Macros, Markets and Munis

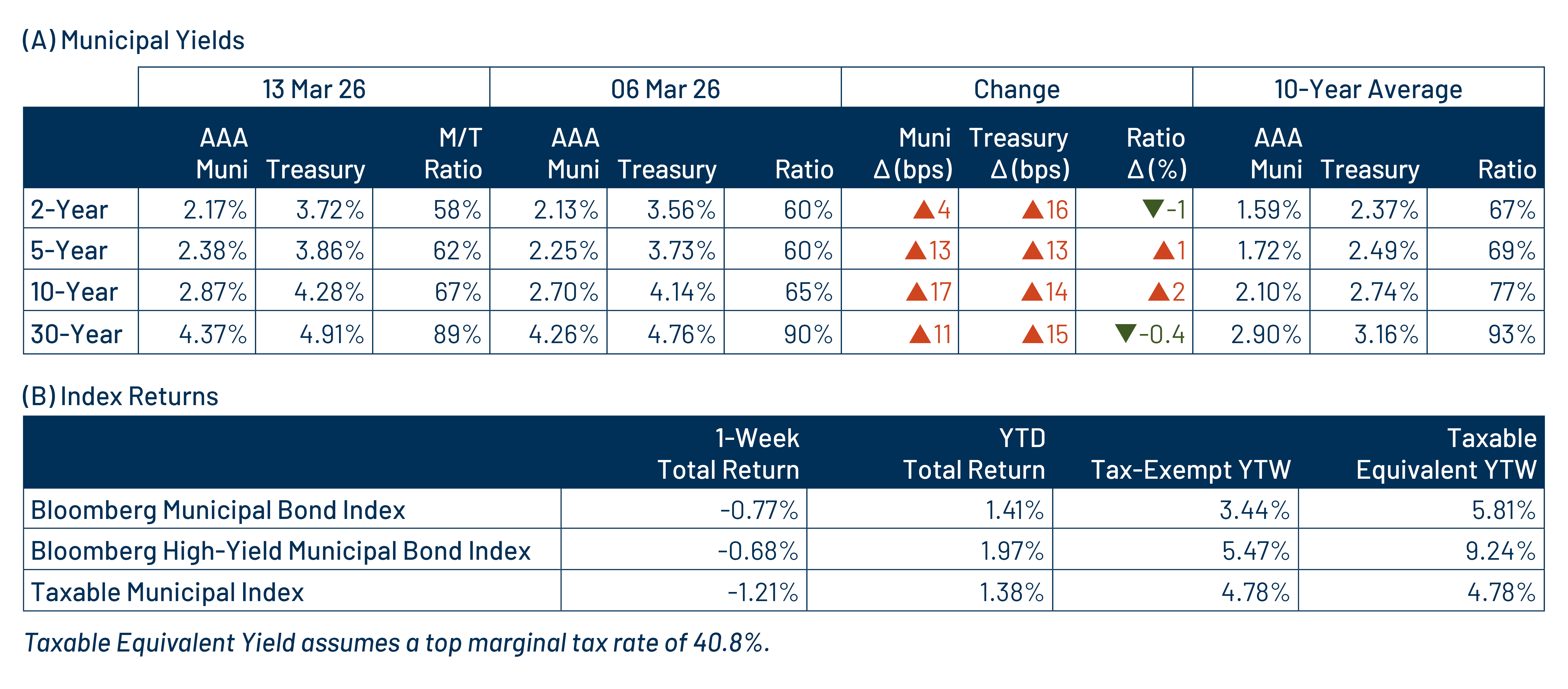

Municipals posted negative returns last week as heavy market volatility persisted amid ongoing geopolitical tensions with oil prices rising above $100 per barrel. On the economic front, 4Q25 GDP was revised lower, February’s Consumer Price Index (CPI) came in right in line with both the prior month and expectations of 2.5% year-over-year (YoY) while January’s core Personal Consumption Expenditures (PCE) Index edged modestly higher to 3.1%. Overall, the Treasury curve shifted 13-16 basis points (bps) higher across maturities. High-grade municipal yields moved in tandem with Treasuries, increasing 4-17 bps across the curve. Meanwhile, muni mutual funds recorded a 16th consecutive week of net inflows. This week we touch on elevated gas prepay issuance amid potential private credit concerns.

Muni Mutual Funds Sustain Strong Demand

Fund Flows ($612 million of net inflows): During the week ending March 11, weekly reporting municipal mutual funds recorded $612 million of net inflows, according to Lipper. Long-term, intermediate, and short-term categories recorded $216 million, $280 million and $76 million of inflows, respectively. Last week’s inflows marked the 16th consecutive week of positive flows, bringing year-to-date (YTD) inflows to $23 billion.

Supply (YTD supply of $103 billion; up 15% YoY): The muni market recorded $14 billion of new-issue supply last week, up 19% from the prior week. YTD new-issue supply of $103 billion is 15% higher than the prior year, with tax-exempt issuance up 17% YoY and taxable issuance down 15%, respectively. This week’s calendar is expected to decline to $11 billion. The largest deals include $1.2 billion Black Belt Energy (PNC) and $983 million NYC Water and Sewer transactions.

This Week in Munis: Gas Prepay

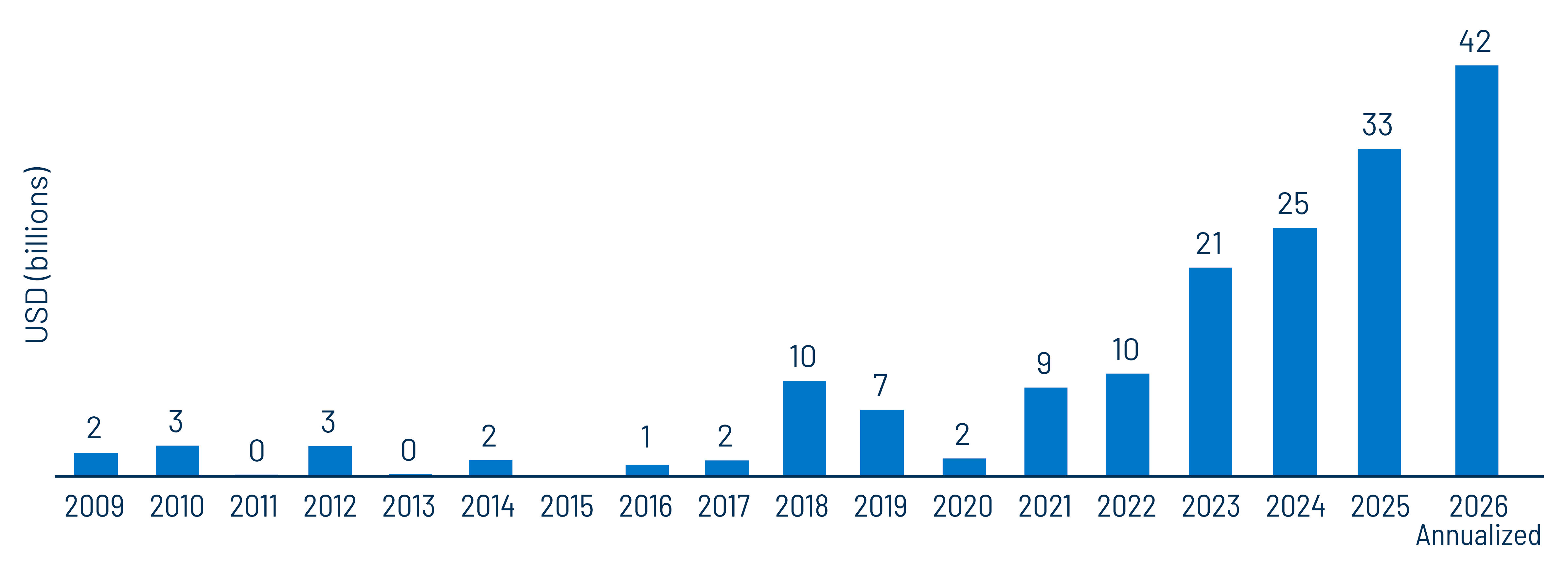

The gas prepay sector has experienced significant growth in recent years, further highlighted this week by a large new issuance involving PNC Bank. Gas prepay security structures provide municipal investors an opportunity to gain exposure to corporate-backed credit within the traditional tax-exempt municipal market. These bonds are typically issued by a municipal authority and facilitate the prepaid purchase of natural gas from a supplier, often a commodity trading arm of a large financial institution. As a result, the underlying credit support of gas prepay bonds generally reflects the credit quality of the participating financial institution rather than the issuing municipal entity.

Prior to 2022, annual issuance in the sector was generally below $10 billion, but has accelerated to an annualized pace of roughly $42 billion in 2026, supported in part by relatively attractive tax-exempt financing conditions. This growth has increased the sector’s presence in the Bloomberg Municipal Bond Index, rising from less than 2% in 2019 to over 5% today. The issuer composition within the sector has also expanded beyond traditional investment banks to also include insurance companies.

The expansion of the gas prepay market provides municipal investors with access to a broader and more diversified pool of issuers and the potential for incremental income relative to traditional state and local government bonds. However, evolving dynamics in private credit markets, particularly lending and liquidity pressures affecting financial institutions and insurers, could introduce additional volatility within the sector. Western Asset believes that active managers with integrated municipal and corporate credit expertise are well positioned to navigate these evolving credit dynamics and identify attractive opportunities for investors amid the elevated supply and potential volatility.

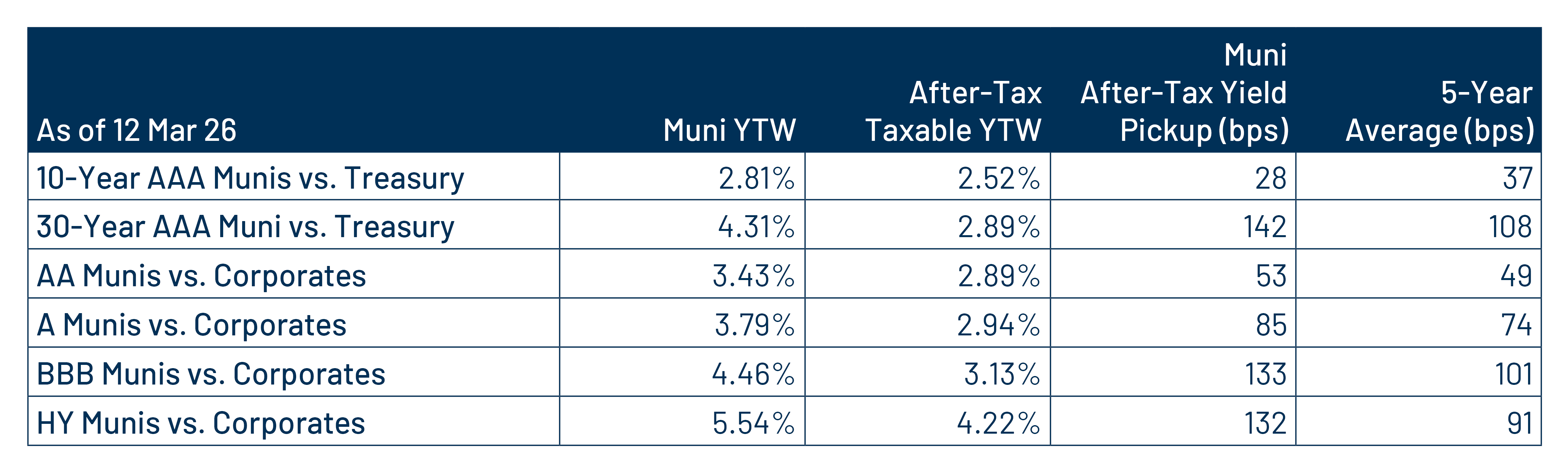

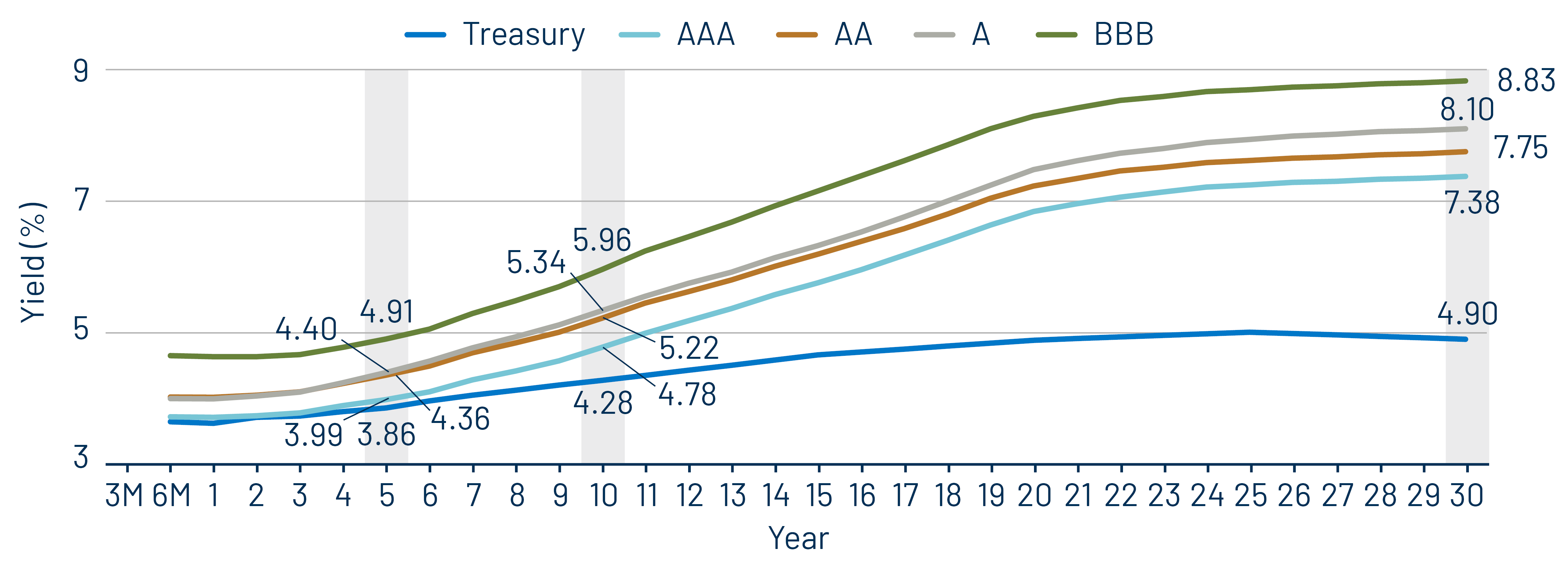

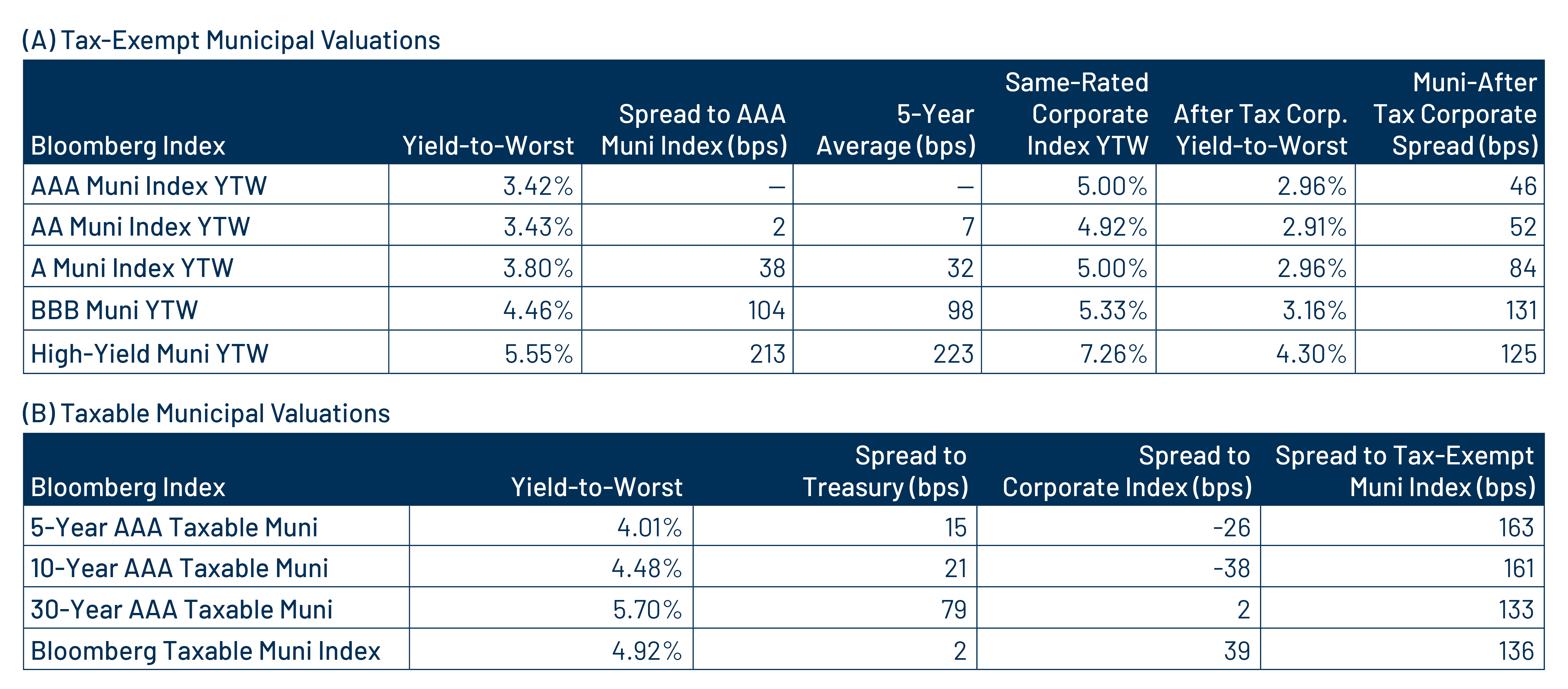

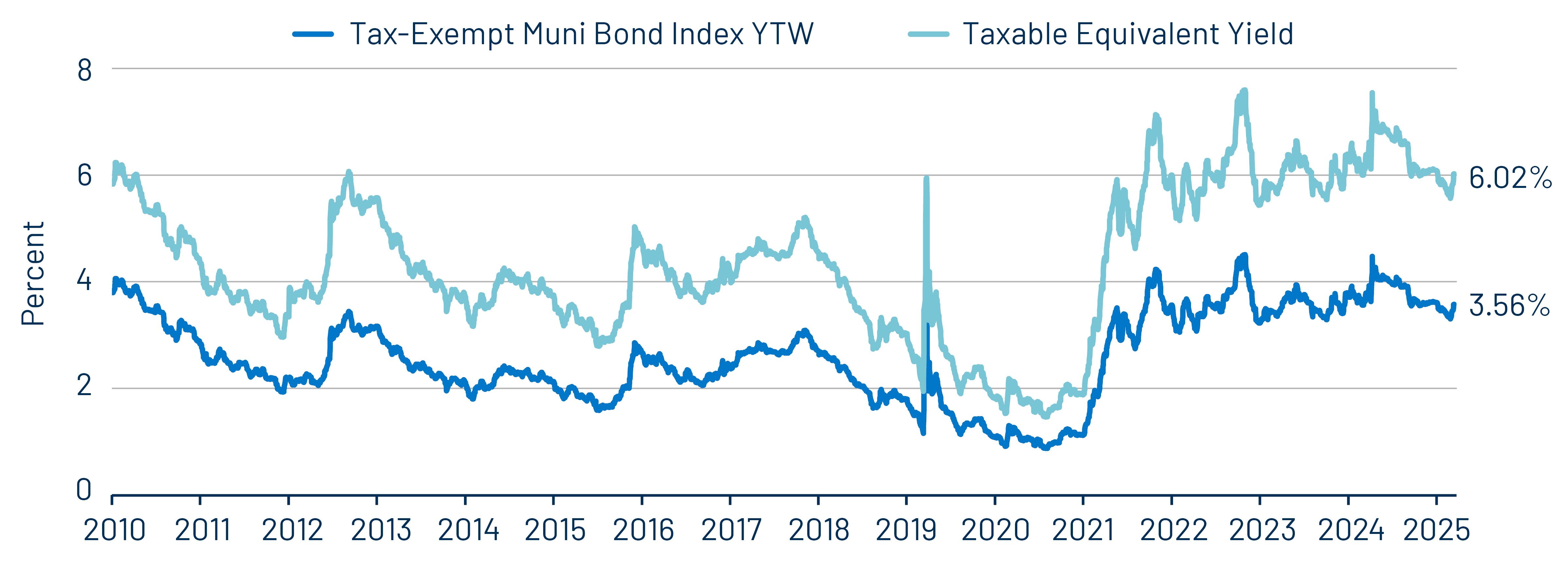

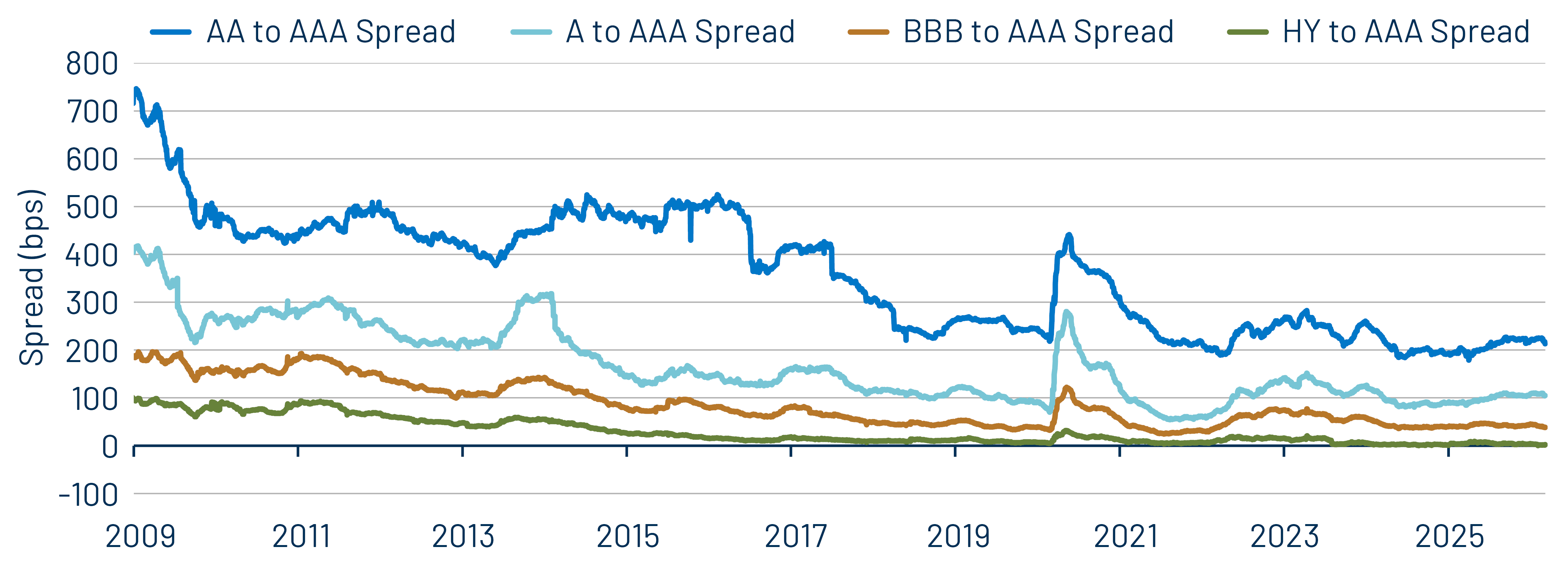

Municipal Credit Curves and Relative Value

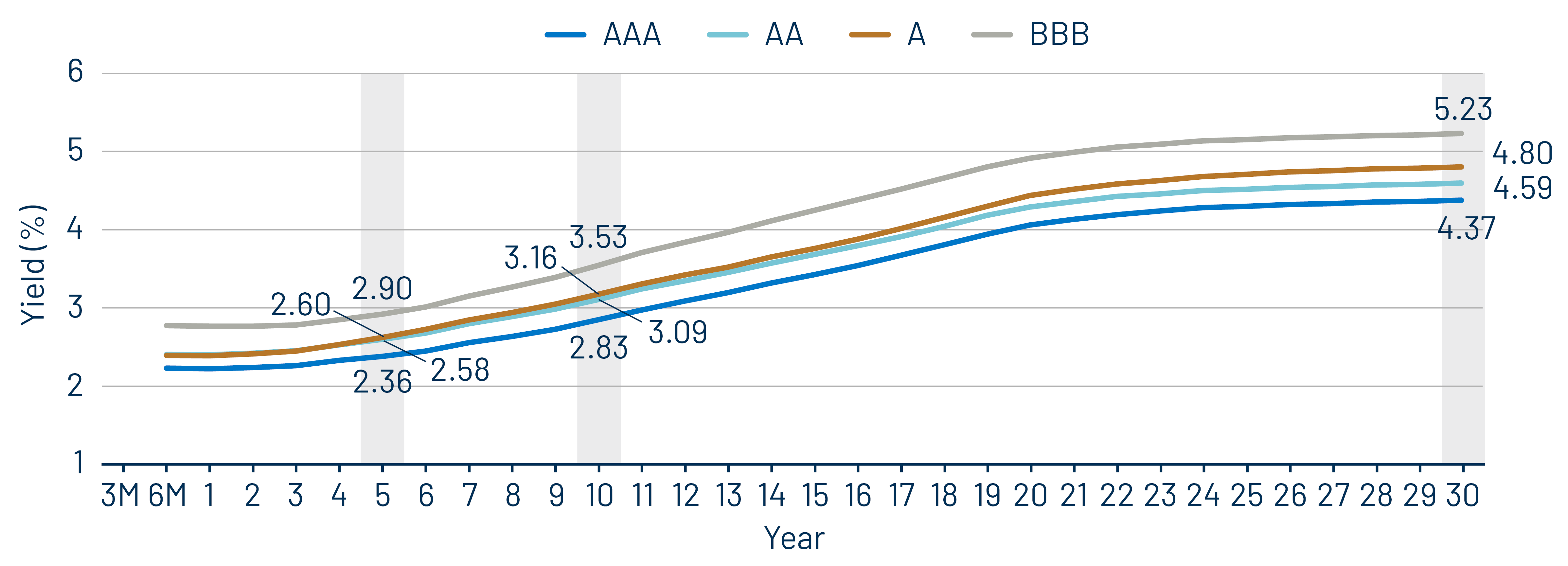

Theme 1: Municipal taxable-equivalent yields moved lower from recent highs, but remain above historical averages.

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration and lower-quality taxable alternatives.

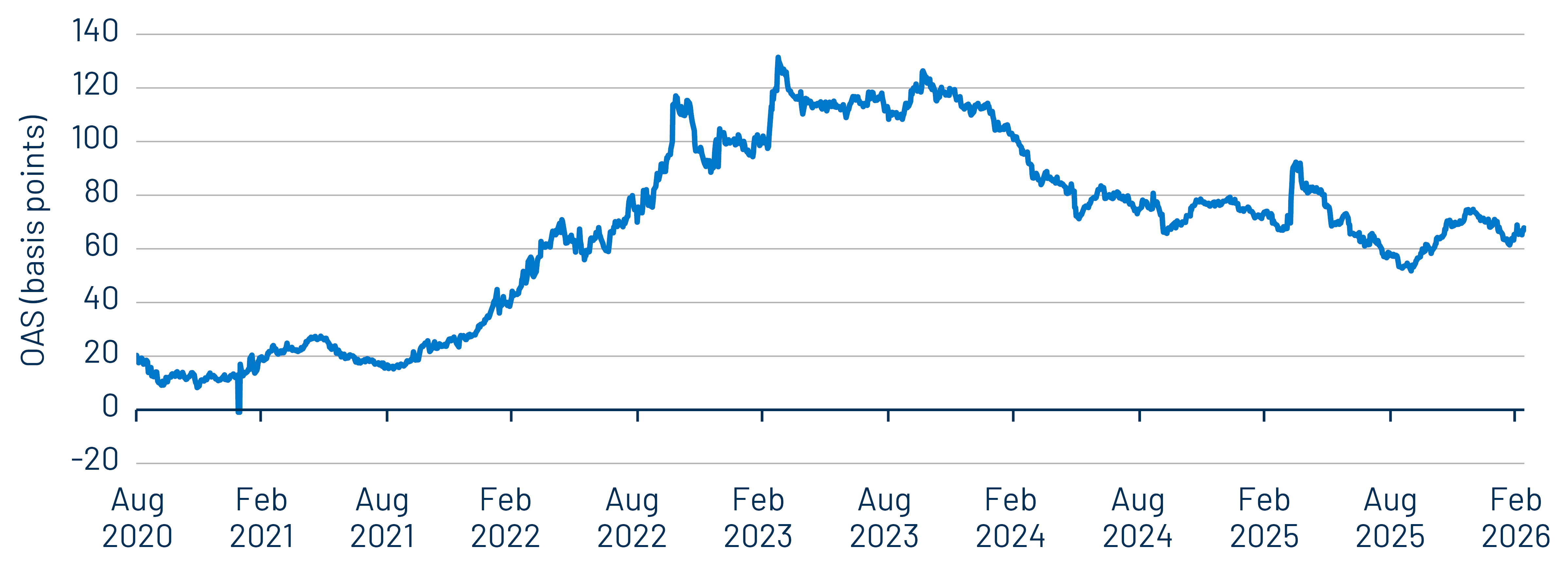

Theme 3: Historically tight municipal credit spreads underscore the importance of credit selection.