Macros, Markets and Munis

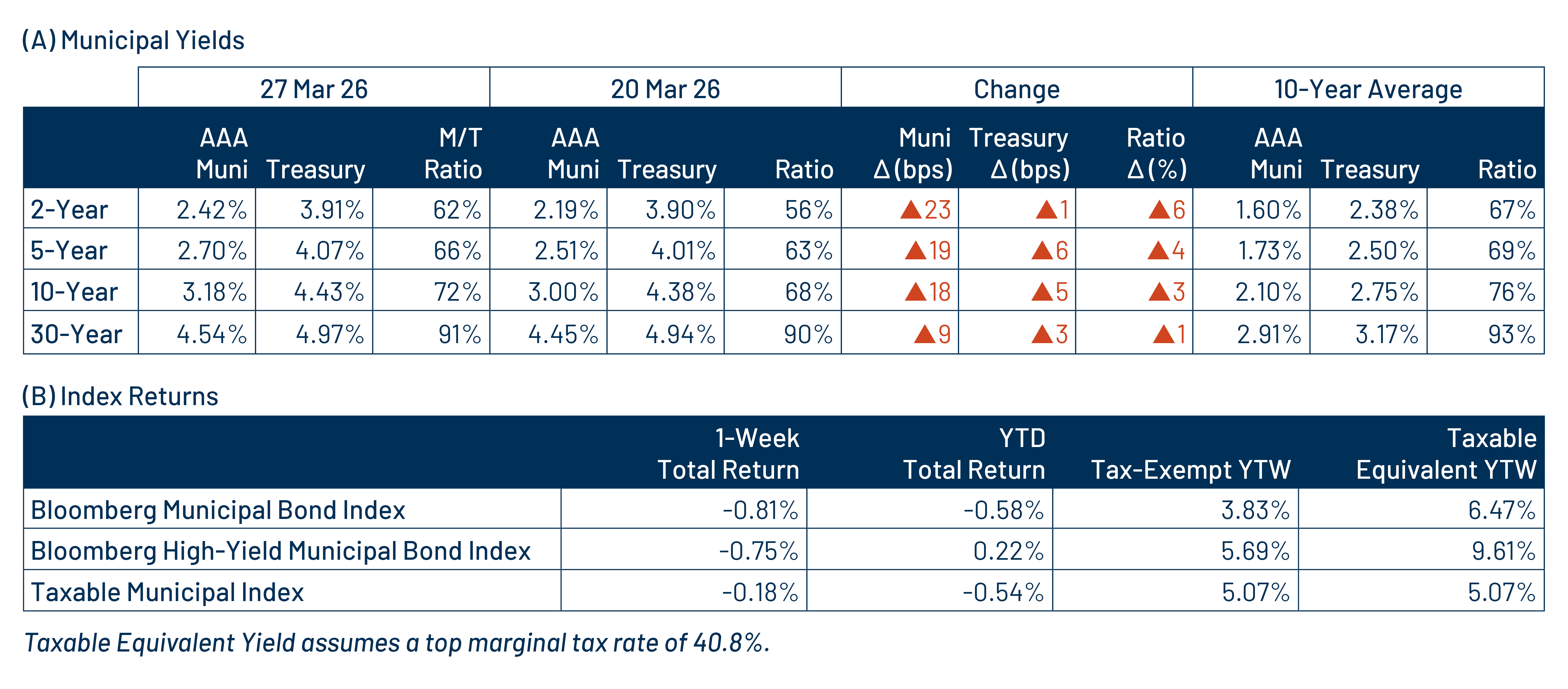

Municipals posted negative returns last week and underperformed taxable fixed-income. Geopolitical developments remained the dominant driver of market volatility last week, as escalating tensions in the Iran conflict pushed oil prices sharply higher. On the macroeconomic front, initial jobless claims ticked higher in alignment with market consensus, as University of Michigan Sentiment data moved lower and fell below expectations. Overall, the Treasury curve shifted higher by 1-6 basis points (bps) across maturities. High-grade municipal yields underperformed, moving 9-23 bps higher across the curve amid weaker technicals. Meanwhile, muni technicals overall weakened substantially amid elevated supply and fund outflows. This week we touch on the Federal Reserve’s (Fed) recently released data on municipal debt holdings.

Technicals Weaken as Funds Post Outflows and Supply Reaches Highest Level of the Year

Fund Flows ($599 million of net outflows): During the week ending March 25, weekly reporting municipal mutual funds recorded $599 million of net outflows, according to Lipper. The majority of outflows came from long-term funds which recorded $905 million of net outflows. Meanwhile, intermediate and short-term categories recorded $193 million and $28 million of net inflows, respectively. Last week’s outflows broke a 17-week streak of inflows, bringing year-to-date (YTD) inflows to $24 billion.

Supply (YTD supply of $129 billion; up 17% YoY): The muni market recorded $16 billion of new-issue supply last week, the highest level of supply so far this year. YTD new-issue supply of $129 billion is 17% higher than the prior year, with tax-exempt issuance up 18% year-over-year (YoY) and taxable issuance down 6%, respectively. This week’s calendar is expected to decline to $8.5 billion. The largest deals include two gas-pre-pay deals, $1.0 billion Black Belt Energy and $1.0 billion Texas Muni Gas Acquisition supply transactions.

This Week in Munis: Strengthened State and Local Revenue Collections

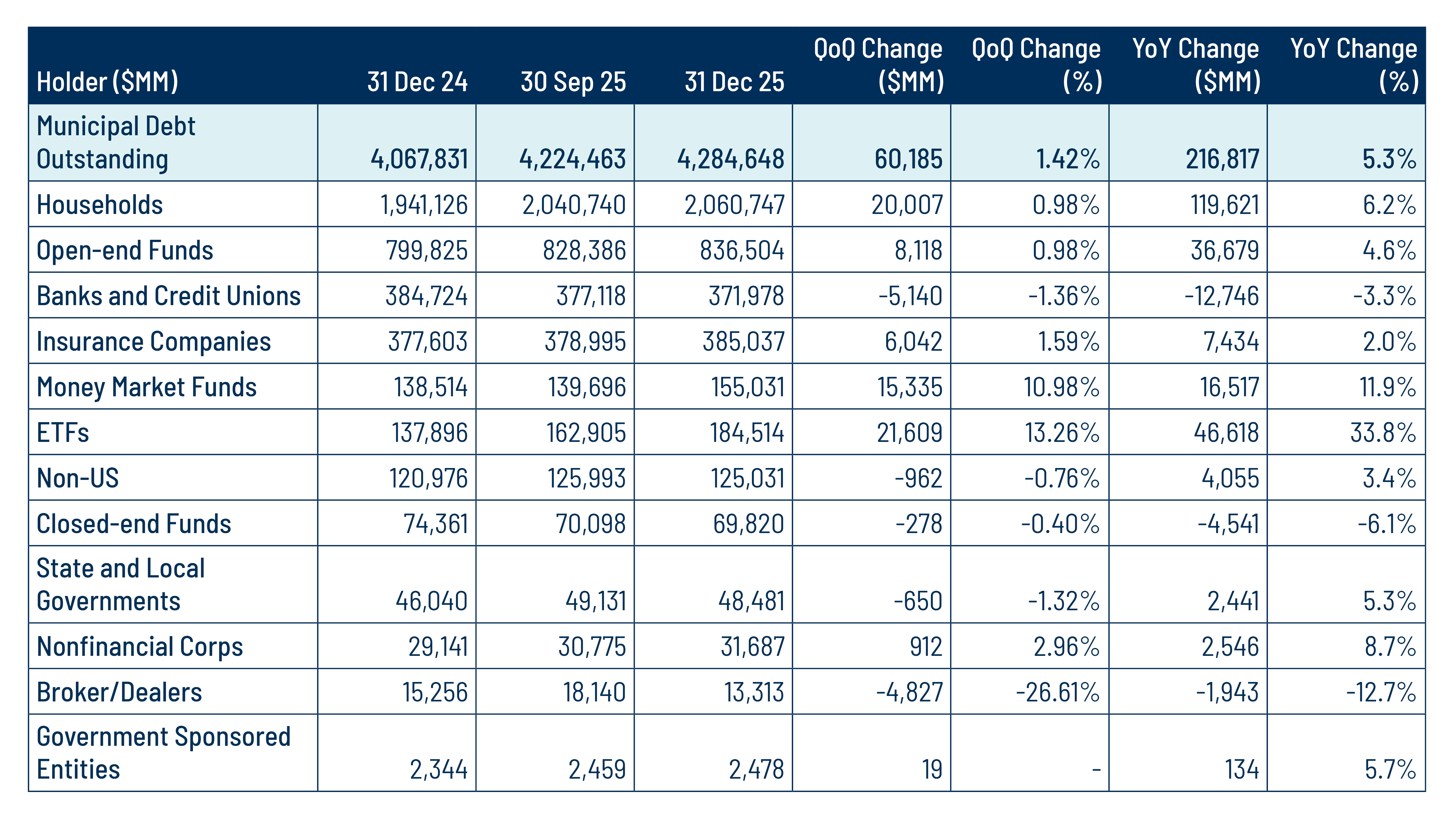

Earlier this month, the Fed released municipal holdings data for 4Q25, providing insight into the demand trends across the muni market through year-end 2025. During the quarter, the municipal market expanded by $60 billion to reach $4.3 trillion. ETFs and money market funds experienced the strongest growth rates during the quarter, increasing by 13% (+$22 billion) and 11% (+$15 billion), respectively. Notably, broker/dealer inventory declined sharply by 27%, indicating a potential drag on market liquidity.

The record supply in 2025 contributed to $217 billion in asset growth across the municipal market. During the calendar year, ETFs exhibited the strongest growth, rising 34% (+$47 billion), compared to traditional open-end funds, which increased just 5% (+$37 billion). Individual household assets grew 6% (+$120 billion), underscoring continued demand for customized SMA solutions. Among major institutional holders, insurance company muni assets rebounded by 2% (+$7 billion) following four consecutive years of declines, largely driven by market returns. In contrast, bank holdings of municipals fell by $13 billion (-3%).

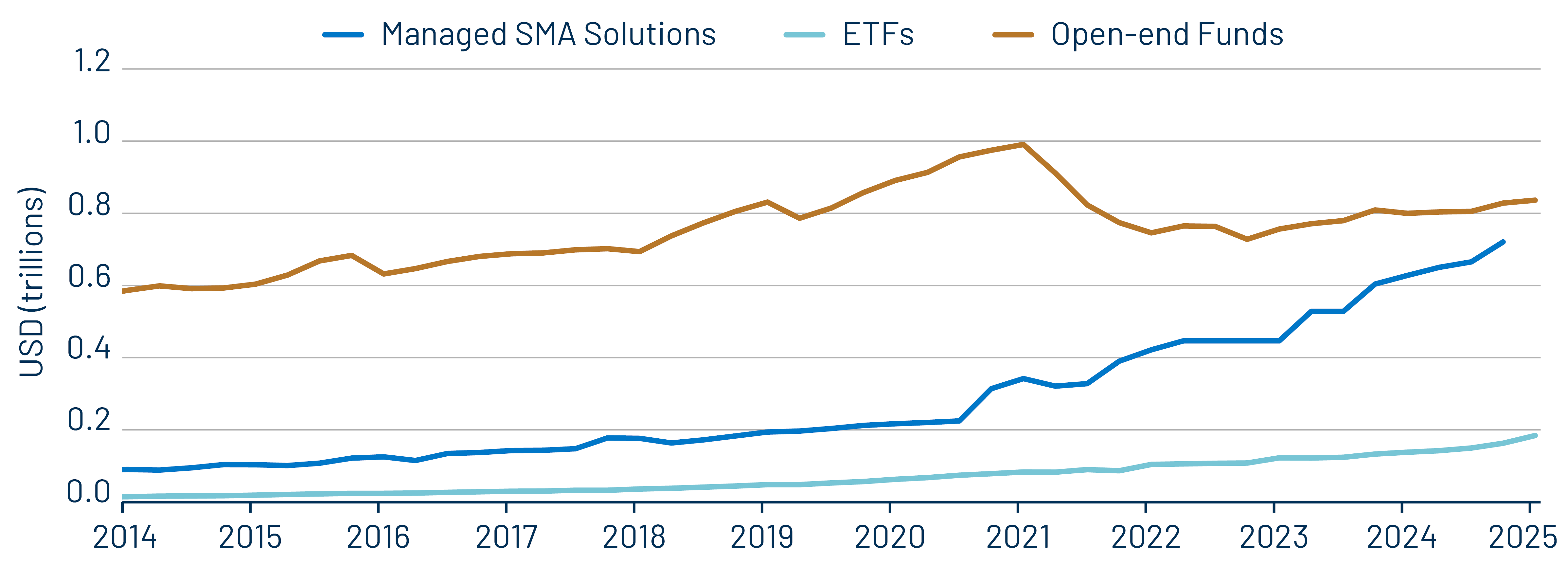

The continued expansion of the individual municipal investor base, relative to institutional participation, has contributed to a more concentrated ownership structure within the muni market. This shift, combined with reduced broker/dealer inventories, has the potential to strain market liquidity and amplify periods of volatility. A growing share of individual assets is being directed toward SMA strategies focused on short- and intermediate-term maturities, contributing to the persistently steep muni yield curve and pressured valuations in the front end over the past year. Western Asset expects these dynamics to continue influencing valuations across the yield curve, creating opportunities for active managers positioned to navigate these demand and liquidity conditions.

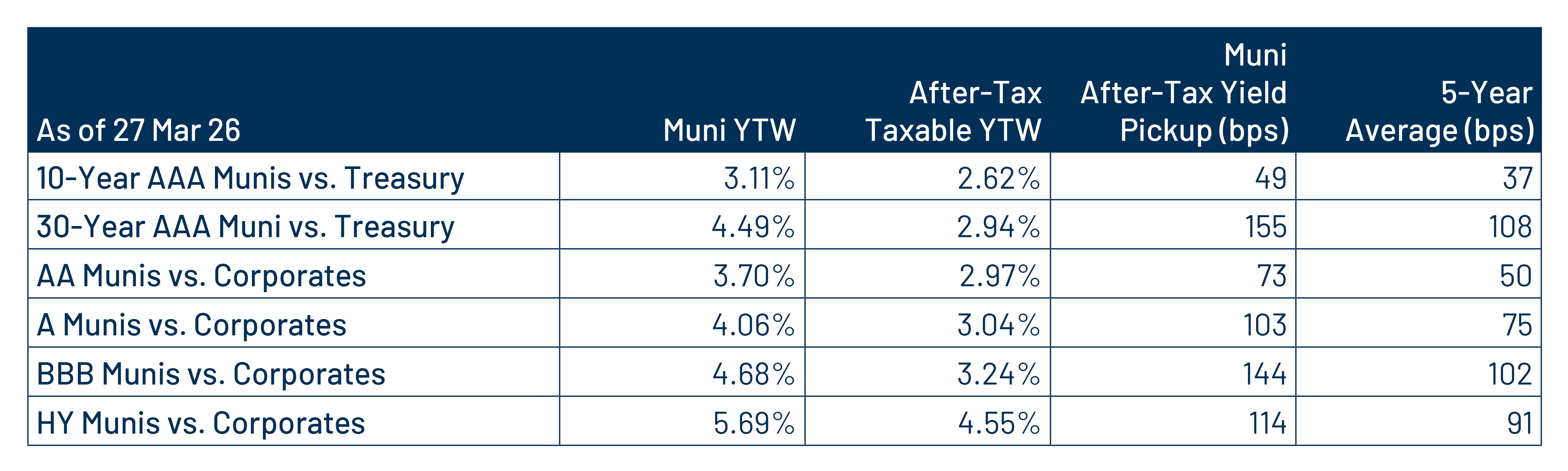

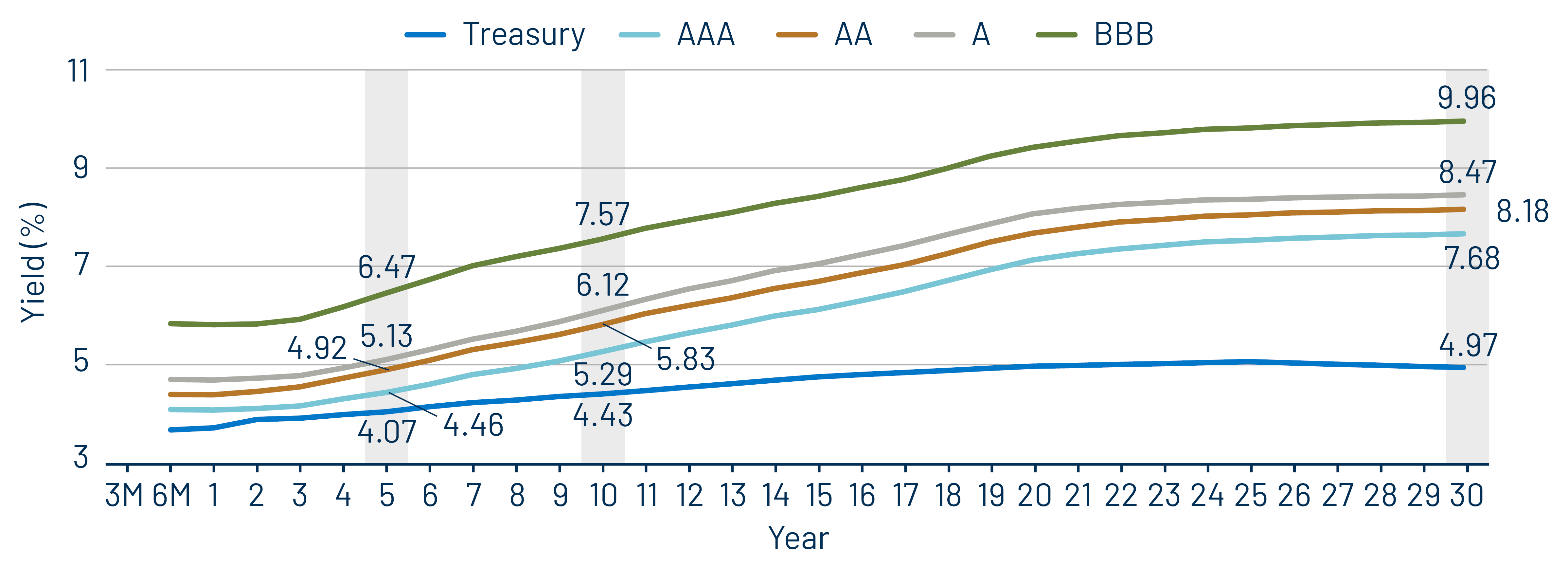

Municipal Credit Curves and Relative Value

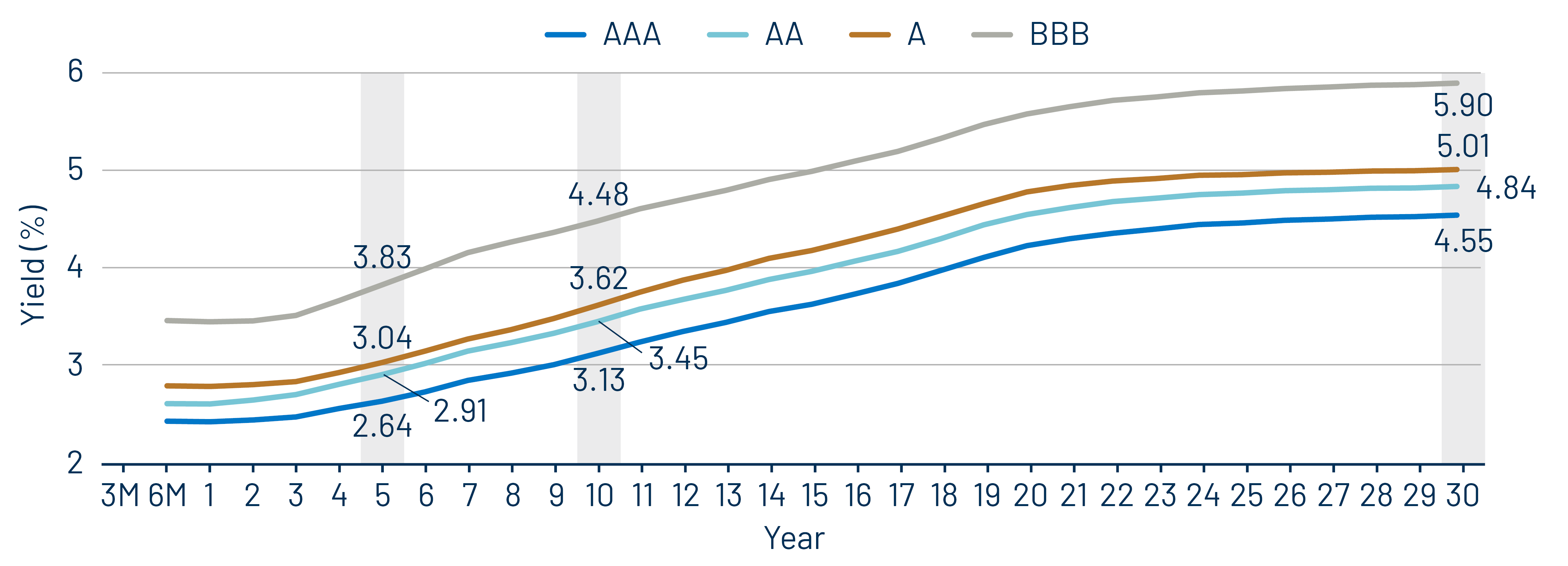

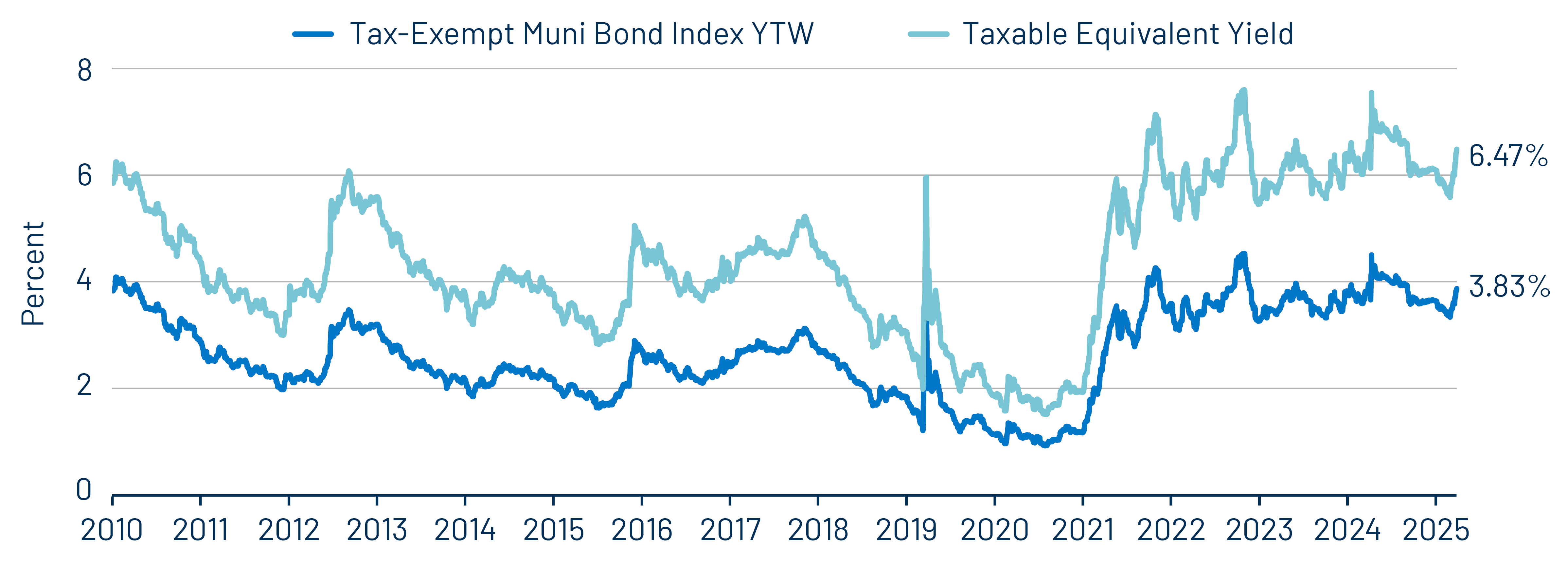

Theme 1: Municipal taxable-equivalent yields remain above historical averages.

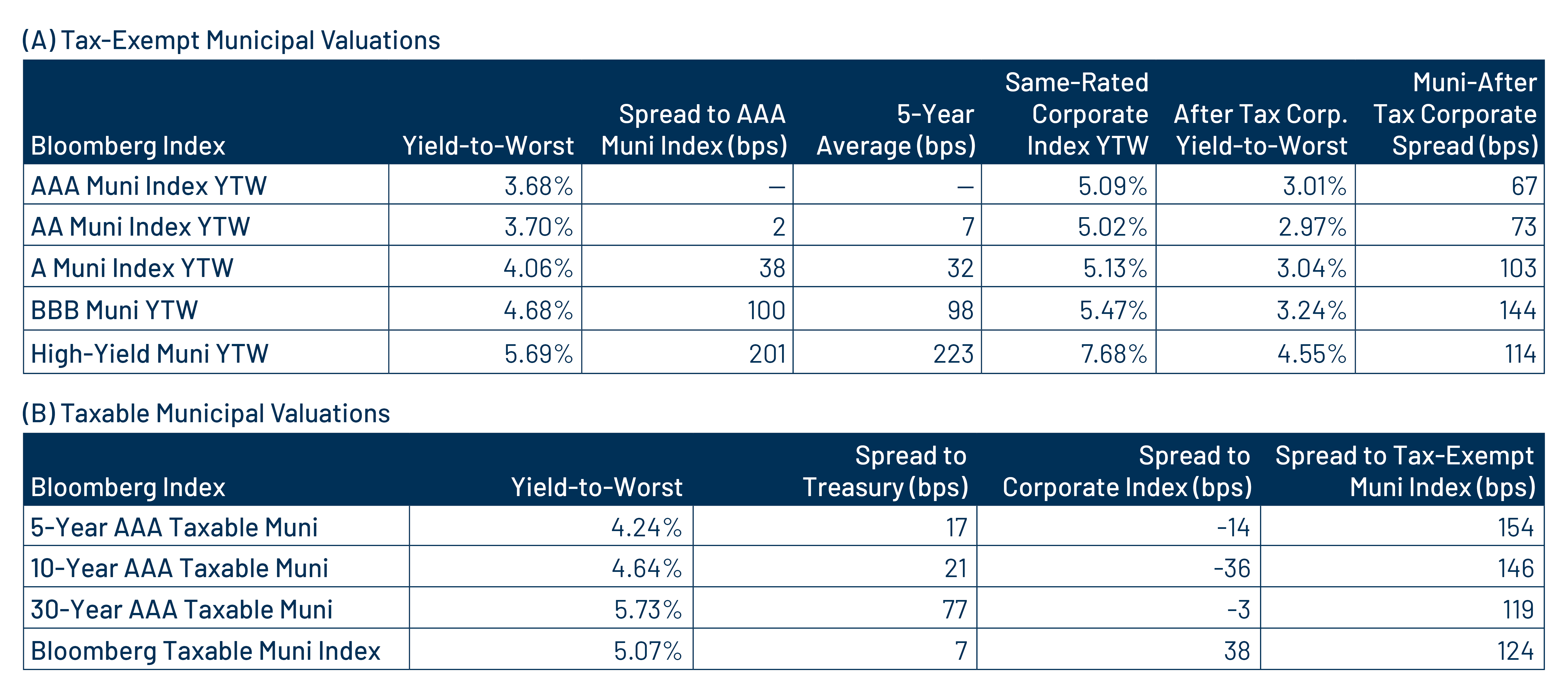

Theme 2: Munis offer attractive after-tax yield pickup vs. taxable alternatives.

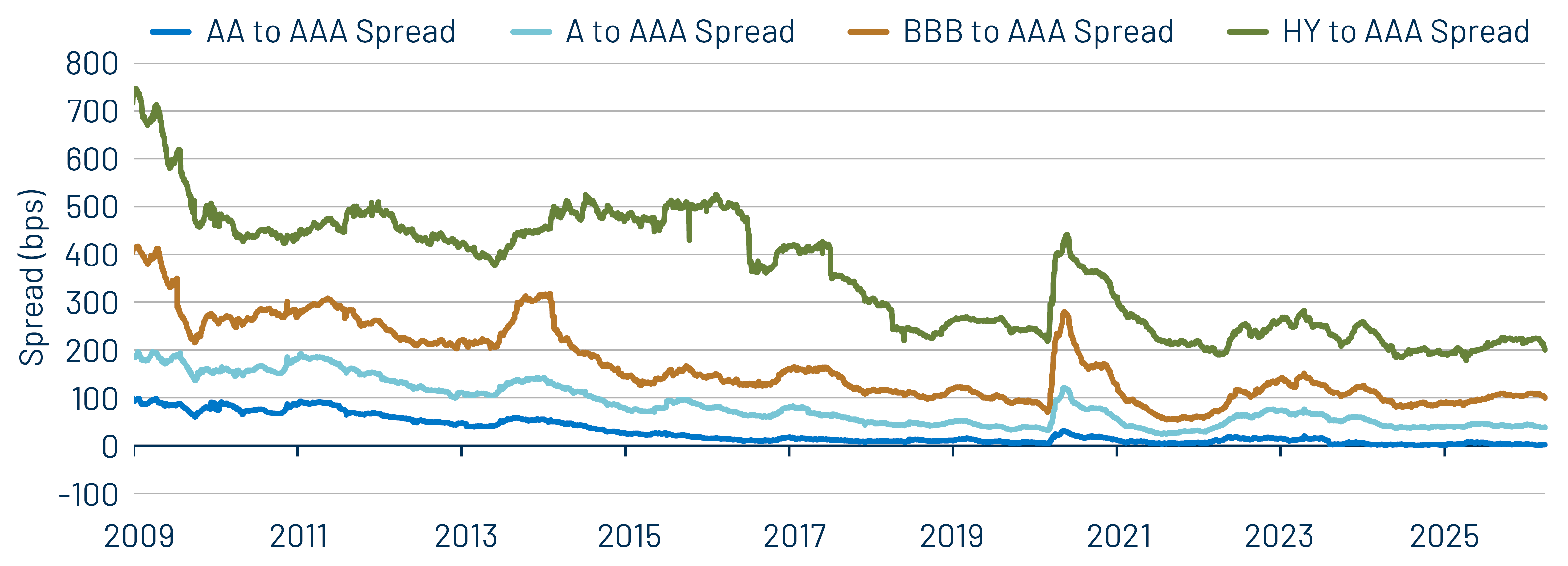

Theme 3: Historically tight municipal credit spreads underscore the importance of credit selection.