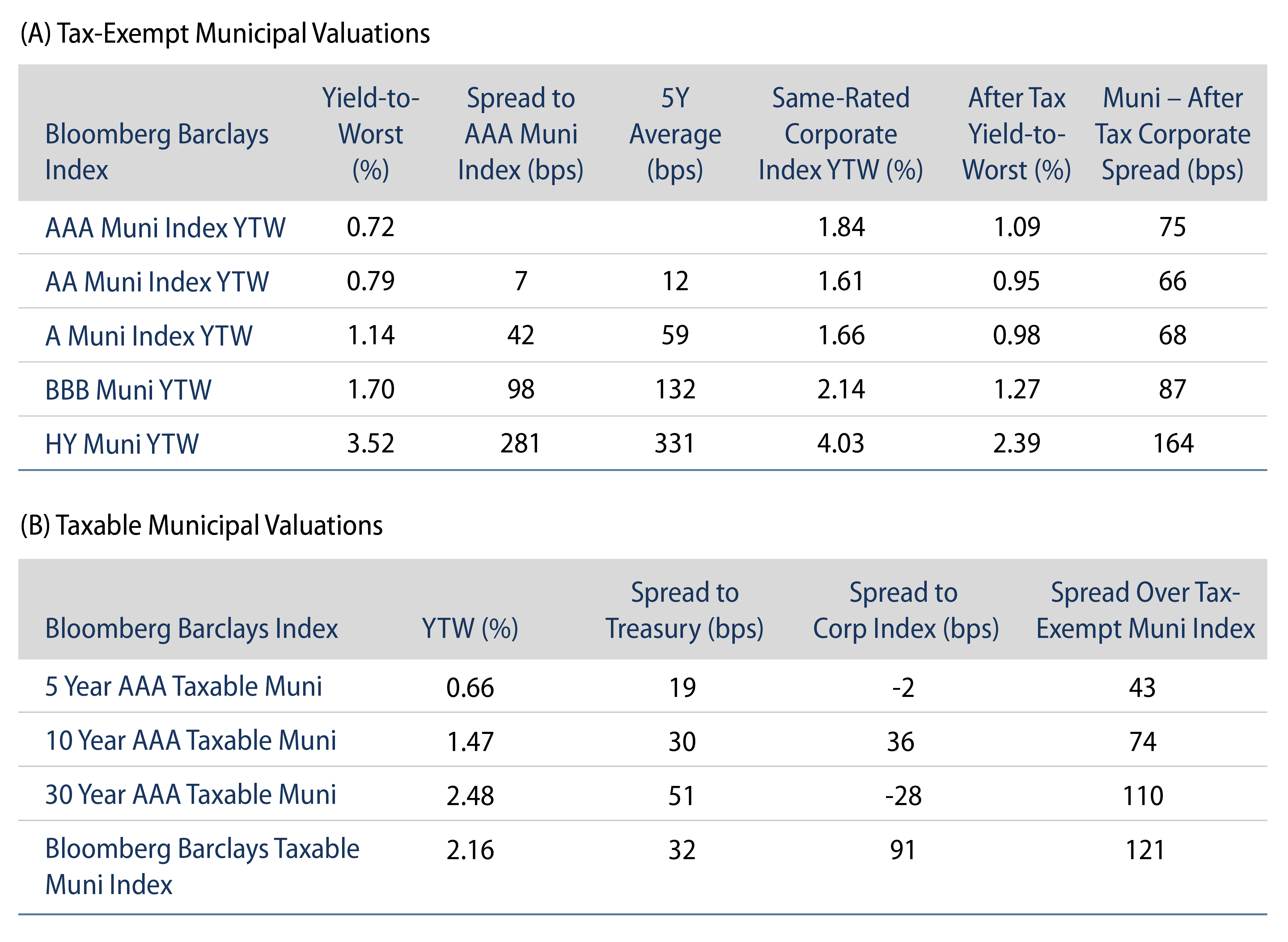

Municipal Yields Moved Modestly Higher, Outperforming Treasuries

Municipal yields moved modestly higher. Municipal mutual funds recorded a 13th consecutive week of inflows. AAA municipal yields moved 1 bp higher across short and intermediate maturities. Municipals outperformed the Treasury selloff as ratios approached record lows. The Bloomberg Barclays Municipal Index returned 0.09%, while the HY Muni Index returned 0.16%. This week we discuss the stress and potential opportunities in the Senior Living sector.

Positive Fund Flows Continue to Support Favorable Technicals

Fund Flows: During the week ending February 3, municipal mutual funds recorded a 13th consecutive week of net inflows, totaling $1.6 billion, according to Lipper. Long-term funds recorded $1.2 billion of inflows and high-yield funds recorded $610 million of inflows, while intermediate funds recorded $87 million of outflows. Year-to-date (YTD) net inflows total $17.2 billion.

Supply: The muni market recorded $8.1 billion of new-issue volume during the week, up 7% from the prior week. New issuance YTD of $34.5 billion is up 11% year-over-year. This week’s new-issue calendar is expected to increase to $8.5 billion (+5% week-over-week). The largest deals include $714 million Tennessee State School Bond Authority and $863 million state of Washington transactions.

This Week in Munis: Senior Living Stress Presents Potential Opportunities

The Senior Living sector, including Continuing Care Retirement Communities (CCRCs)/Life Plan Communities, has been one of the hardest-hit sectors in 2020. The sector, already facing supply challenges ahead of the pandemic, was further stressed by demand issues associated with facilities tragically emerging as COVID-19 hot spots. According to Bloomberg, senior living facilities comprised 35 of the 68 municipal payment defaults in 2020, and six of the eight defaults observed in 2021. Increased defaults and stress in the sector have led to significant underperformance in 2020, with average spreads widening over 250 bps throughout the pandemic, which have not recovered with most of the muni market.

Senior living occupancy rates remain low, falling to 81% as of 4Q20, well below the sustainable target to maintain debt service for most operators. Notably, the latest statistics reveal dispersion between CCRCs and the general senior living market, as well as bifurcation between not-for-profit operators and for-profit providers. CCRC occupancy rates reached 86% at year-end 2020, with non-profit operators operating at 87%, significantly outperforming for-profits which operate at 81%. The health care segments remain hardest hit with occupancy rates at 78% for assisted living and 76% for skilled nursing.

While we expect municipal defaults to remain concentrated within this sector, Western Asset believes such bifurcation in occupancy trends underscores issuer-level opportunities. We favor providers with strong balance sheets that can support these facilities through the duration of the Covid pandemic. We also prefer providers that maintain a diversified operating model, including multiple facilities that are proportioned over a variety of levels of care. In our view, a strong independent living component drives profitability and mitigates the weakness in the health care units.

Macro trends should also support the sector. New construction has slowed as the industry focuses on supply absorption. The strong real estate market also supports the sector’s entrance-fee model, as home sales are the primary source of funds to buy into a community. Overarching demographics of 20 million more seniors entering the population by 2030 should also favor the sector. While more people will likely choose to “age in place” thanks to technology gains and healthier aging, we believe a large contingent will prefer a more social setting or face health demands that will be better met in a facility.