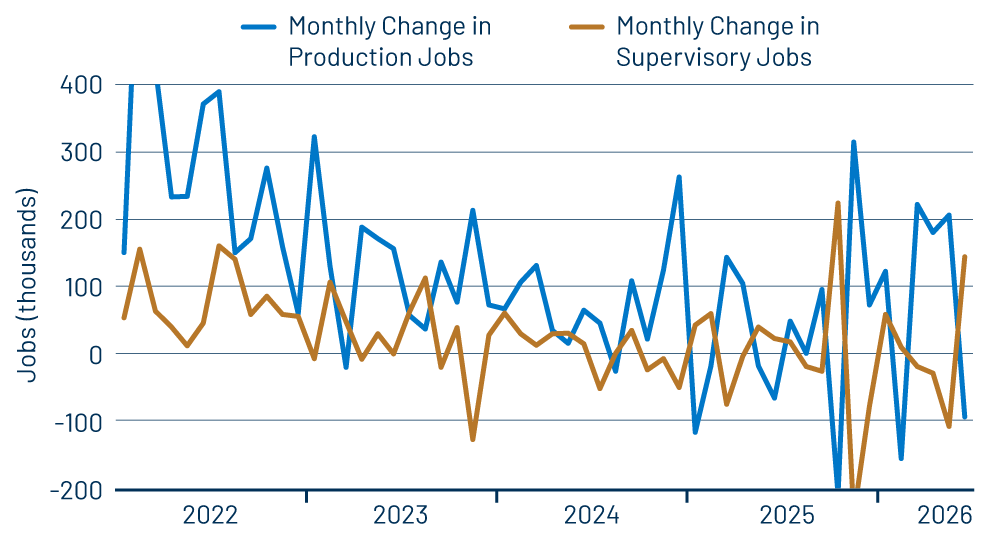

Finally, a month ago, we also pointed out that job gains for recent months through May had been mostly in production-worker jobs, with supervisory jobs actually declining, which was supportive of domestic output growth. Well, that trend also went agley—as the Scots would say—in June, with production jobs declining and “super” jobs up sharply. The June swings don’t fully negate 2026 trends toward production jobs over super jobs, but they at least interrupt them.

Even on the May data, we thought it was silly to be looking for Fed tightening, as 2026 job growth was a welcome change from 2024-2025 torpor, wage gains were restrained, and both tariff and Iran-conflict-related price pressures were not appropriate targets for the Fed’s ministrations. That is even more so the case this month, with May job “excesses” reversed, wages still restrained and oil prices likely to have downward effects on inflation at least for the next few months.