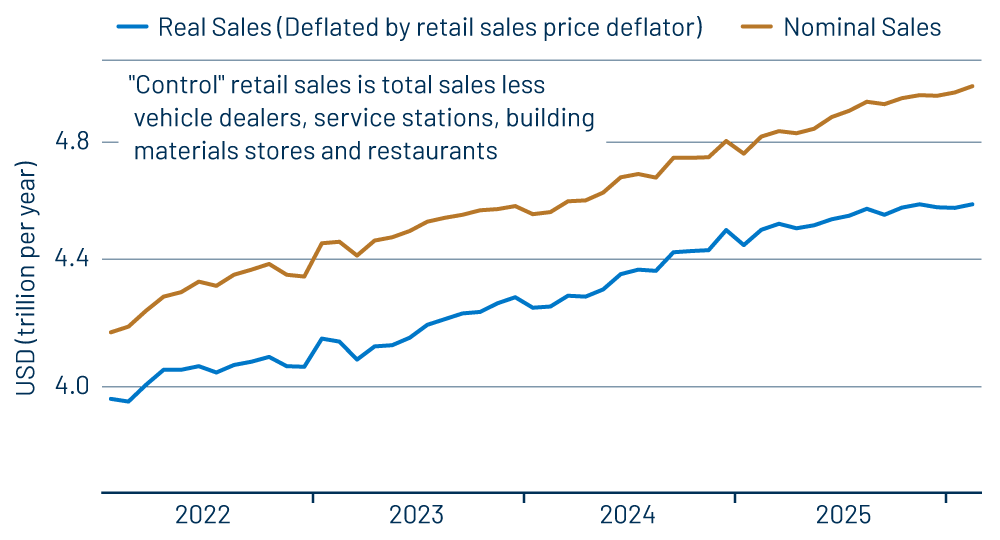

Headline retail sales rose 0.6% in February, on top of a slight 0.1% upward revision to the January sales estimate. Like most economists, we focus on the control measure of retail sales, which excludes sales at car dealers, service stations, building material stores and restaurants, partly because of their higher volatility and partly to focus on store types that cater mostly to households rather than other businesses. That control measure showed a 0.5% increase in February off a slight -0.1% revision to January.

These results are a modest improvement from those of November-January. However, higher prices for retail merchandise ate up much of the gains. As you can see in Exhibit 1, today’s data indicate that nominal retail sales are essentially back on the trend path we have seen over the past five years, but in real terms, sales have leveled off over the last three months. Obviously, faster price gains for merchandise have eaten into real growth.

Still, with nominal sales growth steady, it looks as though underlying consumer demand remains stable, but there has been resistance to higher prices. Goods price increases did moderate somewhat in February, to a 0.16% increase off a 0.3% gain in January. Hopefully, the modest February gains in retail sales will continue.

Within store types, sales gains have been strongest recently at building material stores, car dealers, electronics stores, books/sporting/toy stores, online vendors and department stores. Sales have flagged a bit at furniture stores, drug stores, grocery stores and restaurants. Overall, consumer spending does not look to be weak, but it has seen slower growth recently, mainly due to an increase in goods prices.

No fooling, with today’s release, the Census Bureau is almost fully caught up from the data release delays caused by the government shutdown. Another retail data release is scheduled for later this month, which we will also cover and which will bring Census fully back on schedule. Ironically, we are back on schedule just in time to see what effect the conflict in Iran might have on consumer spending.

Our guess is that the fighting and its associated oil price effects will not have a serious debilitating effect on US consumers or our economy. The 1973 (Yom Kippur War), 1979 (toppling of the shah of Iran) and 1990 (first Gulf War) oil shocks are all commonly associated with rising inflation and a souring economy. In fact, in both 1973 and 1979, inflation had already risen to intolerable levels prior to the upheavals, and the economy had already started to weaken, thanks to Federal Reserve (Fed) tightening to combat inflation. Furthermore, it was price controls on crude oil and gasoline in place then that caused the long gas lines and severely weakened the economy.

The 1990 oil shock was not accompanied by price controls, so there were no gas lines or shortages of fuel. But in that episode as well, the Fed had been tightening policy substantially prior to the oil shock, and the economy was already falling into recession when Iraq invaded Kuwait in August 1990.

In other episodes of sharp oil price increases where Fed tightening was not in play and where prices were allowed to increase oil supply and reduce oil demand, yes, there was pain, but no, there was no resulting recession, and the effects on inflation were brief and did not flow through to “core” inflation. That is, there was little pass-through to prices outside of oil and gas.

Presently, the economy has actually been picking up in recent months, led by an increase in business investment and manufacturing production. We would expect that pickup to continue with only slight collateral damage from the turmoil in the Middle East.