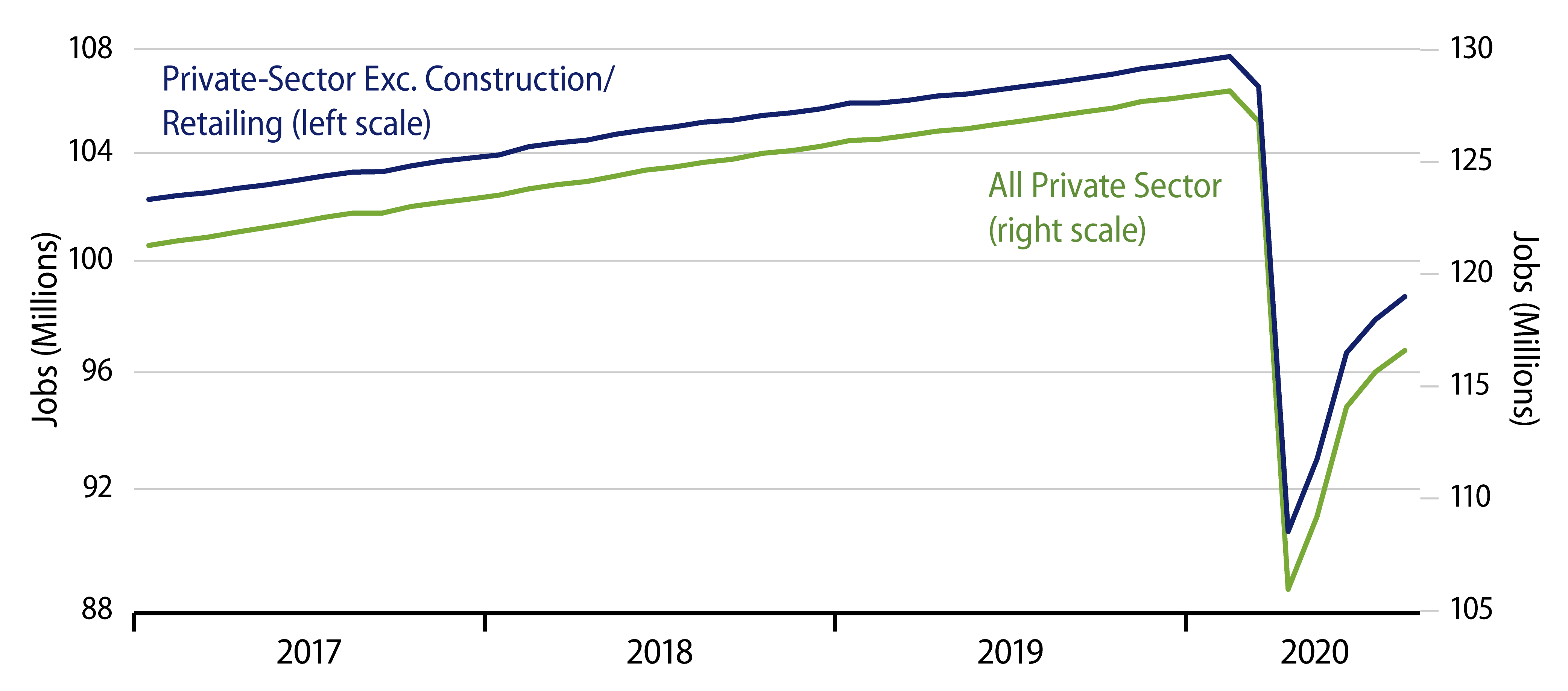

The Bureau of Labor Statistics reported today that private-sector payroll jobs rose by 1,027,000 in August, with a slight upward revision to the July jobs estimate. Government jobs rose an additional 344,000, thanks largely to 2020 Census hiring of as many as 250,000 workers, though local government jobs also rose by 95,000.

Across the range of industries, there were job gains almost everywhere. Economists cited in the press lament a supposed loss of momentum in the job market recovery. This complaint seems fatuous to me. There was no way the economy could replicate the 8 million jobs gained in May and June. That was driven by rebounds in industries fully and artificially constrained by the March/April shutdown and fully reopened in May. Since then, further reopening of remaining industries has proceeded only haltingly.

Other sectors, such as construction and manufacturing, are only gradually recovering toward pre-Covid operating levels, but I find it encouraging that their rebound is continuing. For construction, we have already seen a complete recovery in new-home sales. Housing starts, residential construction spending and jobs follow only with a lag, but there is every reason to believe they will follow. As for manufacturing, consumer demand for merchandise is back essentially fully, and capital goods order have rebounded nearly fully, but foreign trade volumes have not yet re-attained February levels. Lags are working here, too, and manufacturing continues to post monthly gains.

And then there are the hardest-hit service sectors, some of which are only barely bouncing off the bottom. Of these, health care has staged the strongest rebound, regaining 842,000 jobs over May-August after a loss of 1,588,000 jobs (about a 12% decline) in March and April. Restaurants have regained 3,588,000 jobs, after a 6,776,000 decline (about 50%). These two sectors have seen the best recovery in this area, and even they have recouped only about 50% of their Covid-related shutdown losses.

For recreation, following a loss of 1,229,000 jobs (roughly 50%), recent months have seen a rebound of only 459,000 jobs. For passenger travel, a loss of 324,000 jobs (roughly 35%) has been followed by a gain of only 57,000. Accommodations lost 912,000 jobs (about 50%) during March/April and have regained only 132,000 since.

All these singled-out sectors are either still shut down and/or hampered by customers’ fear of utilizing them. That they have bounced at all is at least somewhat impressive. For economists to bemoan the lack of a stronger bounce in these sectors is like forcing a boxer to use only one arm, then complaining about their lack of aggressiveness.

Another question is how much Washington thinks fiscal and monetary stimulus will help. Service sectors are not known to be very interest sensitive, and Presidential/Congressional harangues are not going to reinvigorate foreign trade flows. Meanwhile, nothing coming from federal or local governments is helping boost utilization of basic health care or the “leisure” services detailed here.

The recovery is continuing and at a pace faster than economists were expecting just three months ago. That is more heartening than the consensus response would let on.