Macros, Markets and Munis

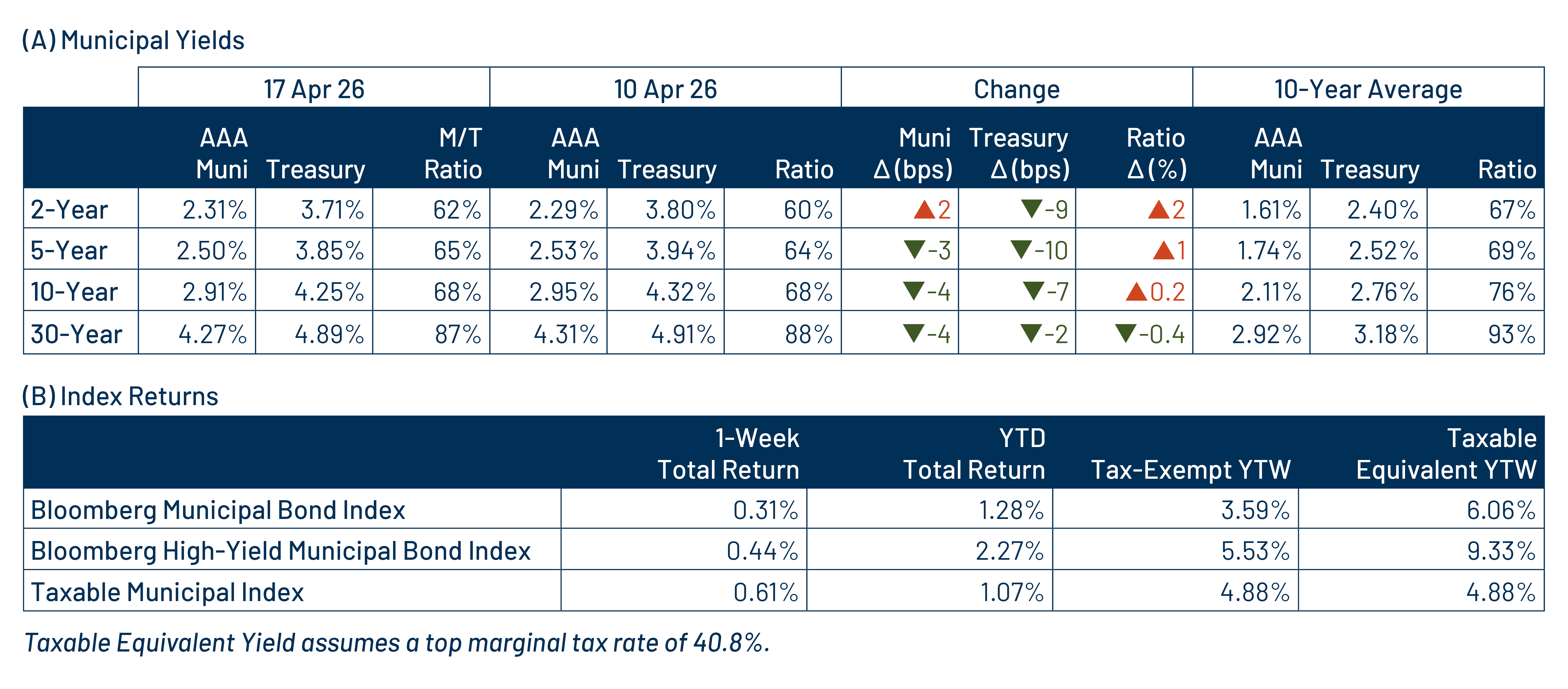

Municipals posted positive returns last week but underperformed Treasuries. Markets remained optimistic with a risk-on tone amid continued progress in trade negotiations and the opening of the Strait of Hormuz. On the economic data front, Producer Price Index data and initial jobless claims both came in below expectations. All told, the Treasury curve steepened, moving 9-10 basis points (bps) lower in shorter maturities and 2 bps lower further out on the curve. Municipals generally underperformed Treasuries amid fund outflows ahead of Tax Day and heavy supply conditions. This week we highlight late credit-cycle trends that have emerged in the muni market.

Technicals Soften Amid Tax-Day Outflows, Elevated Supply

Fund Flows ($427 million of net outflows): During the week ending April 15, weekly reporting municipal mutual funds recorded $427 million of net outflows, according to Lipper, likely due to Tax Day related redemptions. The long-term category recorded $116 million of inflows, while the short-term and intermediate categories recorded $533 million and $10 million of outflows, respectively. Last week’s outflows bring year-to-date (YTD) inflows to $28 billion.

Supply (YTD supply of $162 billion; up 22% YoY): The muni market recorded $18 billion of new-issue supply last week, up 80% from the prior week and the highest level of the year. YTD new-issue supply of $162 billion is 22% higher than the prior year, with tax-exempt issuance up 20% year-over-year (YoY) and taxable issuance up 58%, respectively. This week’s calendar is expected to decline to $12 billion. The largest deals include $1.1 billion New Jersey Health Care Facilities Authority and $750 million Texas Transportation Commission transactions.

This Week in Munis: Late-Cycle Signs

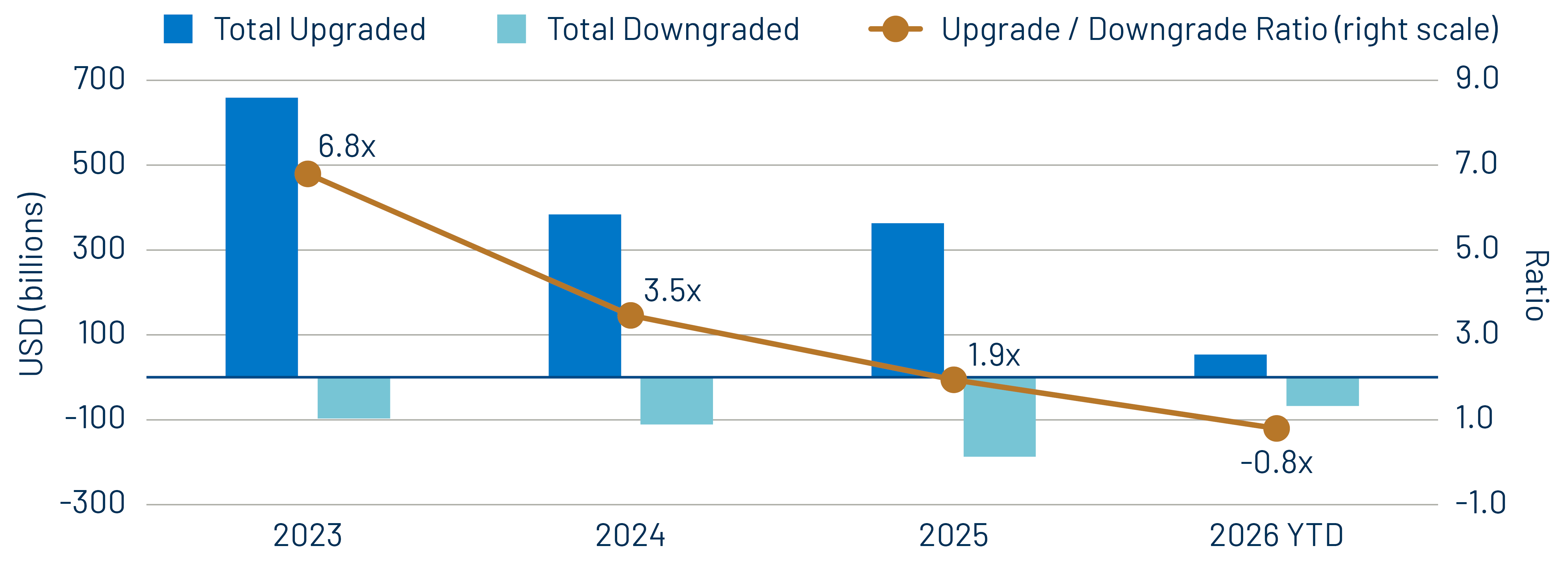

Municipal credit quality has experienced a strong tailwind following the pandemic recovery, as state and local governments maintained robust tax collections, supported in large part by federal aid to businesses and additional direct support to municipalities in the event of revenue shortfalls which ultimately did not materialize. As a result, upgrades significantly outpaced downgrades by 6.8x in 2023 and 3.5x in 2024, before moderating to 1.9x last year. So far this year, muni upgrade trends have further softened, with downgrades outpacing upgrades YTD and the upgrade-to-downgrade ratio declining to 0.8x.

The elevated pace of downgrades has been reflective of broader economic uncertainty that has begun to pressure select municipal budgets. Notably, Fitch downgraded the city of Chicago from A- to BBB+, while S&P and Moody’s lowered the city of New Orleans by one and two notches, respectively, to BBB+/Baa2. Common drivers of these downgrades include operating deficits, revenue uncertainty and strained liquidity. In addition to traditional investment-grade muni credit, several headline project finance issuers within the high-yield index have drawn headlines this year due to potential restructuring risks.

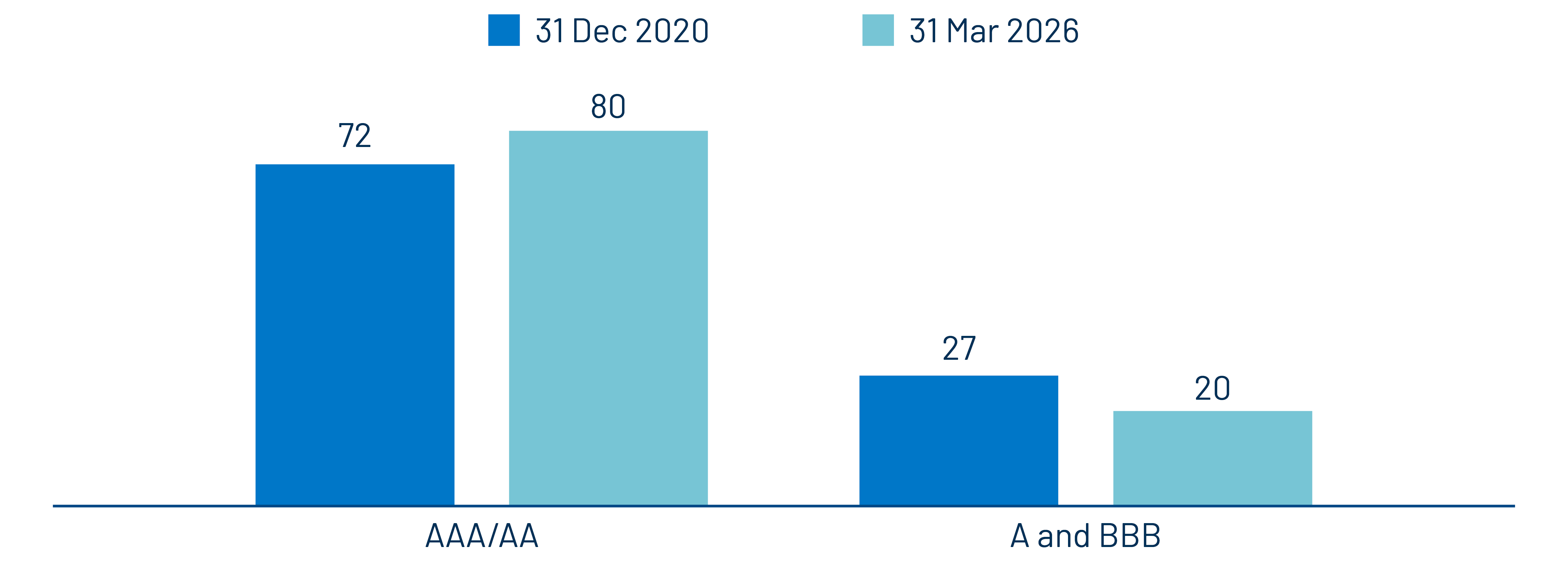

While the recent rating trend is notable, part of the shift in credit dynamics reflects the fact that many municipal issuers are already rated at or near rating capacity. Over 80% of investment-grade municipal debt is rated AA- or higher. While a maturing credit cycle may lead to downgrades and episodic price volatility for individual issuers, we expect the broader municipal market to remain resilient and maintain high overall credit quality. In an environment where downgrades may outpace upgrades, we expect active managers with robust credit research capabilities to be best positioned to capitalize on dislocations driven by credit-specific risks.

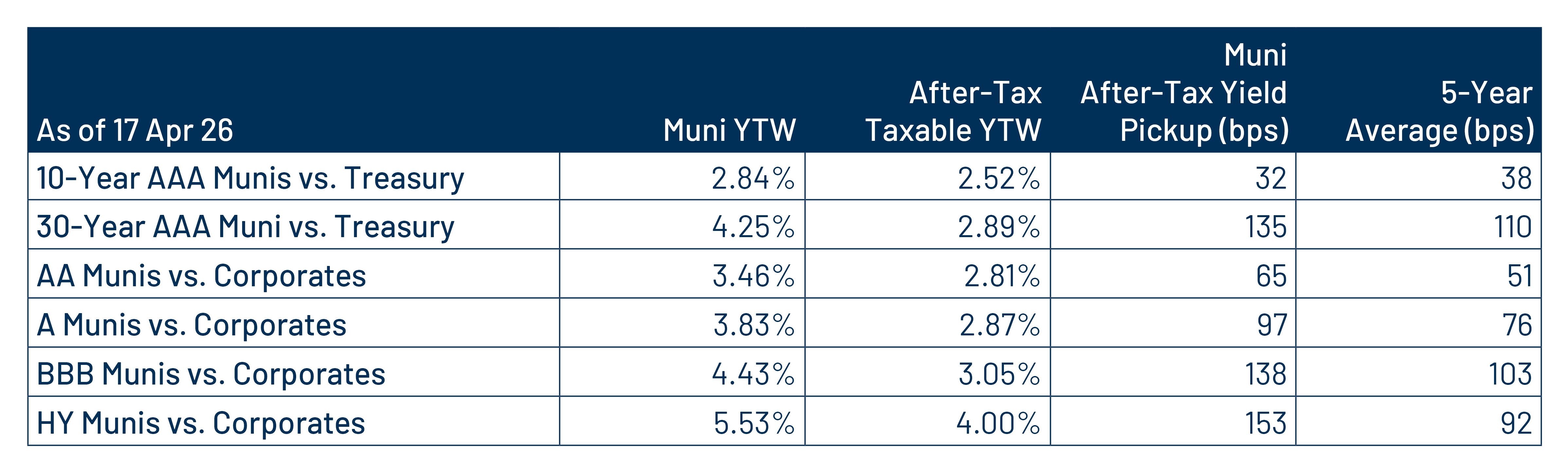

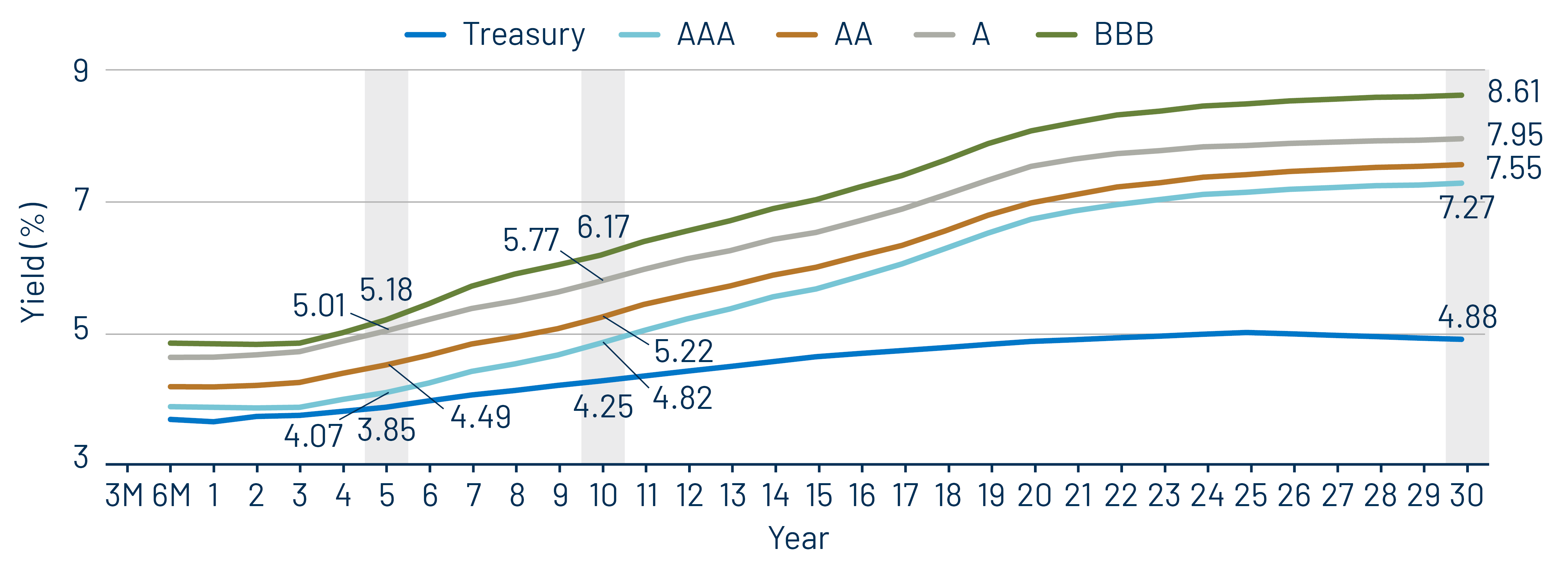

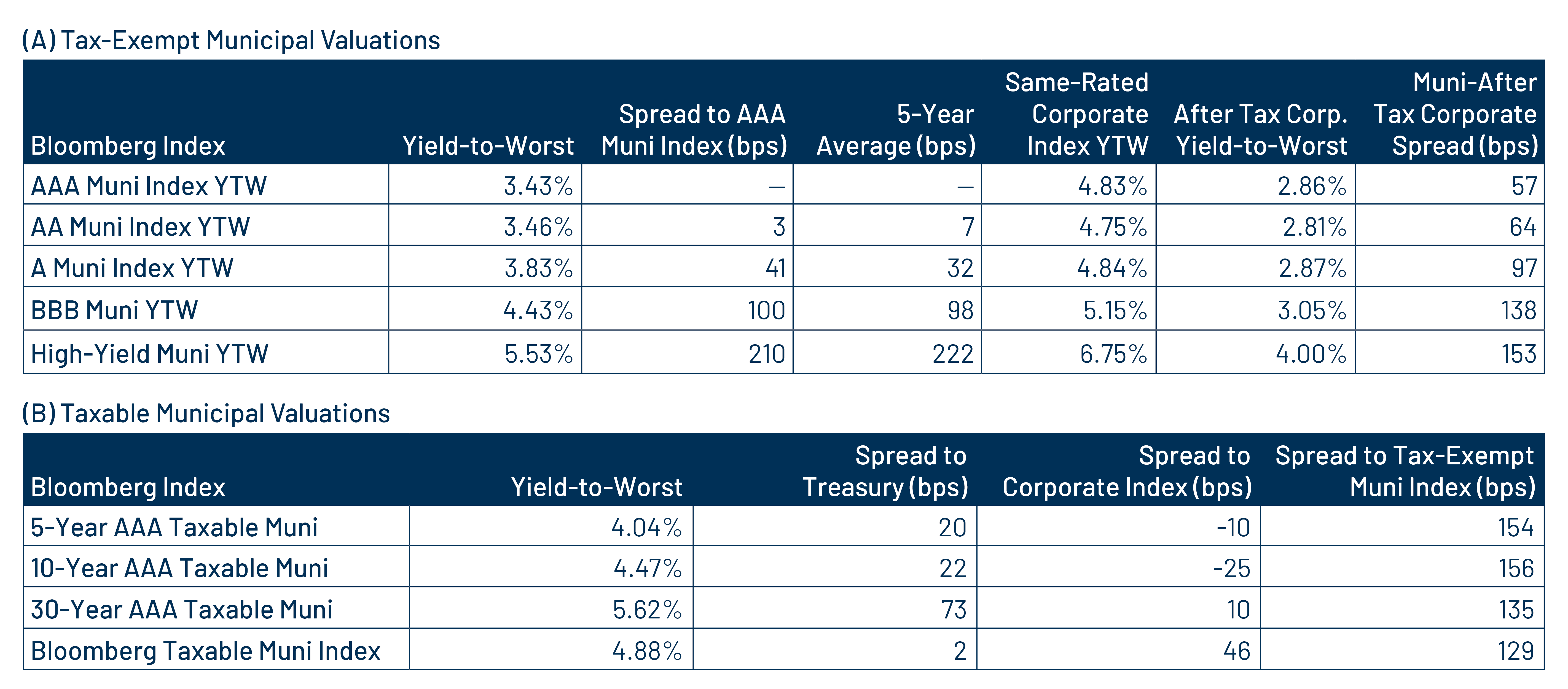

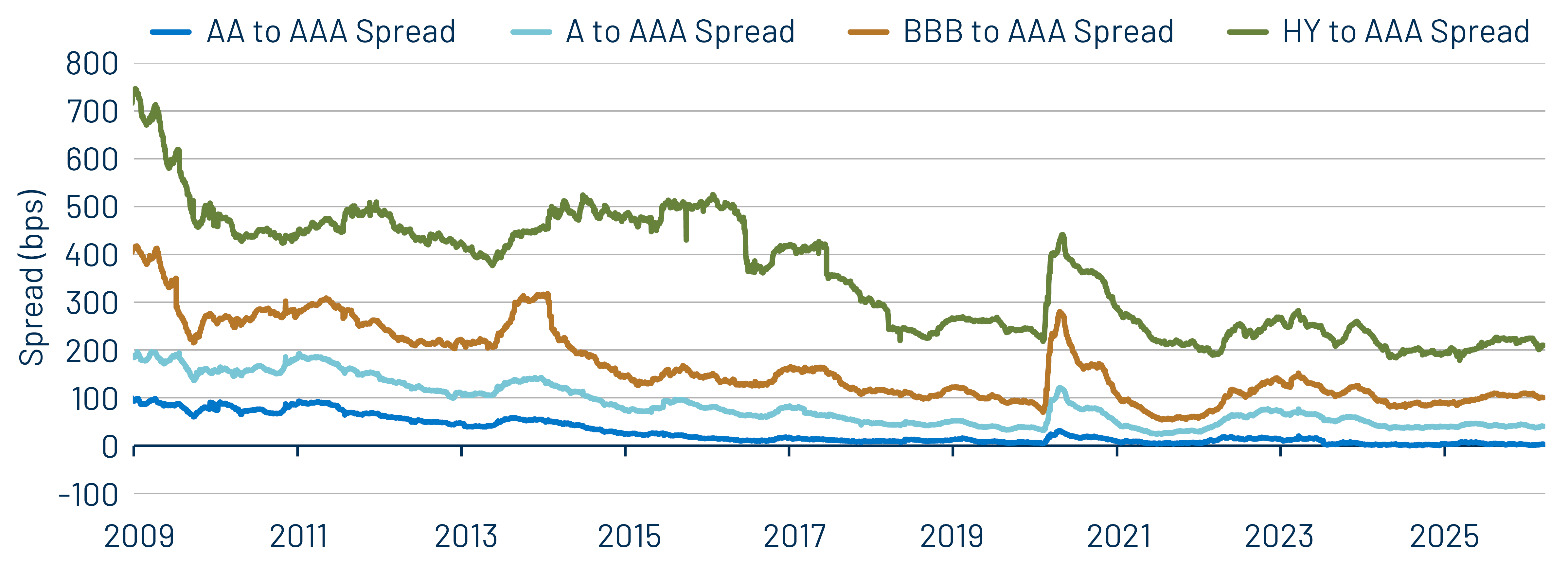

Municipal Credit Curves and Relative Value

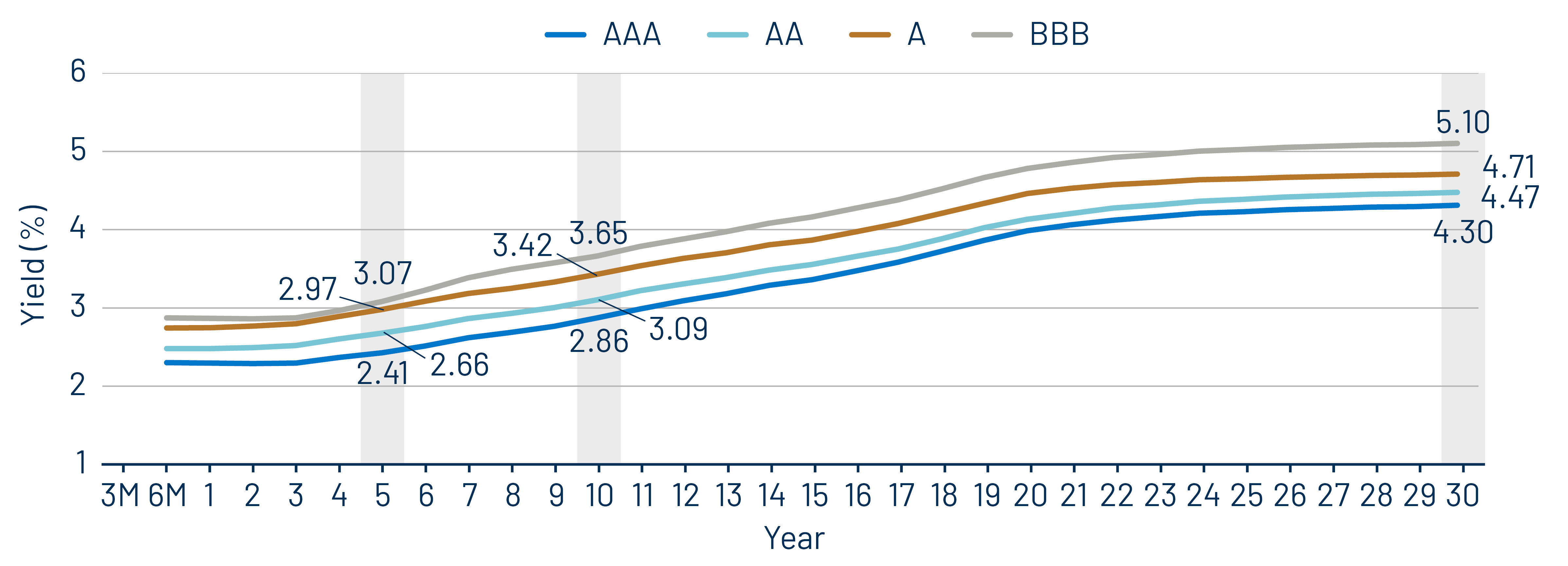

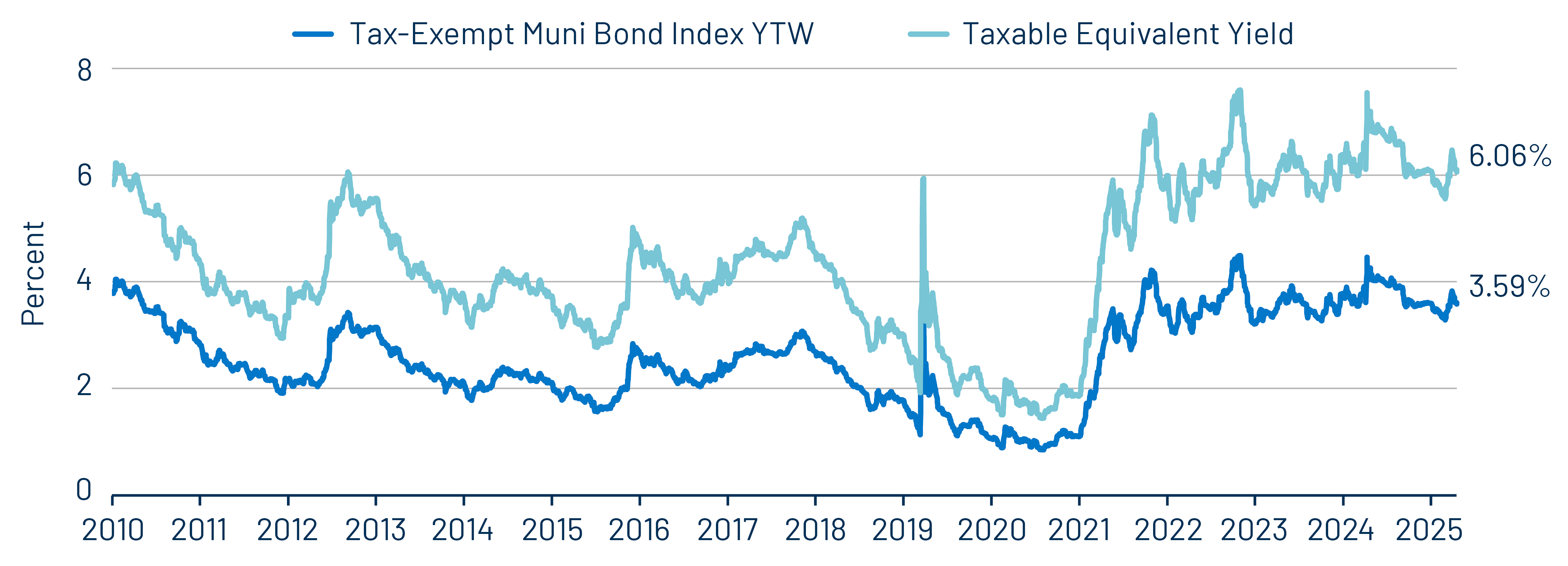

Theme #1: Municipal taxable-equivalent yields moved lower from recent highs, but remain above historical averages.

Theme #2: Munis offer attractive after-tax yield pickup vs. longer-duration and lower-quality taxable alternatives.

Theme #3: Historically tight municipal credit spreads underscore the importance of credit selection.