Macros, Markets and Munis

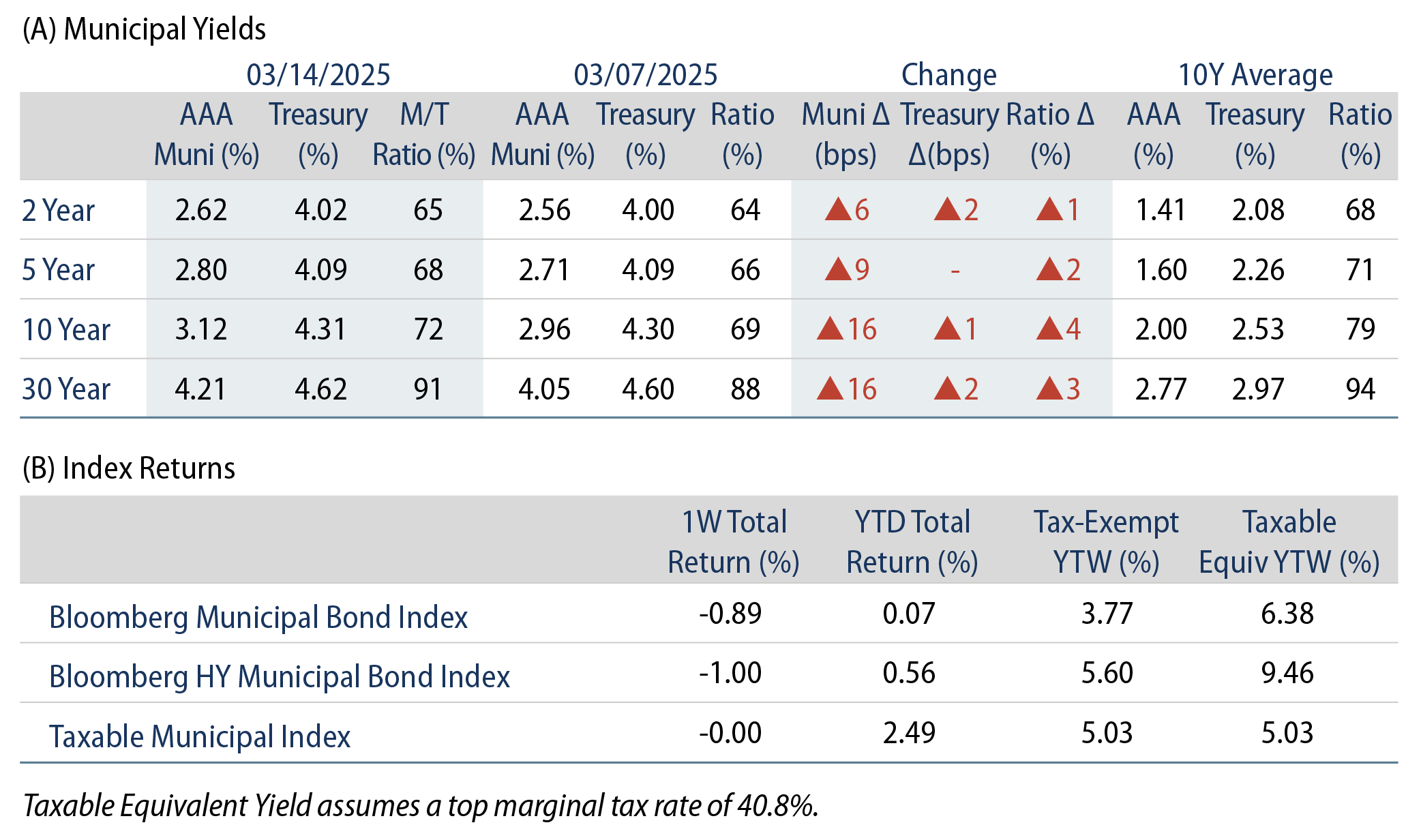

Munis posted negative returns last week as Treasury yields moved 6 to 16 basis points (bps) higher due to a greater consensus taking shape that the Federal Reserve (Fed) will be unlikely to cut rates this week or during its May meeting. Muni yields moved higher in sympathy with Treasuries but outperformed over the week. Risk sentiment remained weak amid ongoing tariff rhetoric and growth concerns. From an economic data perspective, January job openings came in higher than expected, the February Consumer Price Index (CPI) came in below expectations and declined to 2.8%, and consumer sentiment data moved lower. Meanwhile, muni demand turned negative following seven consecutive weeks of inflows. This week we highlight historical municipal market reactions to recessionary environments.

Demand Weakens as Funds Post Outflows

Fund Flows (down $373 million): During the week ending March 12, weekly reporting municipal mutual funds recorded $373 million of net outflows, according to Lipper. Long-term funds recorded $425 million of outflows, intermediate funds recorded $30 million of inflows and high-yield funds recorded $107 million of inflows. Last week’s outflows broke a seven-week streak of inflows and led year-to-date (YTD) inflows lower to $10 billion.

Supply (YTD supply of $103 billion; up 41% YoY): The muni market recorded $11 billion of new-issue supply last week, down from the prior week. YTD, the muni market has recorded $103 billion of new issuance, up 41% year-over-year (YoY). Tax-exempt and taxable issuance are each up 41%, though tax-exempt issuance has comprised the vast majority (95%) of YTD supply. This week’s calendar is expected to tick lower but remain elevated at $10 billion. The largest deals include $3 billion Dormitory Authority of the State of New York and $1.1 billion Metropolitan Transportation Authority transactions.

This Week in Munis: Recessions and Munis

Recession fears spiked last week as tariff policy and austerity measures drew concern across markets. Equities sold off amid the risk-off sentiment, with the S&P 500 falling 3.9% YTD and the Nasdaq falling 6.1% YTD. Notably, the Atlanta Fed GDPNow indicator declined to as low as -2.8% to start the month, marking the lowest level since the 2020 pandemic drawdowns.

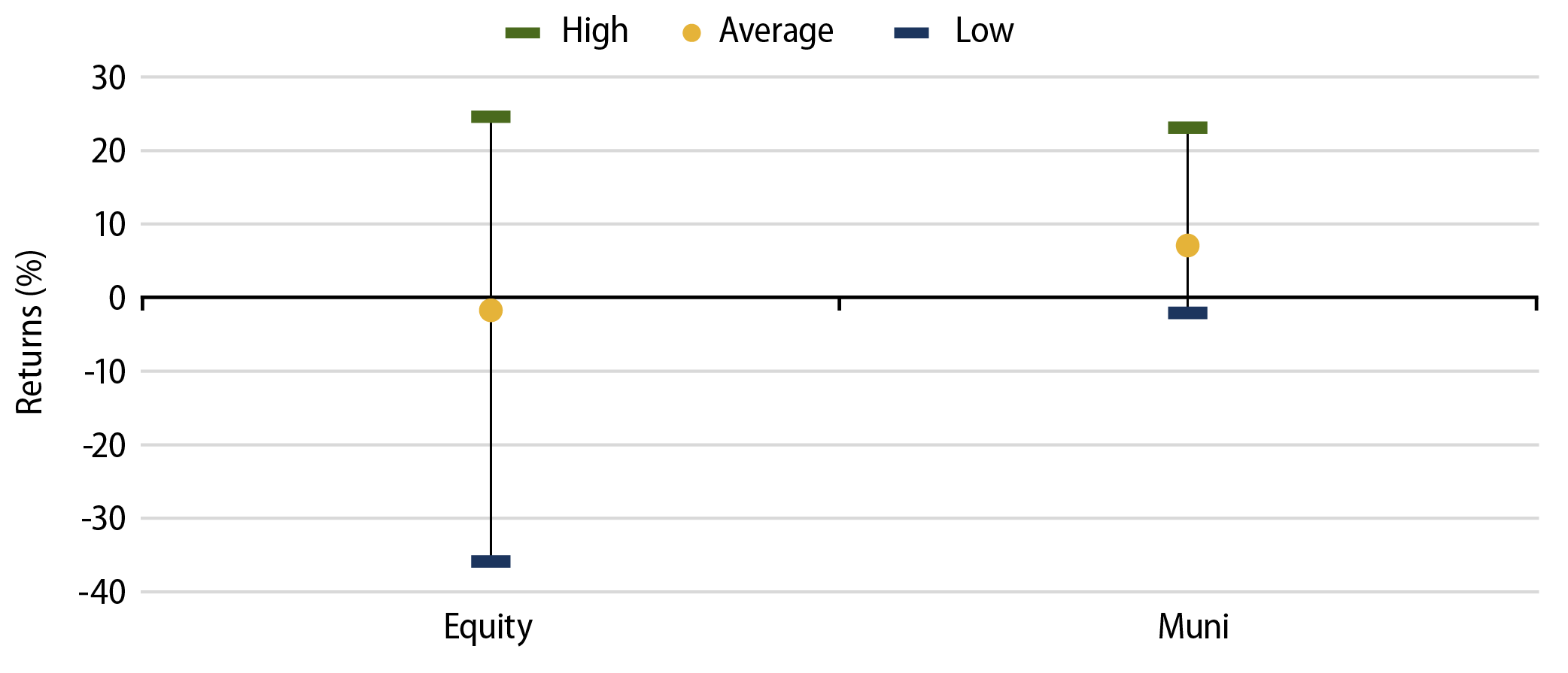

Over the past five recessionary periods, municipals have exhibited attractive risk-adjusted performance compared to equities. When comparing the returns of the Bloomberg Municipal Bond Index to the S&P 500 Index, municipals posted positive returns on average (+7.2%), while equity returns delivered average negative returns (-1.2%). Meanwhile, the maximum drawdown for equities over these periods was 35%, compared to the -1.9% return for the Bloomberg Municipal Bond Index, highlighting the potential for relative stability and resilience of municipal bonds during economic downturns.

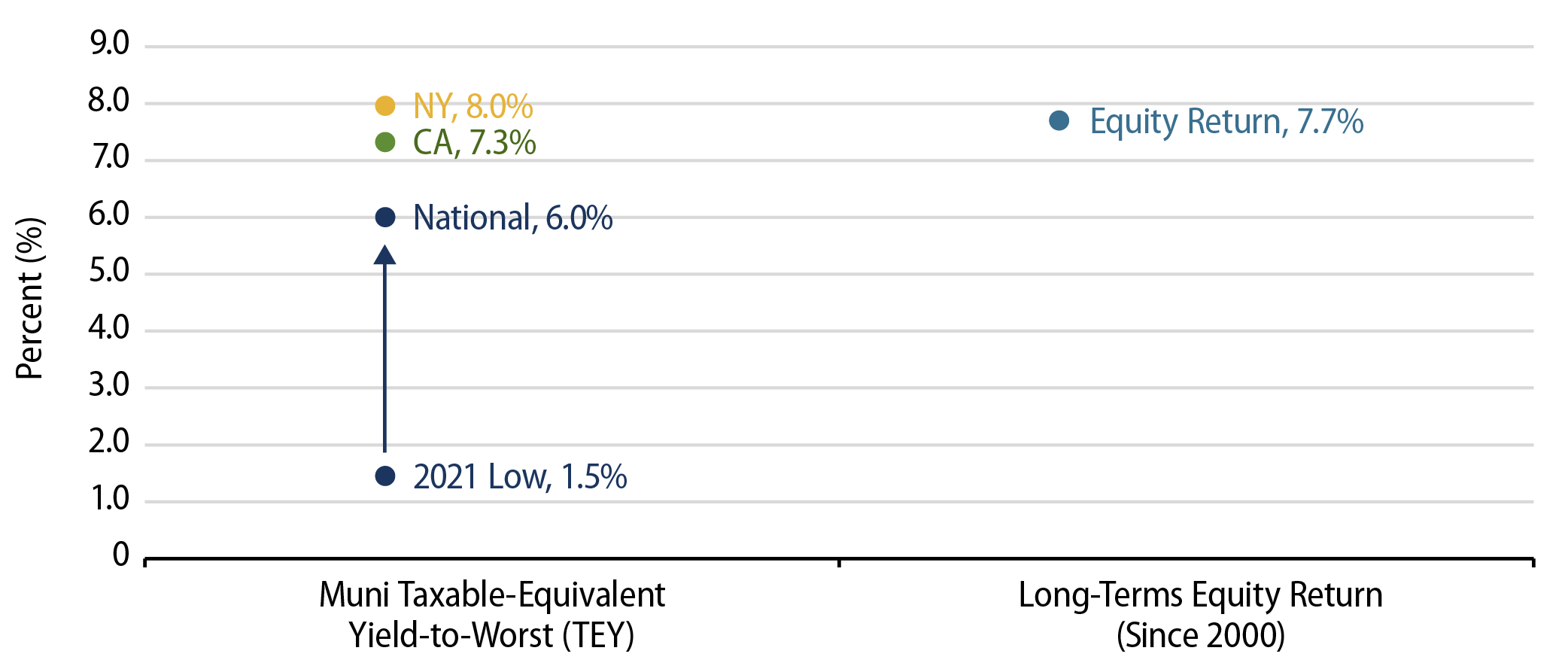

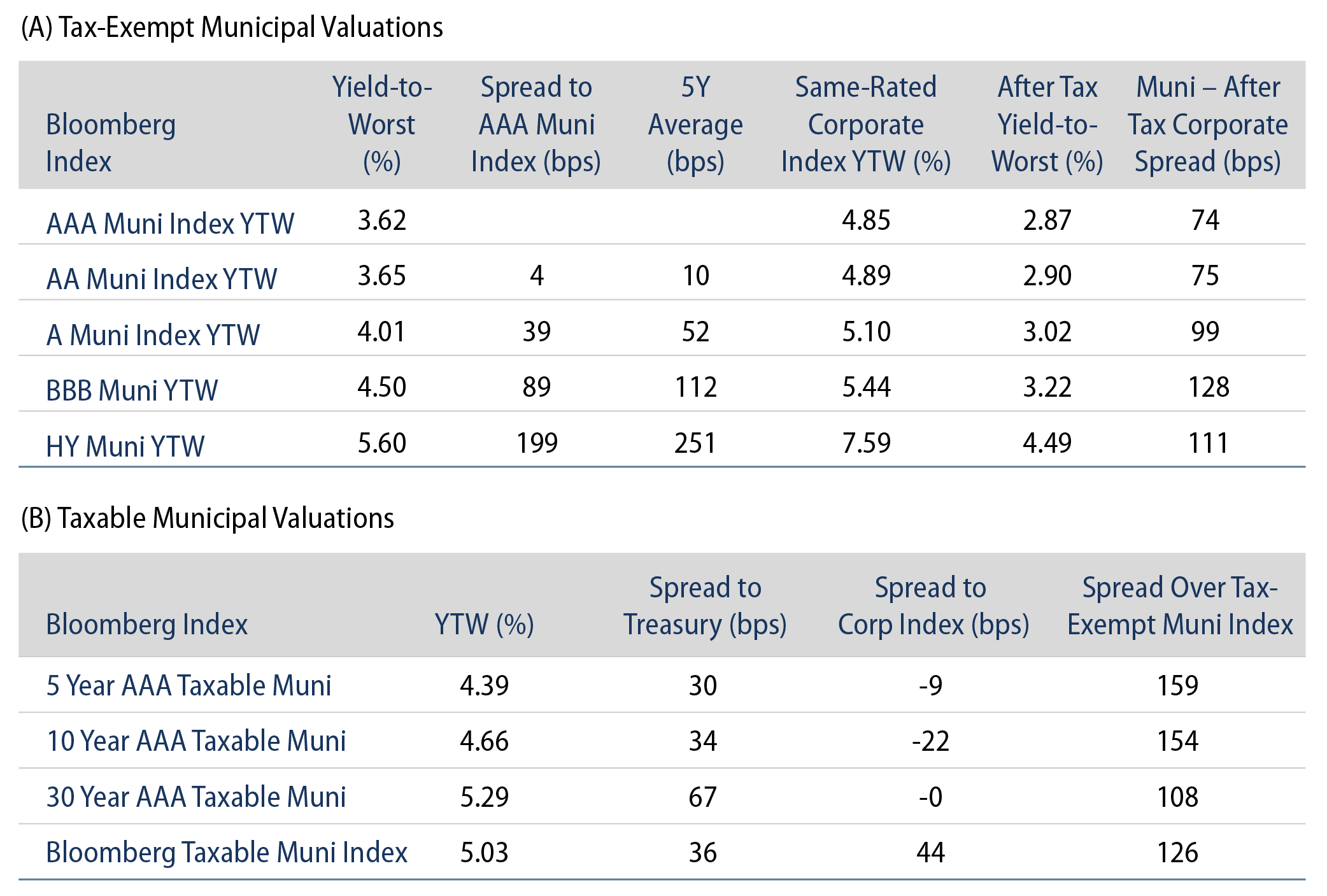

Current muni valuations versus volatile equity counterparts further add to the risk-adjusted value proposition. Considering the Bloomberg Municipal Bond Index starting yield levels, taxable-equivalent income opportunities of 6%-8% offered by munis are presently near long-term equity return levels of 7.7%. This is particularly compelling given that since 2000 the volatility of the S&P 500 Index (15.25%) was more than three times that of the Bloomberg Municipal Bond Index (4.68%). All told, we anticipate the risk-adjusted value proposition to remain supported by favorable fundamental and technical factors, as state and local revenues and reserve balances remain at elevated levels. Meanwhile, we anticipate that demand could also improve should the Fed continue its cutting of short-term rates, making cash solutions less attractive relative to the longer-term after-tax opportunities offered by munis.

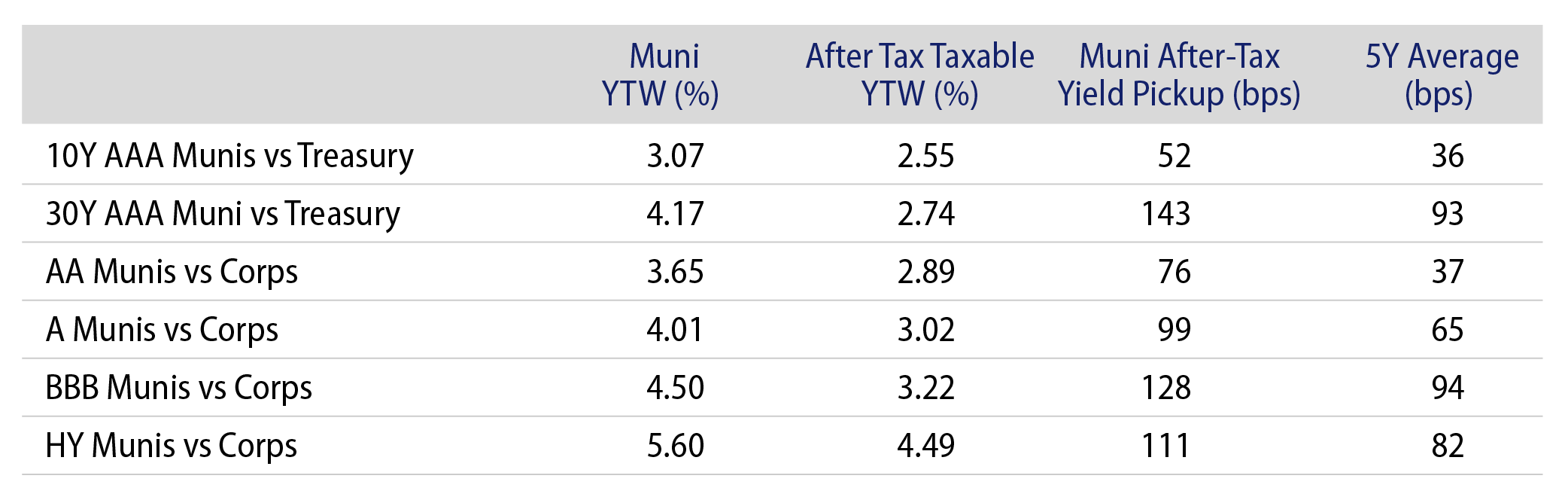

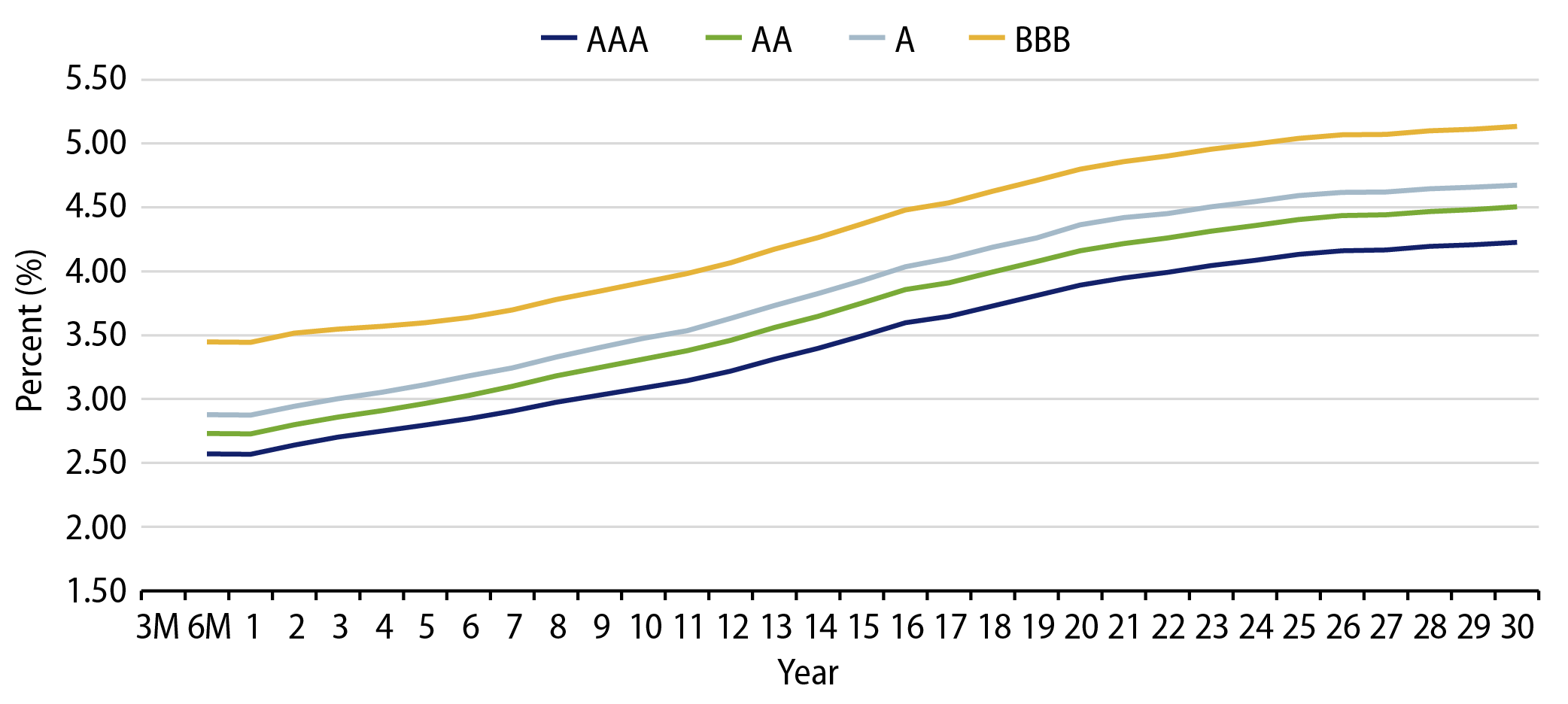

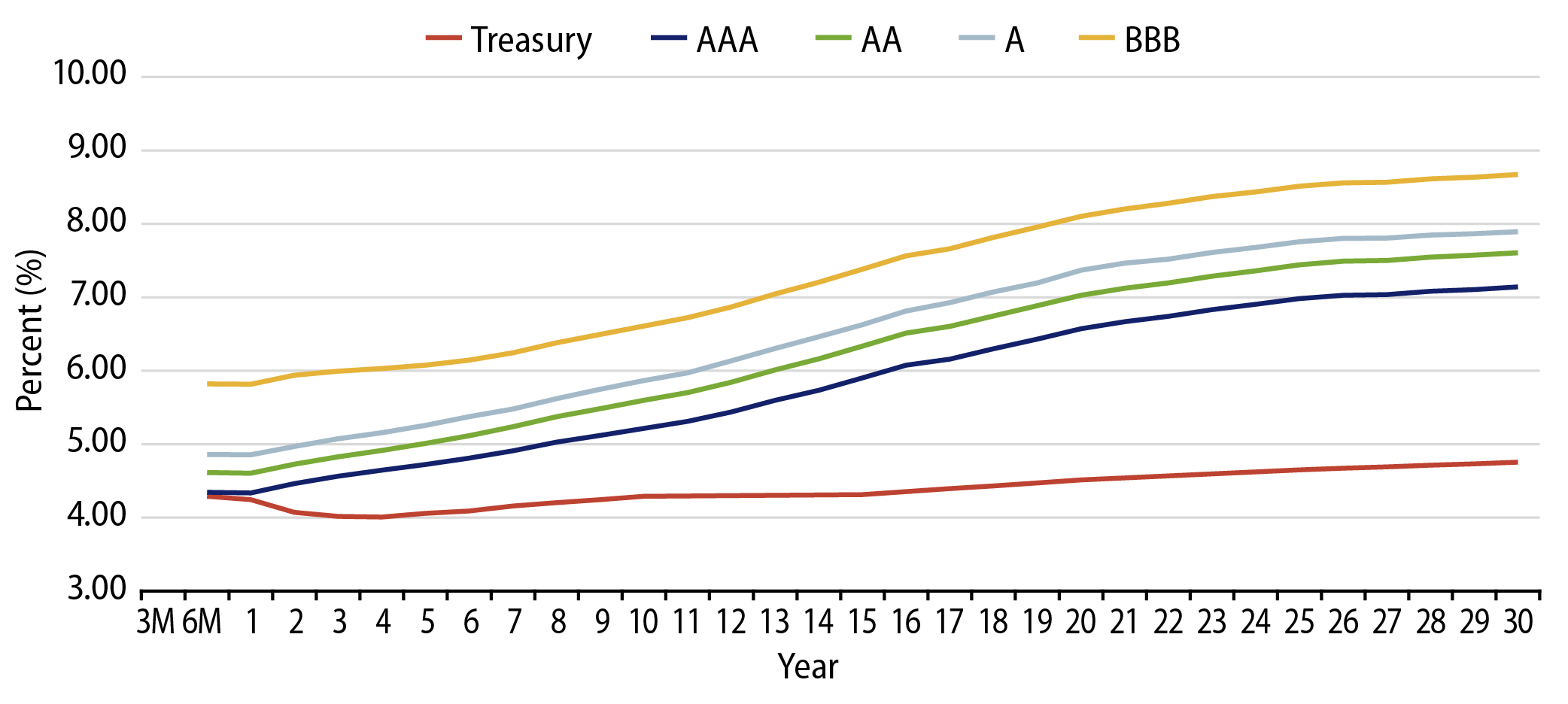

Municipal Credit Curves and Relative Value

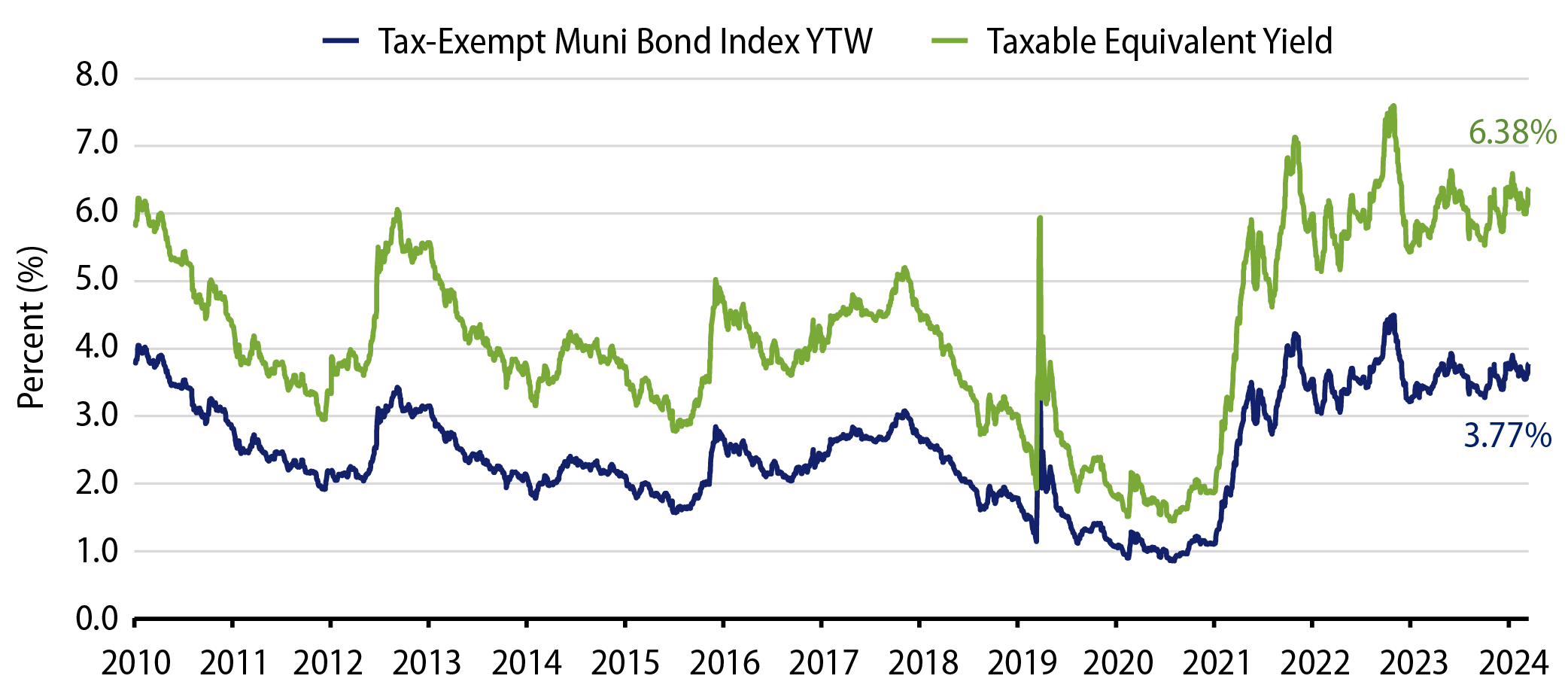

Theme #1: Municipal taxable-equivalent yields and income opportunities remain above decade averages.

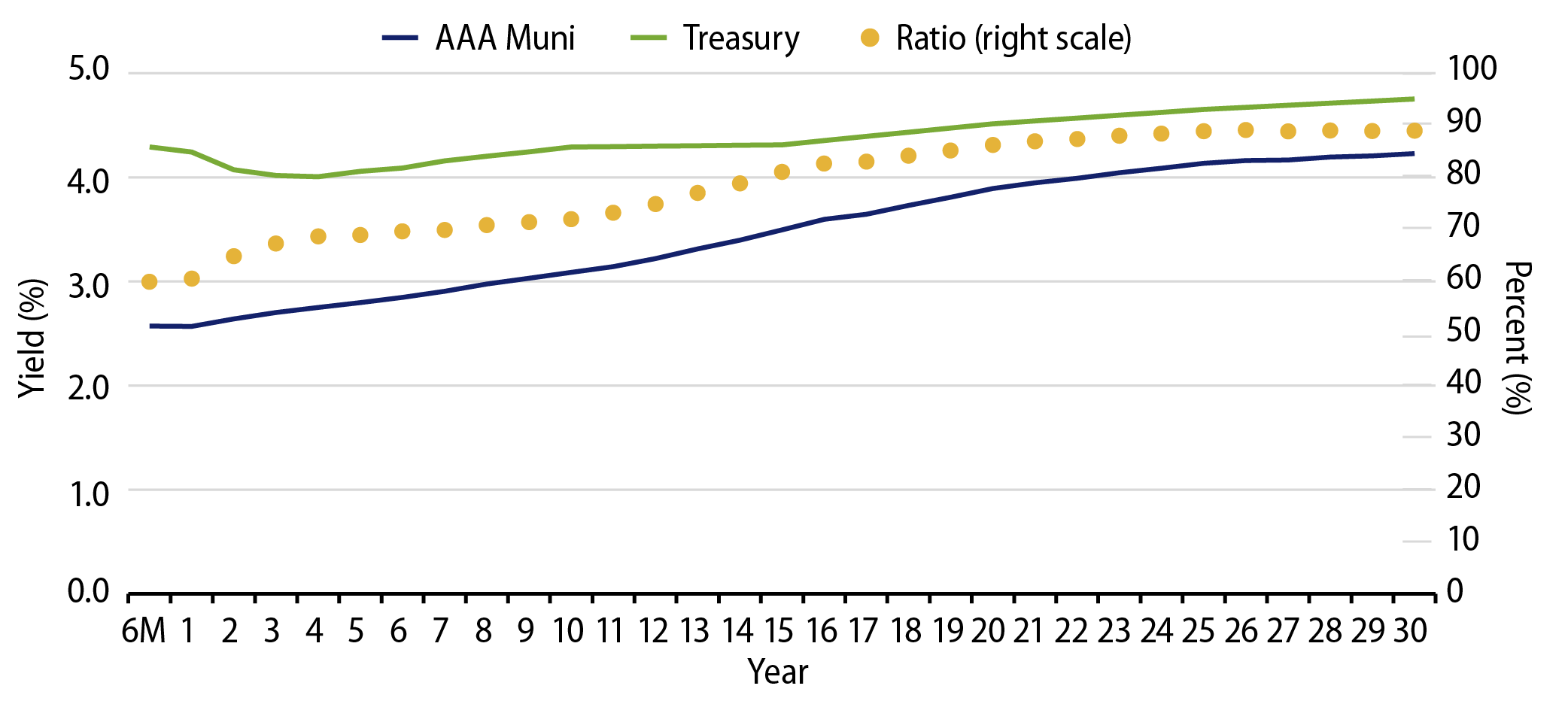

Theme #2: The muni curve has steepened, offering better value in intermediate and longer maturities.

Theme #3: Munis offer attractive after-tax yield pickup versus longer-dated Treasuries and investment-grade corporate credit.