Macros, Markets and Munis

Municipals posted positive returns last week and outperformed Treasuries. As geopolitical tensions persisted, economic data was mixed. Nonfarm payrolls remained resilient, declining from the prior month but coming in nearly double expectations at 115,000 jobs, while the unemployment rate held steady at 4.3%. In contrast, the University of Michigan consumer sentiment fell to record lows. Meanwhile, the Treasury curve flattened with yields declining across most maturities but rising at the short end. High-grade municipals outperformed, with yields moving lower across the curve as demand conditions improved. Overall muni supply and demand remained elevated. This week we touch on the New York budget agreement reached last week.

Demand Improved as Supply Continues to Build

Fund Flows ($1.8 billion of net inflows): During the week ending May 6, weekly reporting municipal mutual funds recorded $1.8 billion of net inflows, according to Lipper. The long-term category recorded $1.2 billion of inflows, the intermediate category reported $363 million of inflows and the short-term category recorded $115 million of net inflows. Last week’s inflows bring year-to-date (YTD) inflows to $33 billion.

Supply (YTD supply of $199 billion; up 15% YoY): The muni market recorded $15 billion of new-issue supply last week, up 48% from the prior week. YTD new-issue supply of $199 billion is 15% higher than the prior year, with tax-exempt issuance up 16% year-over-year (YoY) and taxable issuance up 8%, respectively. This week’s calendar is expected to remain elevated at $14 billion. Largest deals include $1.2 billion New York State Dormitory Authority and $1.1 billion Atlanta Water and Sewer transactions.

This Week in Munis: New York Ends Impasse

Last week, NY Governor Kathy Hochul announced that New York state reached agreement on its FY2027 budget, one month after the start of the fiscal year. The budget is expected to be signed into law next week and would mark the latest adoption since 2010. The $268 billion plan represents a 5.5% increase in spending from the prior year and includes notable increases in education spending and school aid. Positively, the budget is supported by stronger than expected tax collections and maintains healthy reserves. However, the state faces reduced federal aid, contributing to projected out-year gaps for FY2028-FY2030 that will need to be addressed.

Key issues that delayed the budget included a proposed second-home tax on properties valued above $5 million, immigration enforcement and housing reform. The finalized second-home tax features a graduated marginal rate starting at 0.5% on $5 million of market value and rising to 4% for homes exceeding $25 million. It is expected to generate approximately $500 million in annual revenue for New York City and serves as a concession to support the city’s tax base and mayor’s agenda, but the budget does not include increases to individual or corporate income taxes that Mayor Zohran Mamdani originally advocated.

Despite the delayed budget and related policy headlines, the Bloomberg New York Municipal Bond Index has outperformed the broader municipal market YTD and Western Asset believes New York securities offer attractive relative value. The New York index offers higher average yields (3.70%) than the national index (3.66%), and when factoring in high state, and potentially city tax rates, this translates to taxable-equivalent yields of up to 8.33% for high-income earners versus 6.18% for national municipal investors. While policy trends targeting high earners may drive headline volatility and concerns around tax-base migration, the budget process underscores the checks and balances across city and state policymaking. Western Asset expects resilient economic growth to continue supporting wealth creation in key economic centers underpinning New York’s overall credit profile.

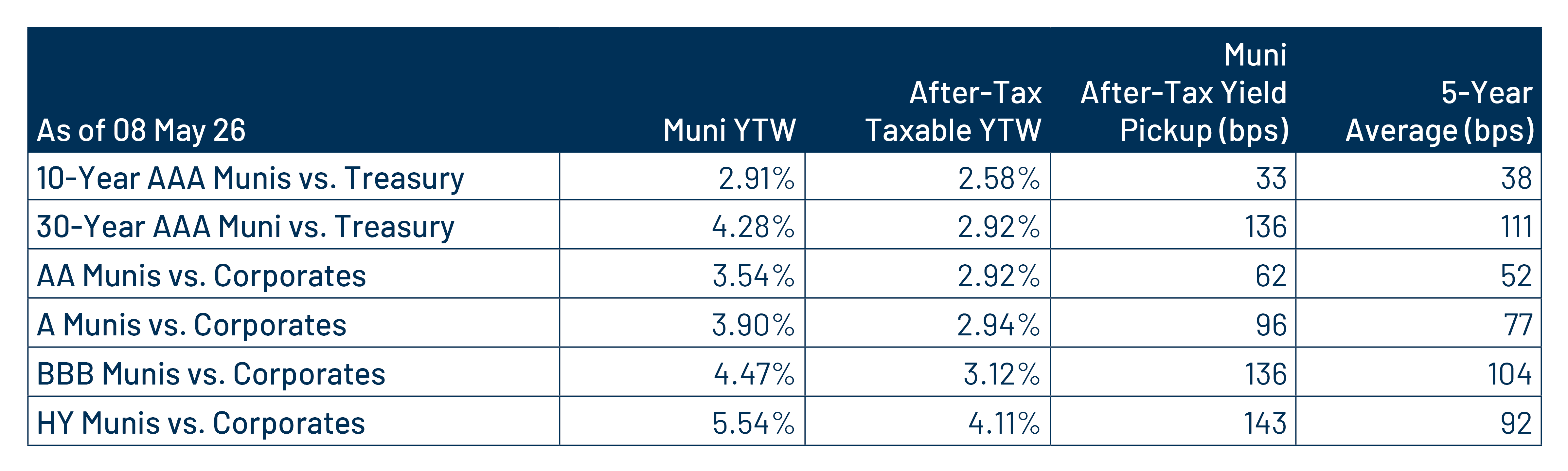

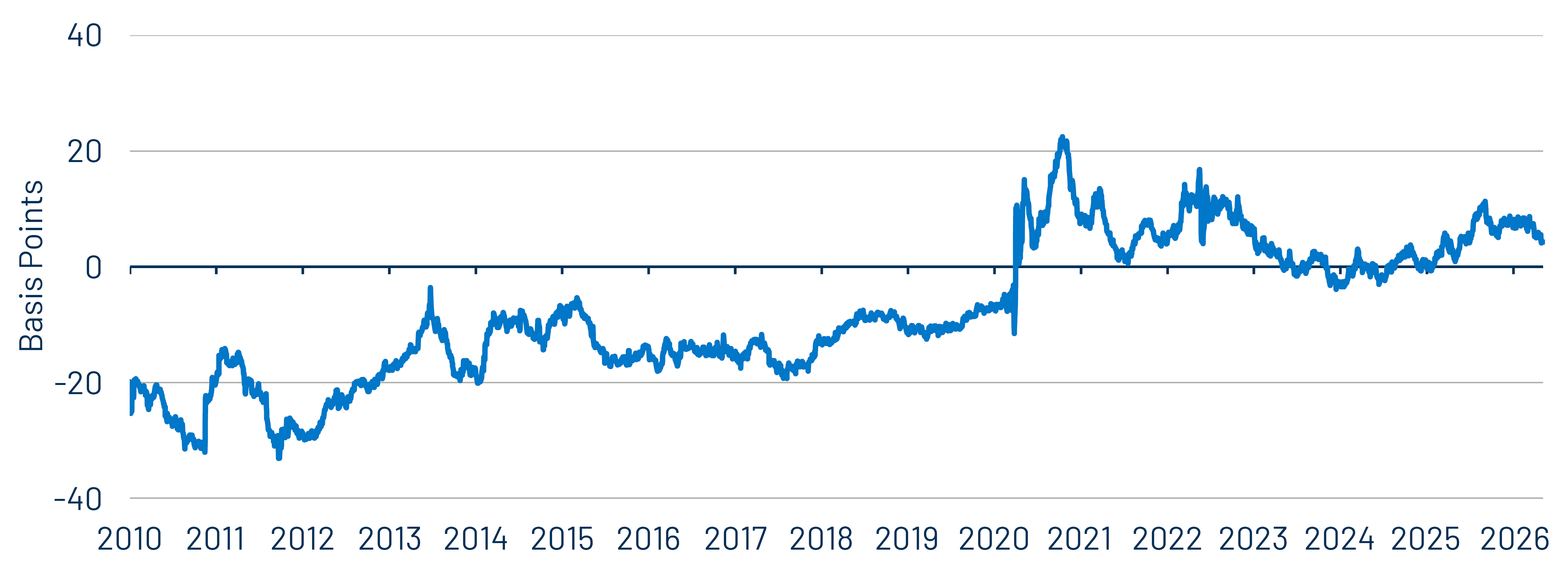

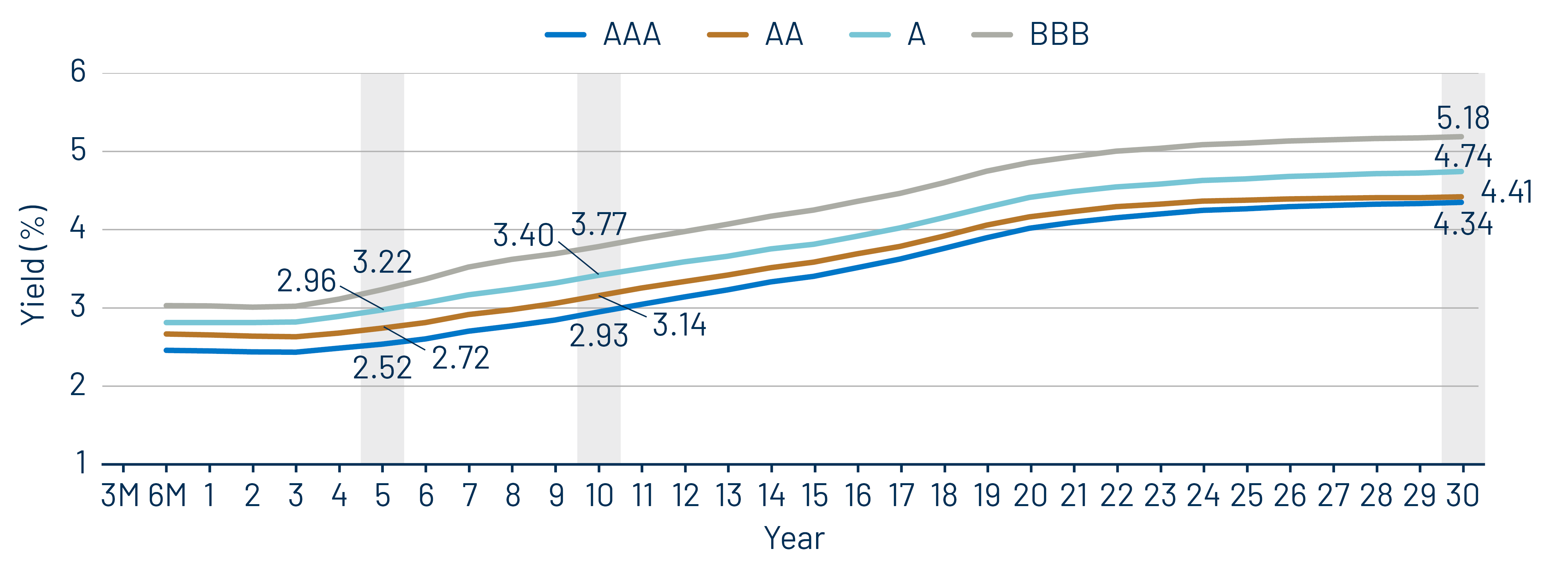

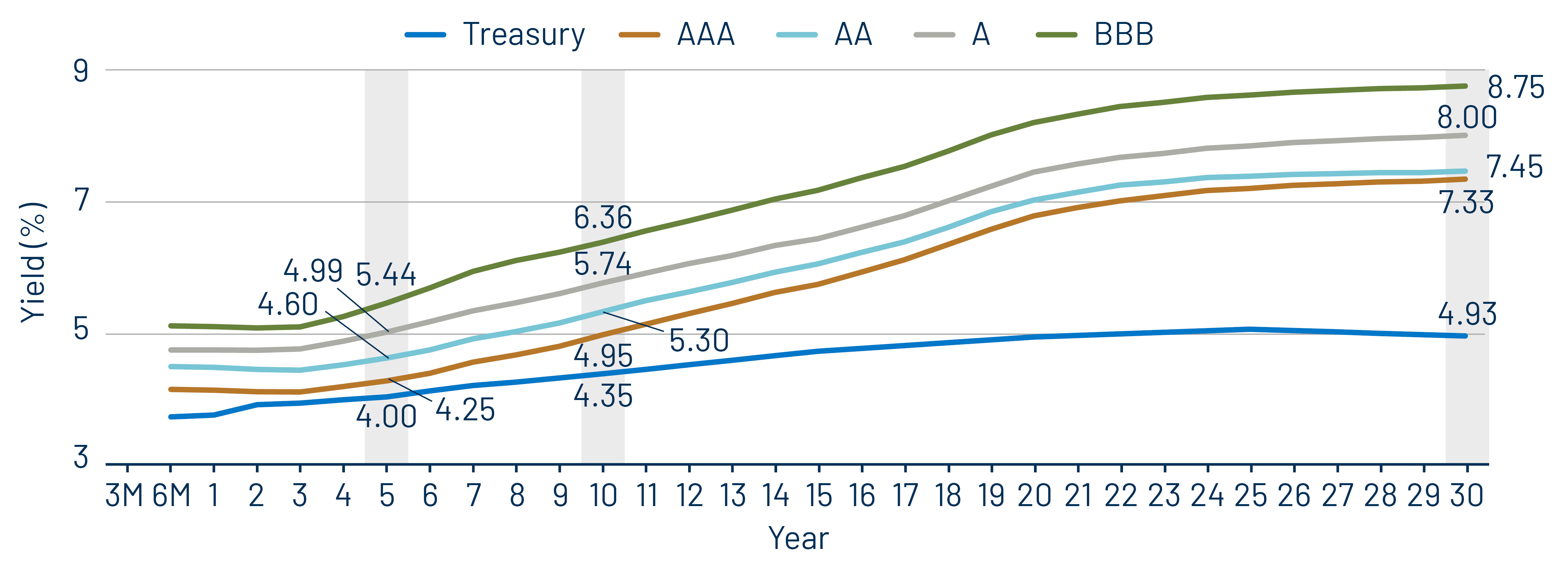

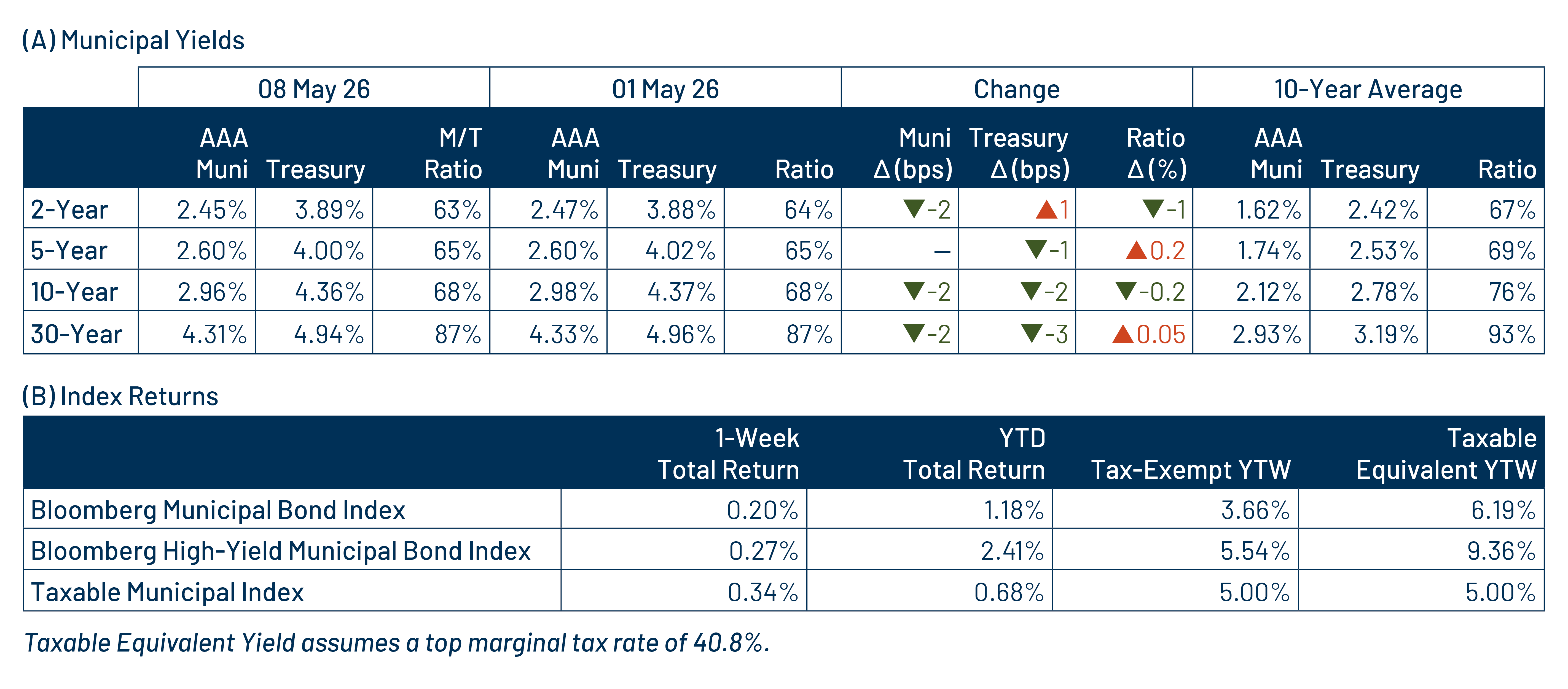

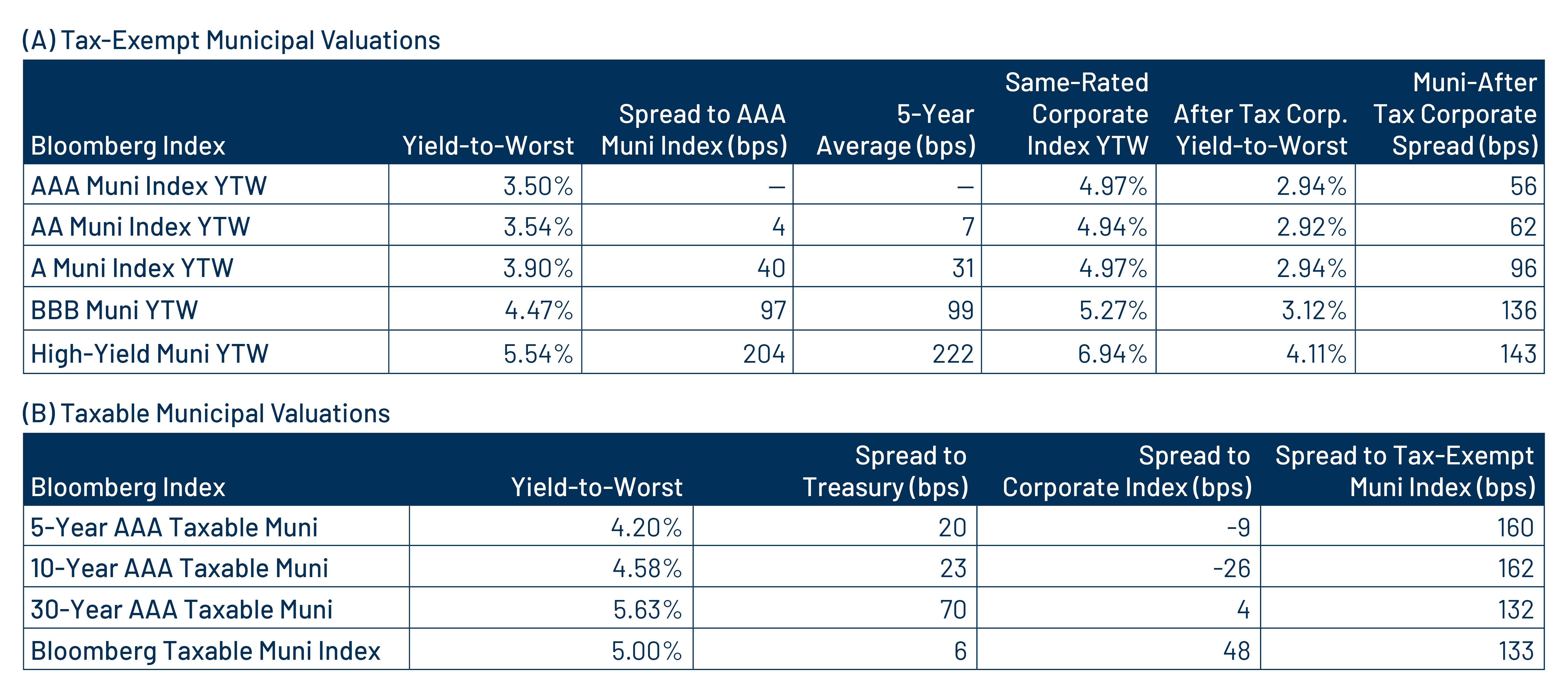

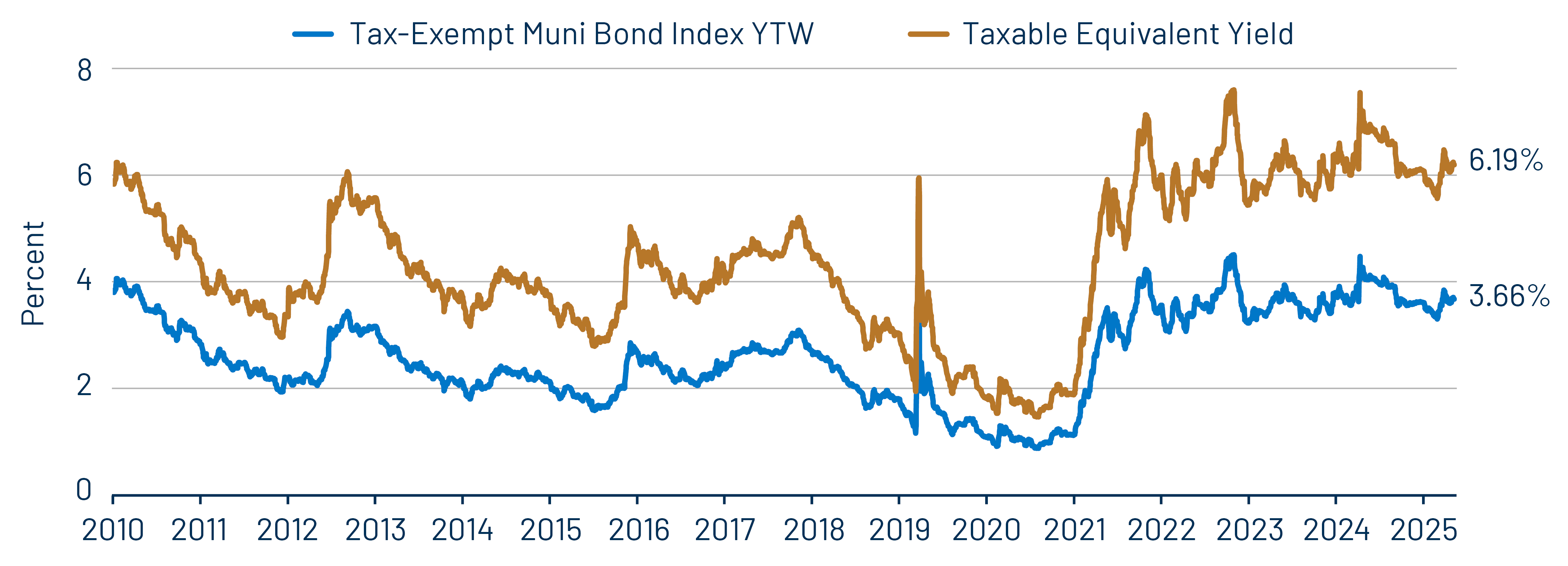

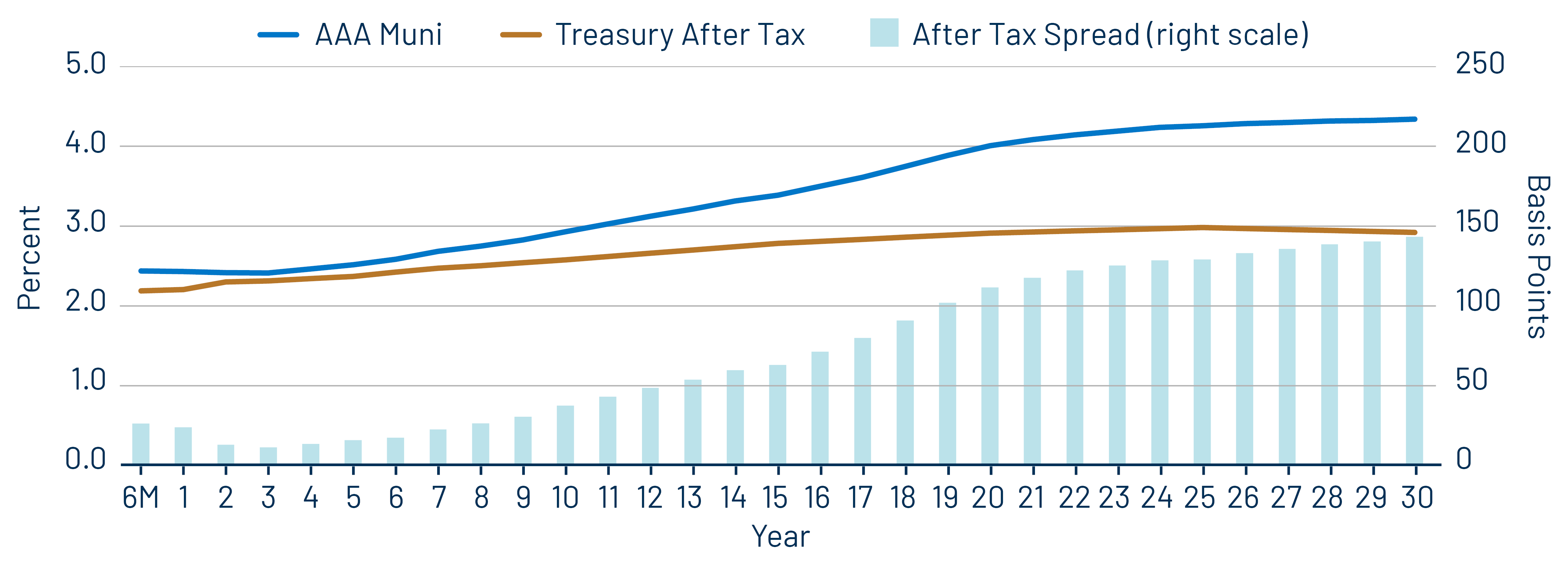

Municipal Credit Curves and Relative Value

Theme 1: Municipal taxable-equivalent yields moved lower from recent highs, but remain above historical averages.

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration and lower-quality taxable alternatives.

Theme 3: The muni curve remains steep and offers relative value in longer maturities.