If you’re a regular reader of financial media, you’ve likely noticed some headlines on ESG—environmental, social and governance—investing and sustainable investing on your feed in recent months. Depending on which pieces you’ve chosen to read, interest in sustainable investing is either dead, floundering or thriving. Between these conflicting proclamations, what should an investor believe?

Sustainable Investing Means More Than Just ESG Equities ETFs

To address the confusion, let’s first revisit the aphorism “ESG means different things to different people.” As defined by the Global Sustainable Investors Alliance in partnership with the CFA Institute and the Principles of Responsible Investment (PRI), sustainable investing can be differentiated across five categories: 1) screening (a.k.a., Socially Responsible Investing (SRI)), 2) ESG integration, 3) thematic investing, 4) stewardship and 5) impact investing. While an investment mandate may fall into more than one of these categories, each is distinctly different in terms of technique and objectives. As a result, lumping the different types together when analyzing market trends and investment performance may lead to unmeaningful or even spurious conclusions.

To illustrate, many news stories focus on ESG equities ETFs. A significant number of these are ESG integration funds and are typically passively managed against benchmarks constructed around MSCI ratings. Many of the passive ESG ETFs are heavily tilted toward technology and exclude energy, which has resulted in significant performance dispersion in recent years. Other ESG ETFs are thematic funds that are narrowly focused on specific sectors and technologies rather than a diverse set of issuers. These integration and thematic funds are not necessarily representative of other funds with specific sustainable investing objectives.

Furthermore, sustainable investing is not limited merely to corporations issuing publicly traded stock. Within fixed-income, the investment opportunity set also includes private corporate issuers, sovereigns and quasi-sovereigns, municipal bonds, and mortgage-backed and asset-backed securities.

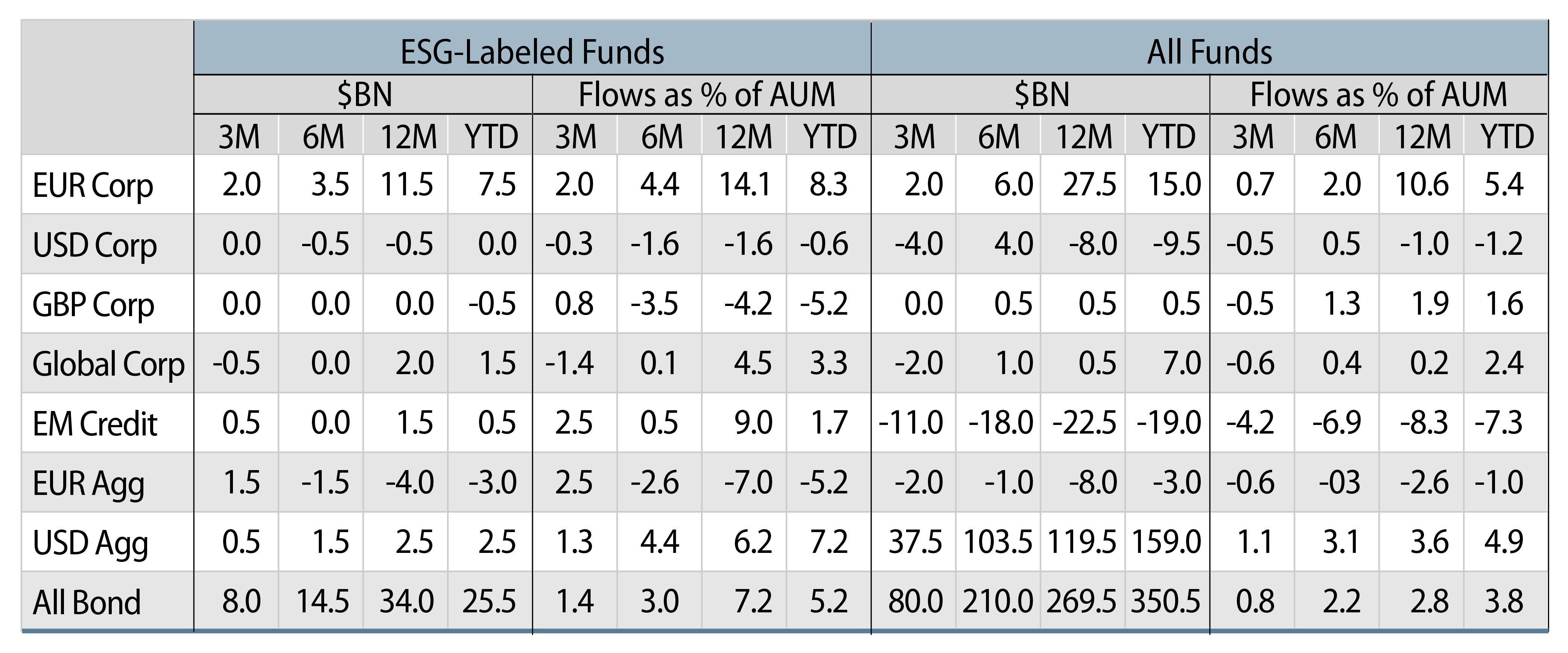

Sustainable Bond Fund Flows Remain Robust1

Next, let’s look at the data on fund flows. We emphasize that trends in sustainable investments should be analyzed in the context of the overall market. If money is flowing into an asset class overall, then it should not be surprising if the sustainable fund segment of that asset class is also growing, and vice versa.

As yields have moved attractively higher this year, investors have increased their fixed-income allocations in response, adding $350.5 billion, or 3.8% of fixed-income fund AUM, to bond funds year to date (YTD) through Q3, according to Barclays (Exhibit 1). In comparison, ESG-labeled bond funds have attracted $25.5 billion, or 5.2%, in the same time period. At a more granular level, sustainable funds have outperformed the broader sector in in the EUR corporate, USD corporate, global corporate, emerging market credit and USD aggregate subcategories, and underperformed in the GBP corporate and EUR aggregate subcategories. Market share varies by region, with ESG-labeled USD corporate funds comprising only 3.5% of the sector, versus 34.1% for the EUR corporate fund sector.

ESG-Labeled Bond Market Continues to Grow

According to Bloomberg New Energy Finance, ESG-labeled bond issuance this year through October 31 stands at $900.5 billion, up 5.6% relative to the same time period last year. For reference, global investment-grade issuance YTD was down 2% at $1.08 trillion.2 We would also note that green bonds, which are the largest and most established category, experienced a strong increase, up 13.1% year-over-year.

Again, issuance trends differ across credit quality and geography, with the strongest representation in the EUR investment-grade market, where 15.4% of the Index is ESG labeled, while the US High Yield Index contains only 2.1% in ESG-labeled bonds.

ESG-Labeled Bond Issuance Is Correlated With Better Issuer Performance Overall

ESG-labeled bonds trade at a premium, or “greenium,” relative to non-ESG bonds, suggesting that there is strong investor demand for sustainable fixed-income investments. Western Asset’s view is that the greenium is largely driven by supply/demand imbalances, as the credit quality is identical between an issuer’s ESG-labeled and traditional bonds. Controlling for issuer, this premium has ranged from 0 to -5 bps for green, social and sustainable bonds (all of which are “use of proceeds” bonds that finance green and/or social projects exclusively), whereas it has moved from a premium to a discount for sustainability-linked bonds.3

Given that use of proceeds bonds tend to be issued at tighter spreads than their non-ESG counterparts, you may wonder whether they have generated lower returns as a result. Some superficial analyses compare the returns of a corporate green bond index with a broad corporate index; however, this methodology is inappropriate for two reasons. First, green bond indices lack sector diversification and are more weighted toward financials and utilities than broader indices. Second, green bond indices tend to be comprised of longer maturity bonds than broader indices.

In contrast, a proper comparison of ESG and non-ESG bond performance adjusts for issuer, sector and maturity, as does HSBC. Their researchers found that after issuing ESG-labeled bonds, issuers benefit from what they term a “halo effect,” in which both the ESG-labeled and non-labeled bonds of that issuer outperform their peers.4 This effect has been consistent since HSBC began its analysis in 2021.5 These trends support our belief that a significant contingent of investors are seeking to invest in issuers committed to sustainability.

Conclusion

Putting the facts all together, we conclude that sustainable investing in fixed-income is far from its denouement. Western Asset will continue to partner with its clients to help them achieve their financial as well as sustainable investment goals.

ENDNOTES

1. Barclays ESG Quarterly Credit Update: Q3 23. This analysis uses EPFR data and methodology which designates a fund as ESG if any of the following conditions applies: i) it has “ESG,” “SRI,” “Sustainable” or similar wording in the fund name; ii) it is benchmarked to an ESG/SRI benchmark; iii) its factsheet or prospectus has wording that indicates one of its main objectives is investing in ESG/SRI securities; or iv) it is offered by a fund manager whose entire business is built on ESG investing principles.

2. JPMorgan US High Grade Corporate Bond Issuance Review October 2023.

3. Societe Generale.

4. https://www.research.hsbc.com/R/84/hswm76PFl9GvLv

5. https://www.research.hsbc.com/R/10/Fl9GvLv