Macros, Markets and Munis

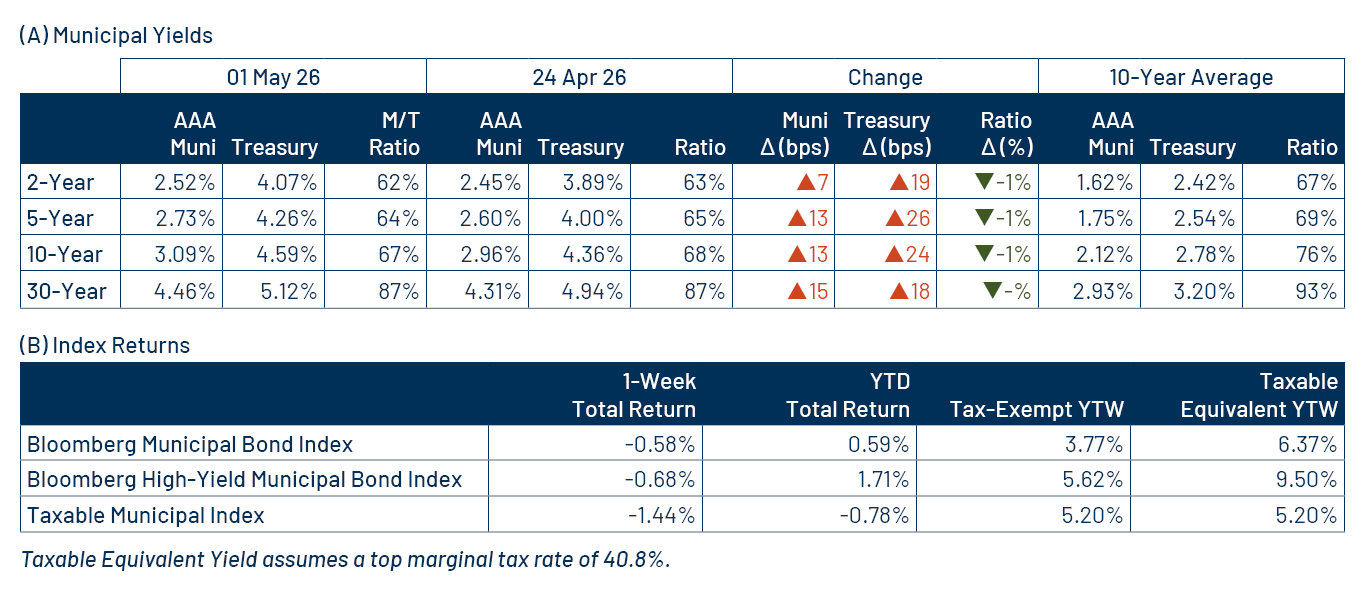

Municipals posted negative returns last week and outperformed Treasuries. Stalling ceasefire talks and reignited inflation concerns contributed to market volatility last week. The Consumer Price Index (CPI) rose 3.8% year-over-year (YoY) last week, coming in above both the prior month’s reading of 3.3% and consensus expectations of 3.7%. The Federal Reserve’s (Fed) preferred inflation measure, core Personal Consumption Expenditures (PCE), also accelerated to 2.8% YoY, exceeding expectations. In response, markets shifted from pricing a higher probability of interest rate cuts to assigning greater odds to additional rate hikes. Treasuries sold off across the yield curve, moving 18-26 basis points (bps) higher with the greatest pressure on intermediate maturities. Municipals generally outperformed, moving just 7-15 bps higher across the curve, with supply and demand dynamics remaining elevated. This week we touch on the current municipal inflow cycle and what may lie ahead for muni demand.

Demand Improved as Supply Continues to Build

Fund Flows ($1.3 billion of net inflows): During the week ending May 13, weekly reporting municipal mutual funds recorded $1.3 billion of net inflows, according to Lipper. The long-term category recorded $656 million of inflows, the intermediate category reported $416 million of inflows and the short-term category recorded $209 million of net inflows. Last week’s inflows bring year-to-date (YTD) inflows to $37 billion.

Supply (YTD supply of $218 billion; up 16% YoY): The muni market recorded $15 billion of new-issue supply last week, up 4% from the prior week. YTD new-issue supply of $218 billion is 16% higher than the prior year, with tax-exempt issuance up 17% YoY and taxable issuance up 9%. This week’s calendar is expected to remain elevated at $14 billion. Largest deals include $762 million Oklahoma Public Property Authority and $609 million Missouri Highways and Transportation transactions.

This Week in Munis: Steady Demand

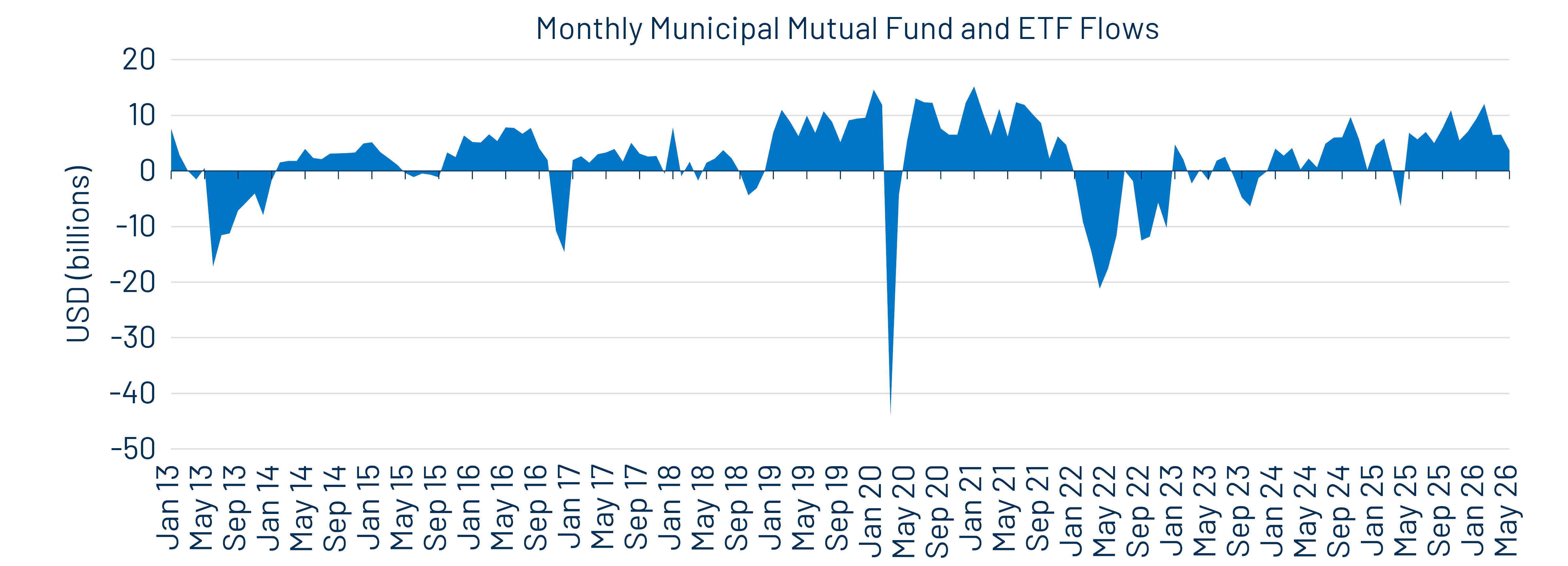

This week’s strong municipal mutual fund flows extended the favorable demand trends that have been building in recent years. So far this year, muni mutual funds recorded $37 billion of inflows, according to Lipper. Across the curve, flows have been concentrated in long-term strategies ($20 billion), followed by intermediate-term ($11 billion) and short-term strategies ($4 billion). From a credit-quality perspective, investment-grade funds attracted the majority of new assets ($31 billion), while high-yield funds recorded $4 billion of net inflows. From a vehicle perspective, open-end funds ($20 billion) outpaced ETFs ($16 billion) in attracting new assets.

The current inflow cycle that began in 2024 after the Fed effectively ended its rate-hiking campaign has steadily strengthened to near-record levels. Following $45 billion of inflows in 2024 and $62 billion in 2025, the YTD inflows bring the cumulative total flows to approximately $144 billion. This has more than reversed the record $125 billion of outflows recorded between January 2022 and January 2024 during the Fed’s aggressive rate-hiking period.

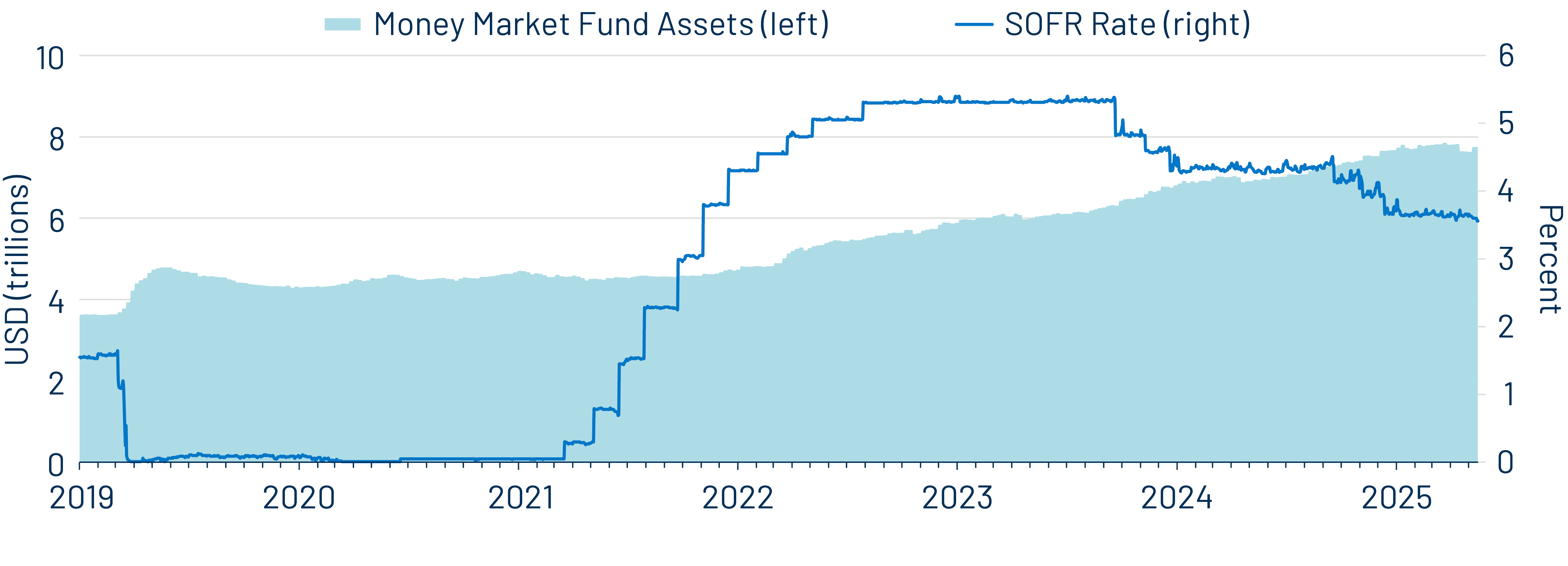

Western Asset believes that relatively high taxable-equivalent municipal yields have supported the recovery in fund flows, particularly as valuations appear increasingly full across more volatile asset classes, including corporate credit and equities. While we expect attractive tax-exempt income opportunities to continue driving muni market demand for both municipal funds and separately managed accounts, renewed inflation pressures could encourage investors to remain in cash equivalents longer than currently expected, as money market assets have continued to grow to nearly $8 trillion even after the Fed reduced rates in recent years. As a result, we anticipate a more gradual reallocation into municipals, rather than some of the sharper recoveries recorded in recent history, potentially contributing to ongoing technical dislocations that create opportunities for active management ahead.

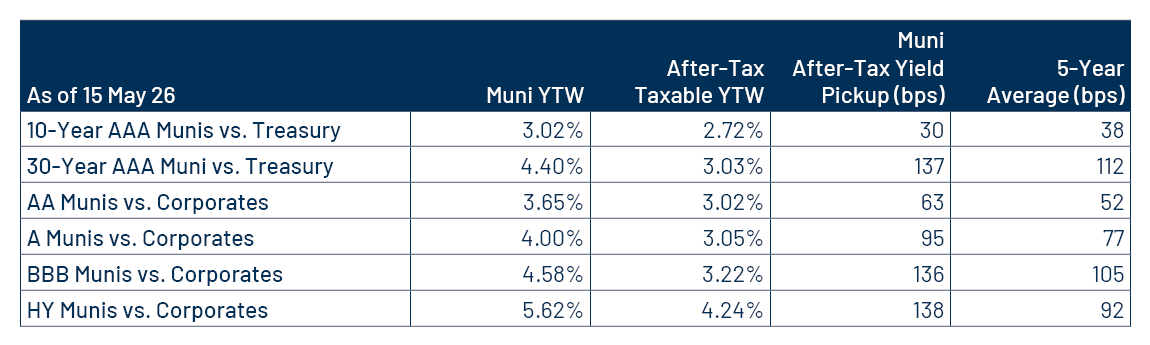

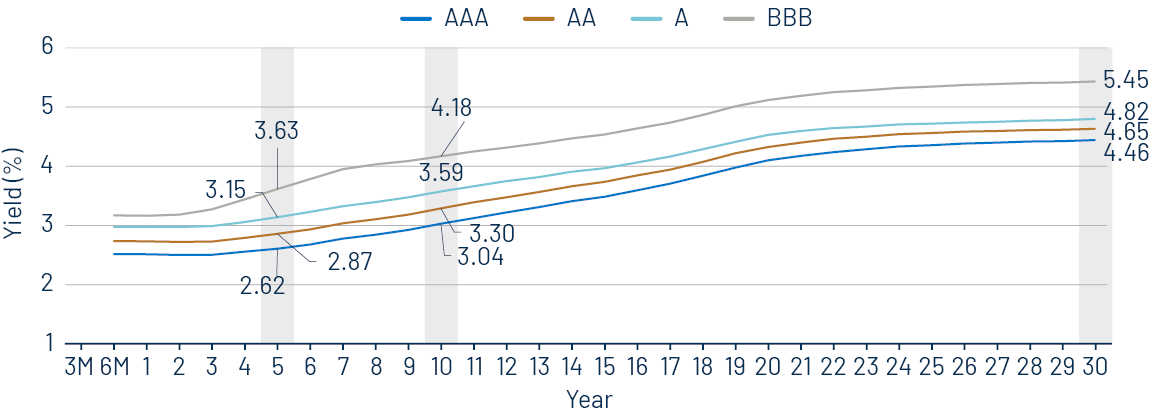

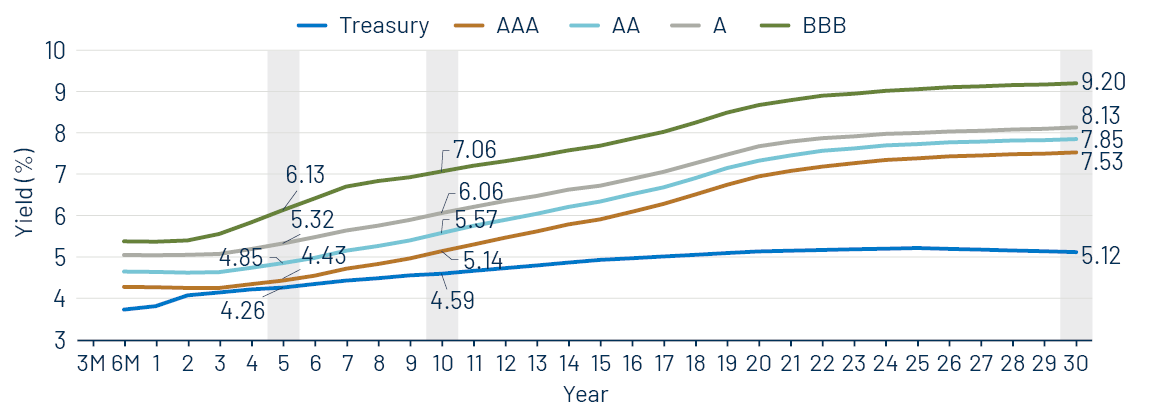

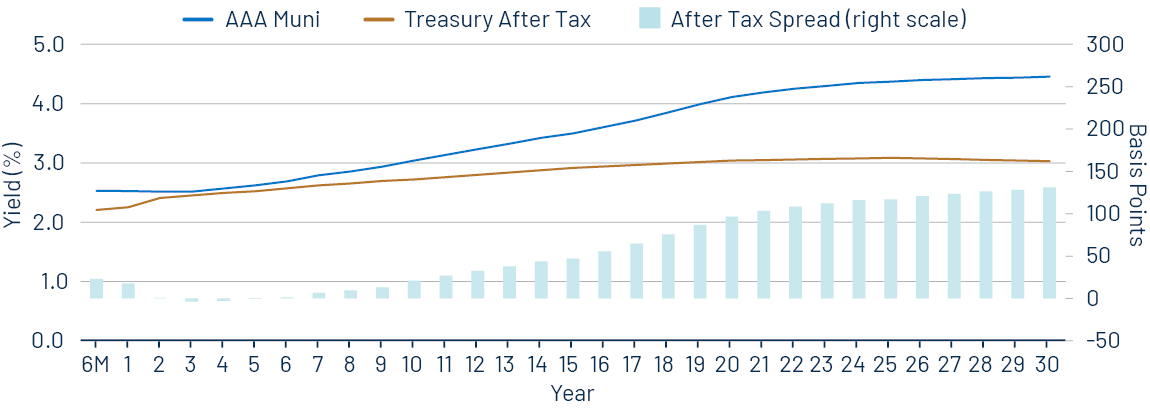

Municipal Credit Curves and Relative Value

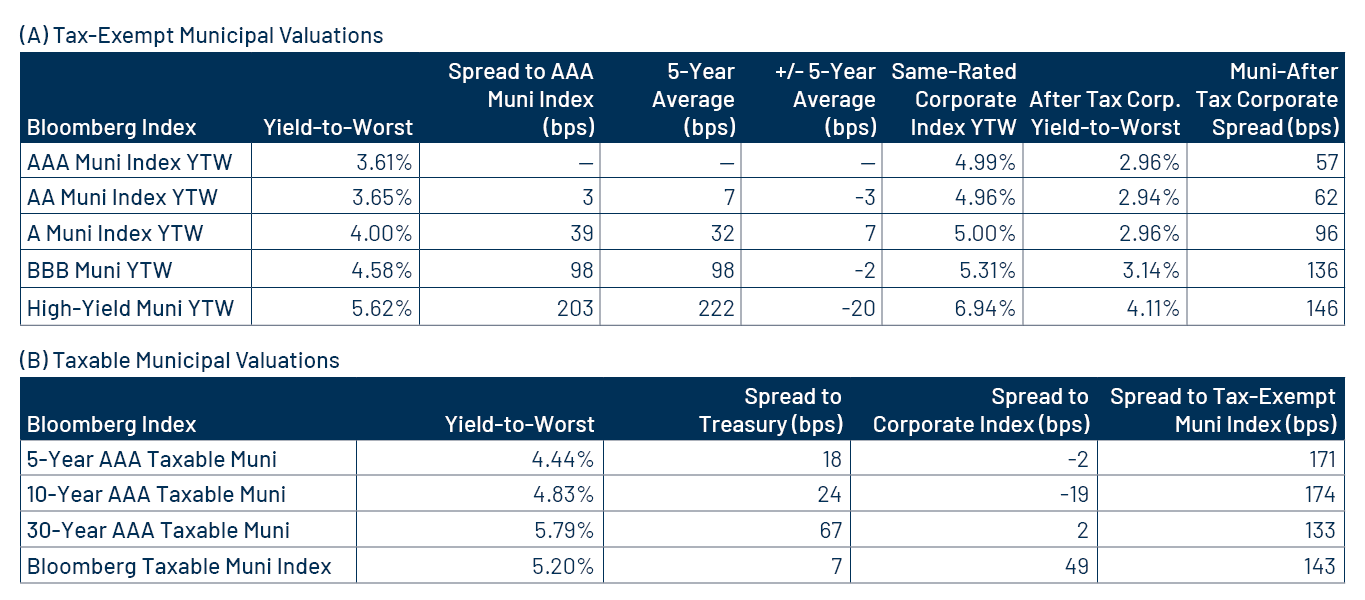

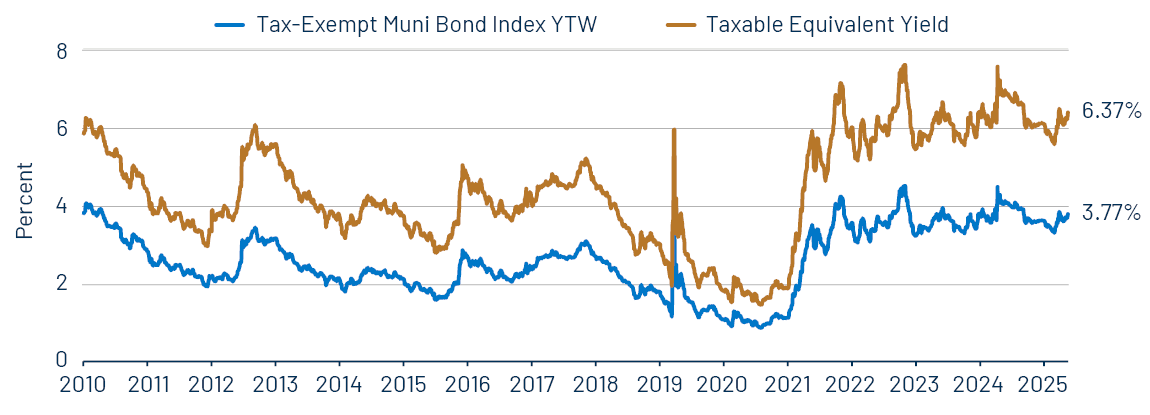

Theme 1: Municipal taxable-equivalent yields moved lower from recent highs, but remain above historical averages.

Theme 2: Munis offer attractive after-tax yield pickup vs. longer-duration and lower-quality taxable alternatives.

Theme 3: The muni curve remains steep and offers relative value in longer maturities.