On June 21, 2025, the US launched strikes on three major Iranian nuclear facilities, dramatically escalating tensions across the Middle East. In a recent blog, we expressed growing concern that the US and other global powers could become further entangled in this conflict. We also warned that any direct attack on Iran risked provoking a response that might disrupt Iranian oil production and send shockwaves through global energy markets.

The stakes are high. The Middle East supplies about a third of the world’s oil, and while Iran’s share is smaller—roughly 4% of global output—it remains a key player. The real danger, however, extends beyond Iran’s own production. The conflict threatens to spill over into the wider region and jeopardize vital transit routes, especially the Strait of Hormuz.

Indeed, just hours after the US strike, Iran’s parliament endorsed a measure to close the Strait—a move with potentially seismic consequences for global oil flows. Although the final decision rests with Iran’s Supreme National Security Council and Ayatollah Ali Khamenei, who have not closed the Strait as of this writing, the mere possibility is enough to unsettle markets and put upward pressure on oil prices.

It’s important to note that the Strait of Hormuz is the world’s most critical oil chokepoint. Each day, about 20% of global oil consumption—nearly a third of all seaborne oil—passes through its narrow waters. This strategic corridor connects the Persian Gulf to the Arabian Sea and serves as the main route for oil exports from Saudi Arabia, Iran, the UAE, Kuwait and Iraq, much of it destined for Asia. Any disruption, whether from military action or political brinkmanship, could choke off supply and delay shipments. Shipping costs and insurance premiums have already risen. The result would likely be a surge in global oil prices, rattling investor confidence, dampening consumer spending and complicating the already delicate work of central banks. The extent and duration of any disruption would dictate the magnitude of these effects. While there are alternative pipelines, their capacity is limited and cannot fully compensate for a closure of the Strait.

At the time of writing, oil prices have retreated from their earlier highs of the day—a positive sign. However, this does not rule out the potential for prices to climb again should there be a significant escalation in the region. Anticipating the trajectory of oil prices at this juncture remains extremely challenging given the fluid situation and the many variables at play.

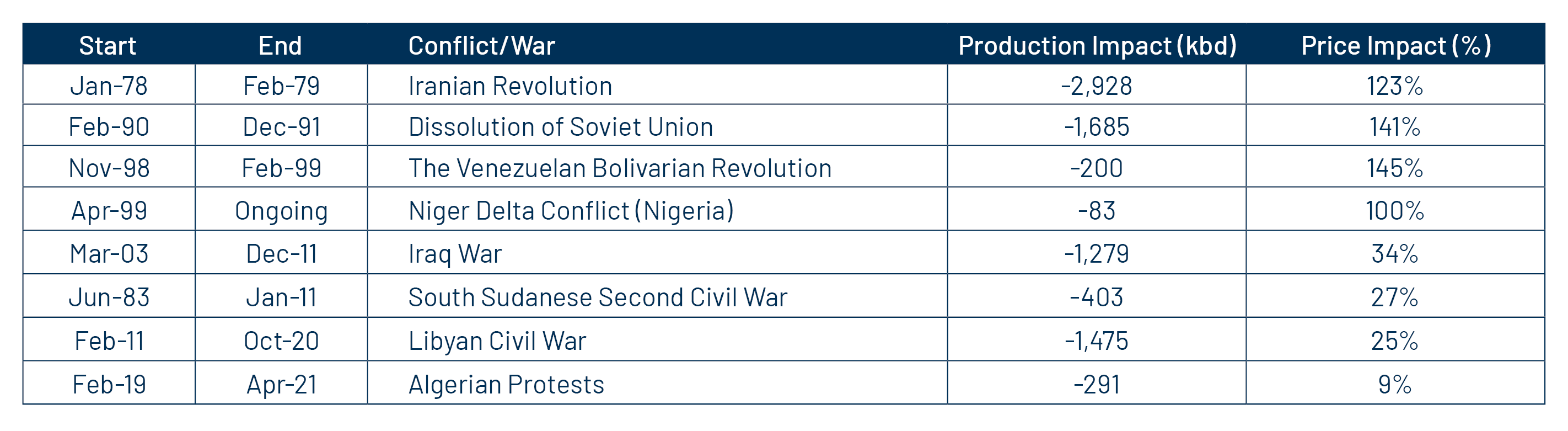

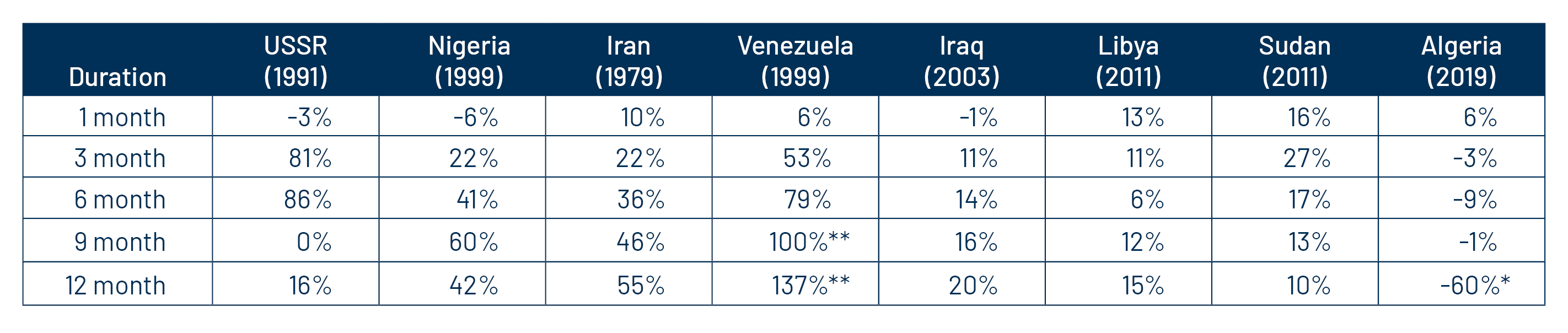

As you can see in the two Exhibits that follow, the impact of geopolitical shocks on oil prices has historically varied widely in both magnitude and duration. Importantly, past events have not resulted in a closure of this critical chokepoint.

Since 1995, the US 5th Fleet, headquartered in Bahrain, has been tasked with ensuring the safety of commercial shipping through the Persian Gulf, as well as overseeing operations in the Red Sea and Arabian Sea. In the current situation, we expect Iran may engage in brinkmanship to restrict passage but is unlikely to fully close the Strait. A complete shutdown would not serve Iran’s interests, as it would cut off its own export revenues and negatively impact its primary oil trading partner, China.

What is clear is that the US bombing of Iran’s nuclear sites has unleashed a wave of political and economic uncertainty, not only for the region but also for major powers like Russia and China, who have significant interests in the Middle East. The next steps taken by Iran, the US and other stakeholders will determine whether the crisis deepens or begins to stabilize. With the fate of the Iranian regime now in question, any upheaval in Tehran could further destabilize the region.

At present, we’re positioned slightly overweight in energy, mainly through domestic US companies. At the end of 2024 and through March 2025, before this latest escalation, we had been in the process of trimming our energy exposure, aiming to move closer to a market weight position. This was based on stretched valuations and OPEC+ shifting its strategy toward protecting market share by ramping up production.

Looking more closely at our portfolios, our bias is toward domestic pipeline operators rather than the more commodity price-sensitive exploration and production (E&P) companies. However, we have maintained exposure to domestic natural gas-oriented producers over their oil counterparts. Recently, E&P firms have prioritized boosting free cash flow and returning capital to shareholders through higher dividends and share buybacks. Their balance sheets and liquidity are in much better shape than in previous cycles, and management teams have been focused on attracting equity investors back to the sector. As a result, these companies haven’t been reinvesting aggressively to grow production as they did in the past.

With the potential for higher oil prices due to the current conflict, we’re closely monitoring how US oil producers respond. Any uptick in activity would take months to translate into higher production, and in our view, the main beneficiaries in the near term would be domestic pipeline companies.