Macros, Markets and Munis

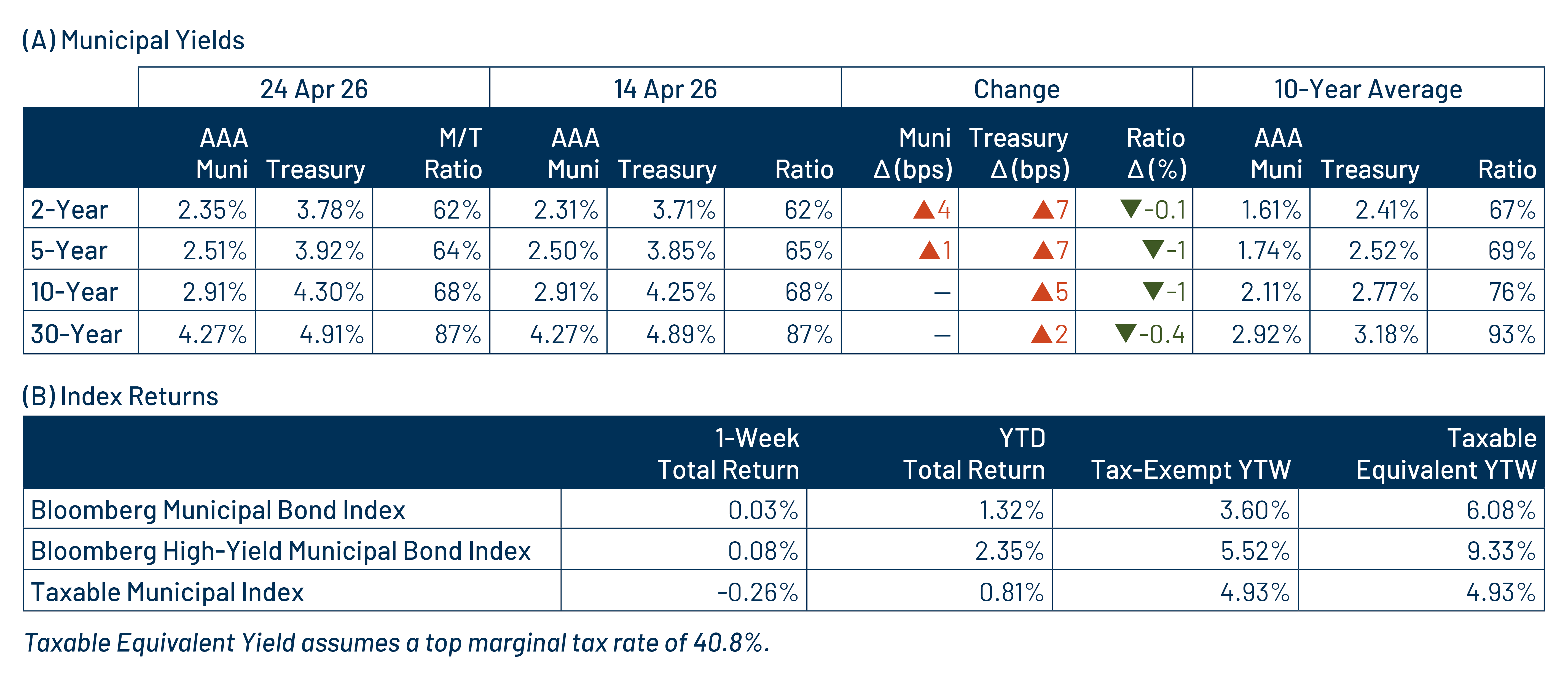

Municipals posted positive returns and outperformed taxable fixed-income last week. Markets remained focused on the Iran war, as negotiations were repeatedly postponed throughout the week. Economic data was limited, but consumer sentiment rose above expectations, while initial jobless claims also moved higher. Treasuries sold off across the curve, with yields rising approximately 7 basis points (bps) in shorter maturities and 2 bps in longer maturities, resulting in a flatter curve. Municipals generally outperformed Treasuries amid rebounding demand, with yields rising just 1 to 4 bps in the front end. Demand recovered following the prior week’s outflows. This week we touch on elevated muni supply trends.

Demand Rebounds From Tax Day Selling

Fund Flows ($1.0 billion of net outflows): During the week ending April 22, weekly reporting municipal mutual funds recorded $1 billion of net outflows, according to Lipper, rebounding from the prior week’s Tax Day redemptions. The long-term category recorded $600 million of inflows, the intermediate category reported $304 billion of inflows and the short-term category recorded $22 million of net inflows. Last week’s inflows bring year-to-date (YTD) inflows to $29 billion.

Supply (YTD supply of $175 billion; up 22% YoY): The muni market recorded $13 billion of new-issue supply last week, down 25% from the prior week. YTD new-issue supply of $175 billion is 22% higher than the prior year, with tax-exempt issuance up 22% year-over-year (YoY) and taxable issuance up 25%, respectively. This week’s calendar is expected to remain elevated at $12 billion. The largest deals include $1.3 billion Massachusetts Development Finance Agency and $770 million Southern California Public Power (Gas Pre-Pay) transactions.

This Week in Munis: Sustained Supply

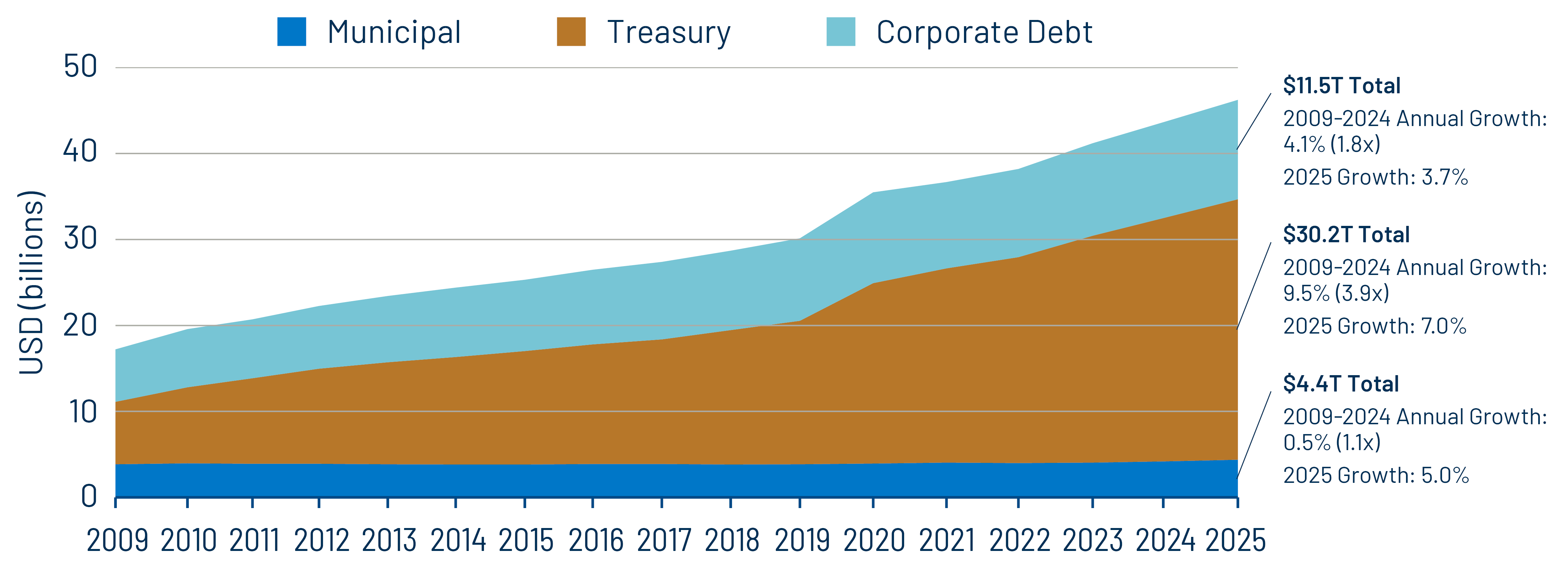

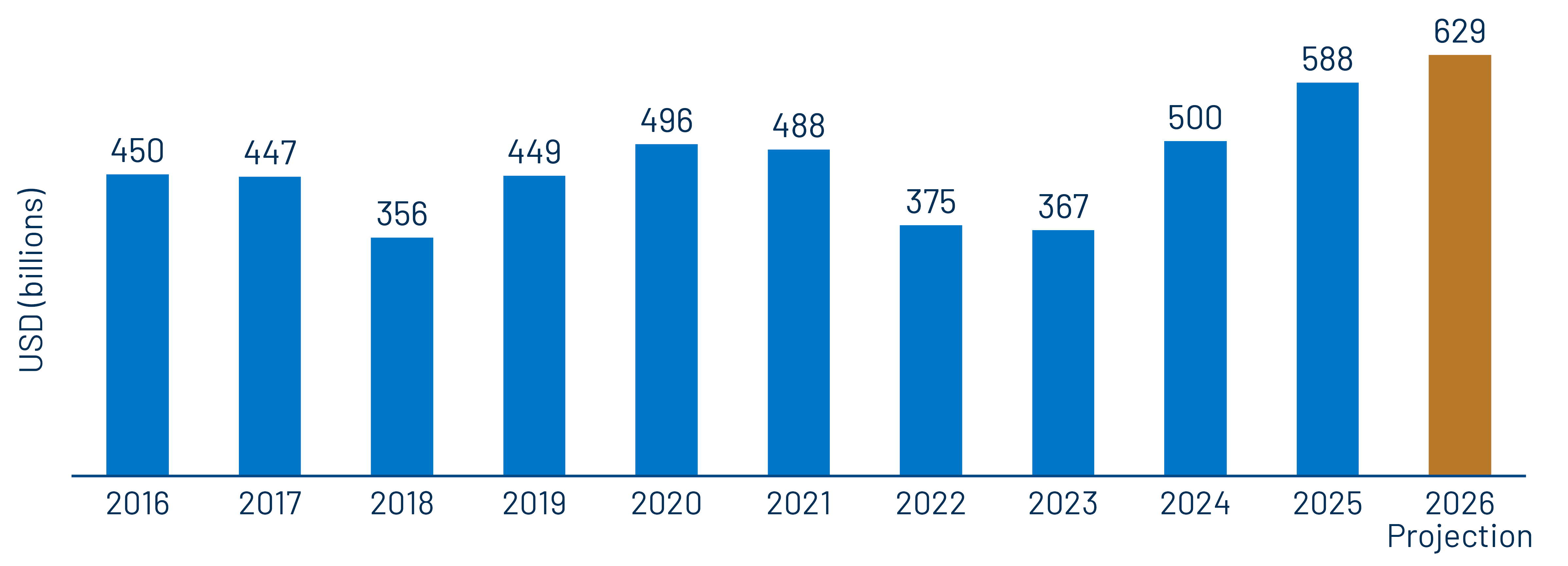

Post-GFC (global financial crisis), municipal issuance remained relatively constrained as municipalities focused on addressing structural budget deficits and pension liabilities. From 2009 through 2024, municipal debt outstanding grew by less than 10% (approximately 0.5% annually), compared to corporate debt, which nearly doubled (1.8x) and Treasury debt, which nearly quadrupled (3.9x). The record $588 billion of issuance in 2025 marked a notable shift, supporting market growth more in line with other fixed-income sectors, with municipal debt expanding by approximately 5%, between the 3.7% growth of corporates and 7.0% growth of Treasuries.

So far in 2026, elevated supply trends have persisted. Including this week’s issuance, approximately $185 billion of new-issue supply through April represents roughly 7% above prior record-year levels, tracking toward an estimated $629 billion for the full year. Recent strength has been driven by a confluence of factors, including a rebound in infrastructure demand following subdued issuance during the rate volatility of 2022-2023, policy uncertainty surrounding the election and the passage of the “One Big Beautiful Bill” and ongoing inflationary pressures increasing the cost of infrastructure projects.

Looking ahead, we expect elevated municipal supply to persist. The One Big Beautiful Bill Act includes provisions that could further support issuance, including expanded use of private activity bonds, reduced thresholds for affordable housing projects and increased support for public-private partnerships. In addition, rising demand for data centers and broader infrastructure investment is likely to sustain issuance needs. As inflation continues to pressure key inputs and pandemic-era stimulus funds fade into 2026, municipalities may increasingly re-lever balance sheets, contributing to higher issuance.

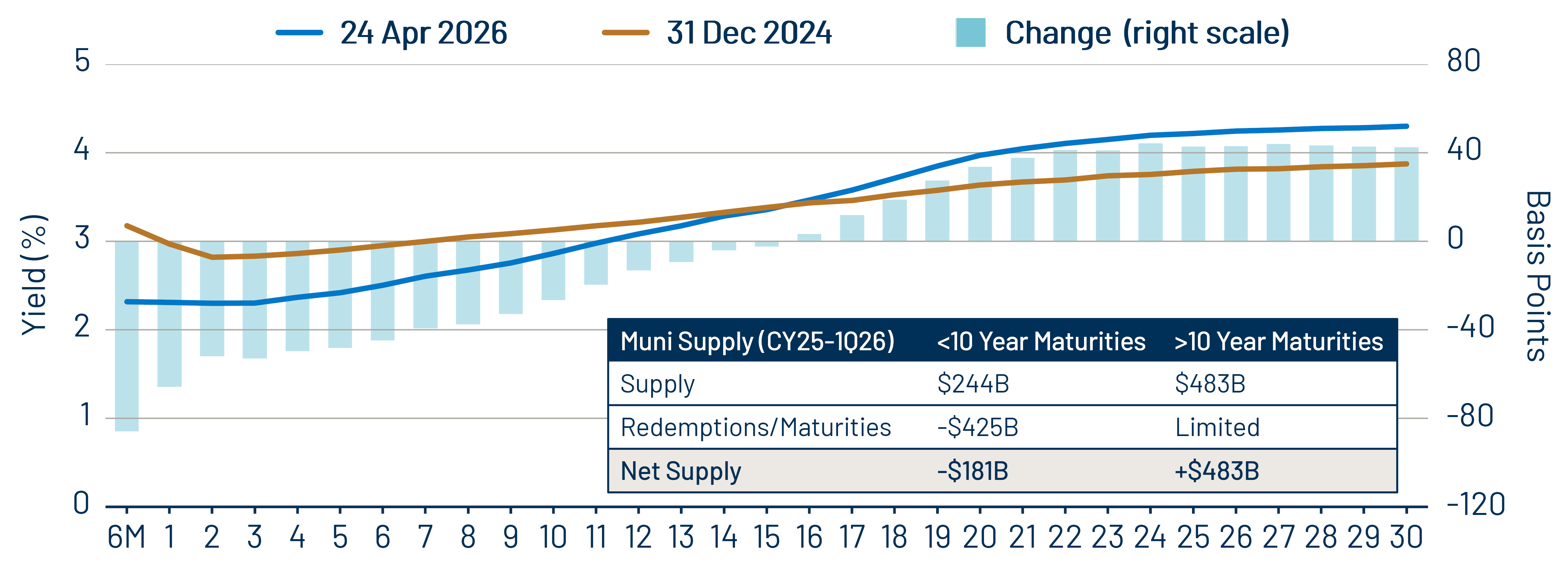

From a valuation perspective, the increased supply observed over the past year has contributed to a steeper municipal yield curve, offering greater after-tax relative value and rolldown opportunities compared to other fixed-income markets. Higher supply levels also expand the opportunity set for active managers to tailor portfolios to specific client mandates. Western Asset believes investors with the flexibility to access the full breadth of the municipal market are well positioned to benefit from these dynamics and achieve improved after-tax outcomes.

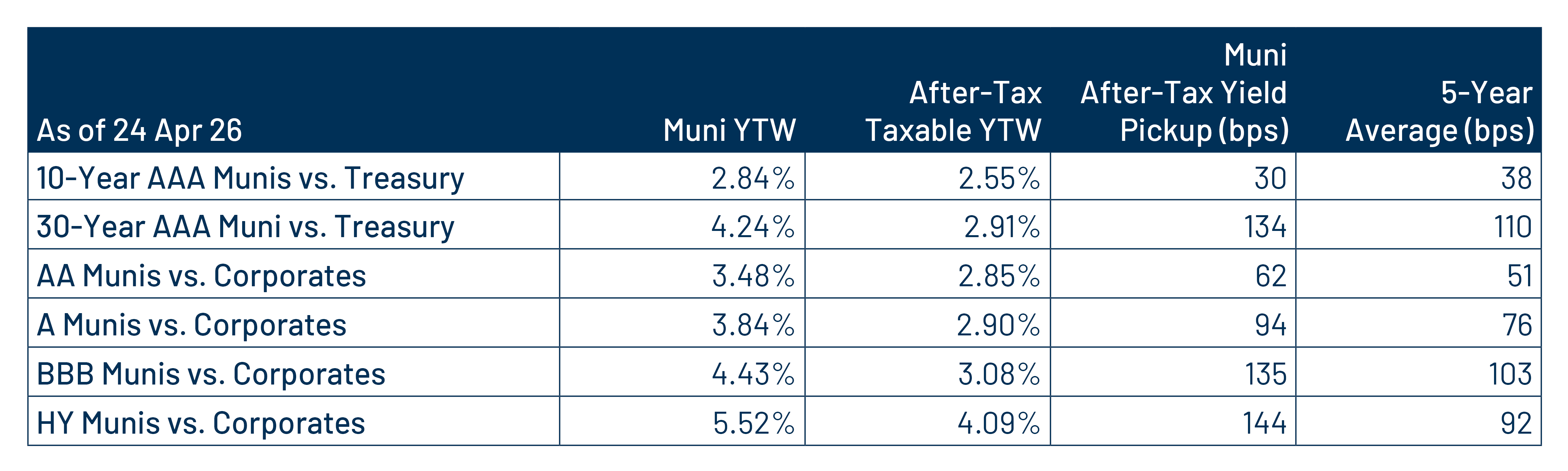

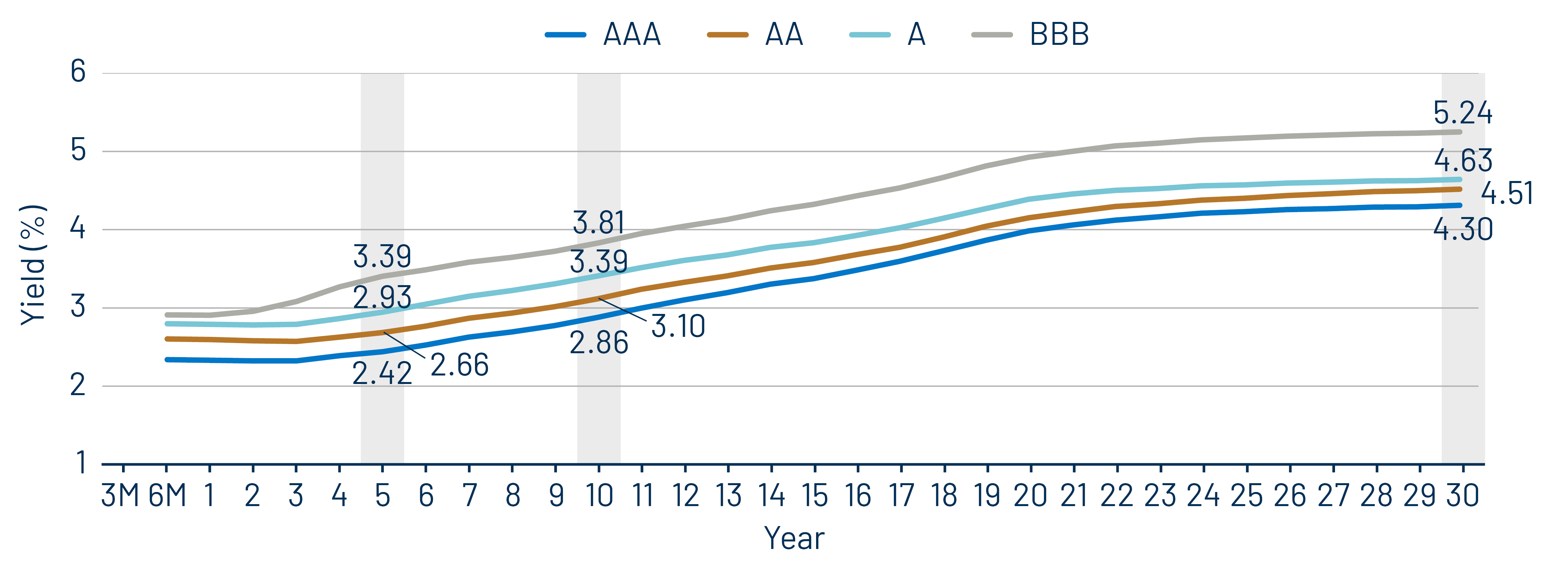

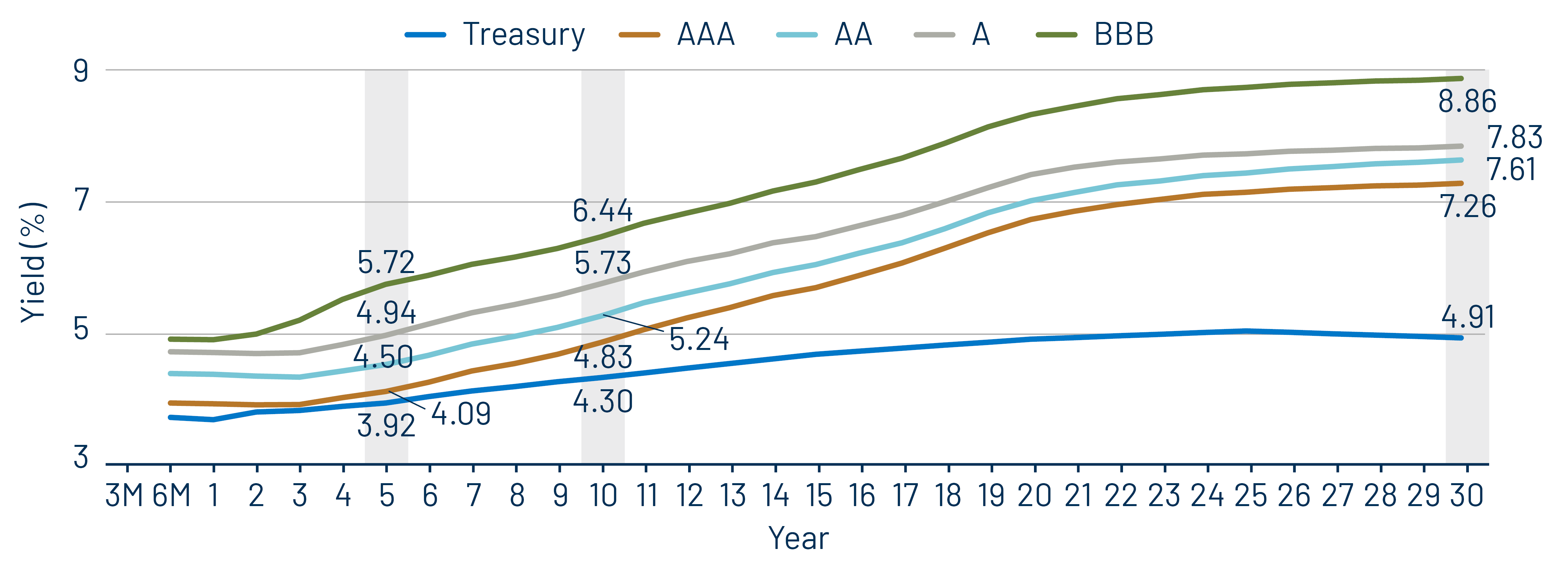

Municipal Credit Curves and Relative Value

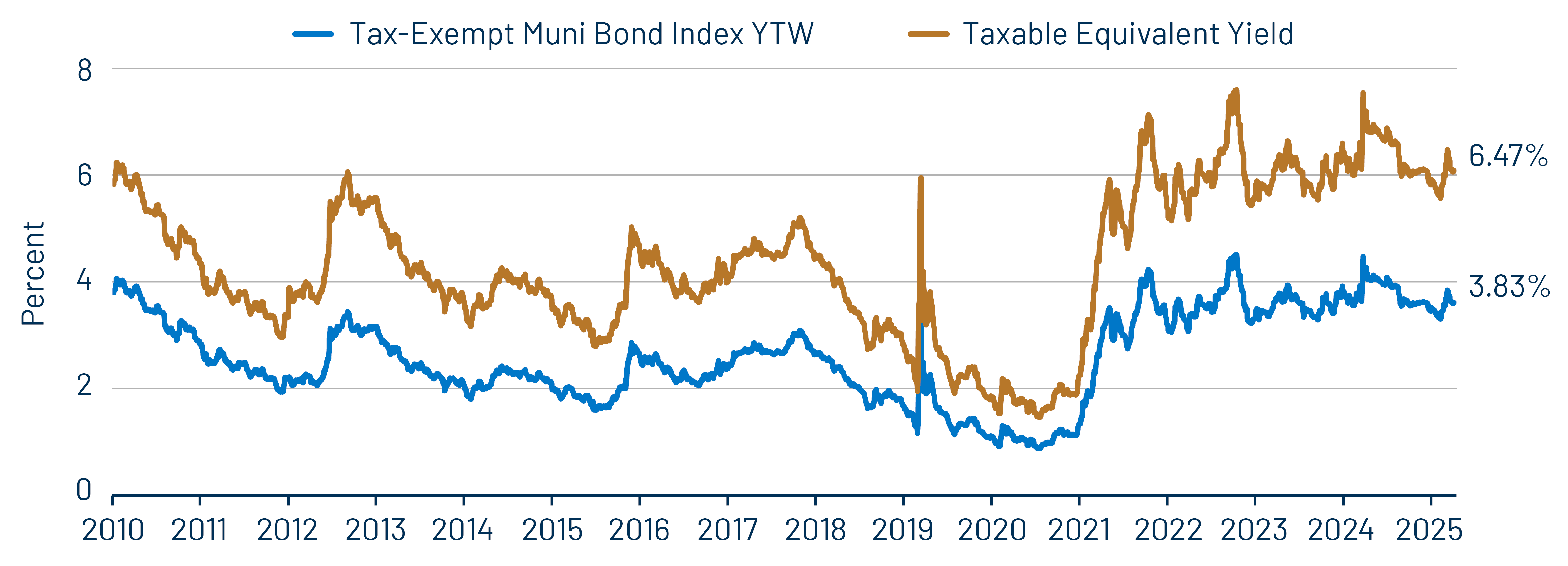

Theme #1: Municipal taxable-equivalent yields moved lower from recent highs, but remain above historical averages..

Theme #2: Munis offer attractive after-tax yield pickup vs. longer-duration and lower-quality taxable alternatives.

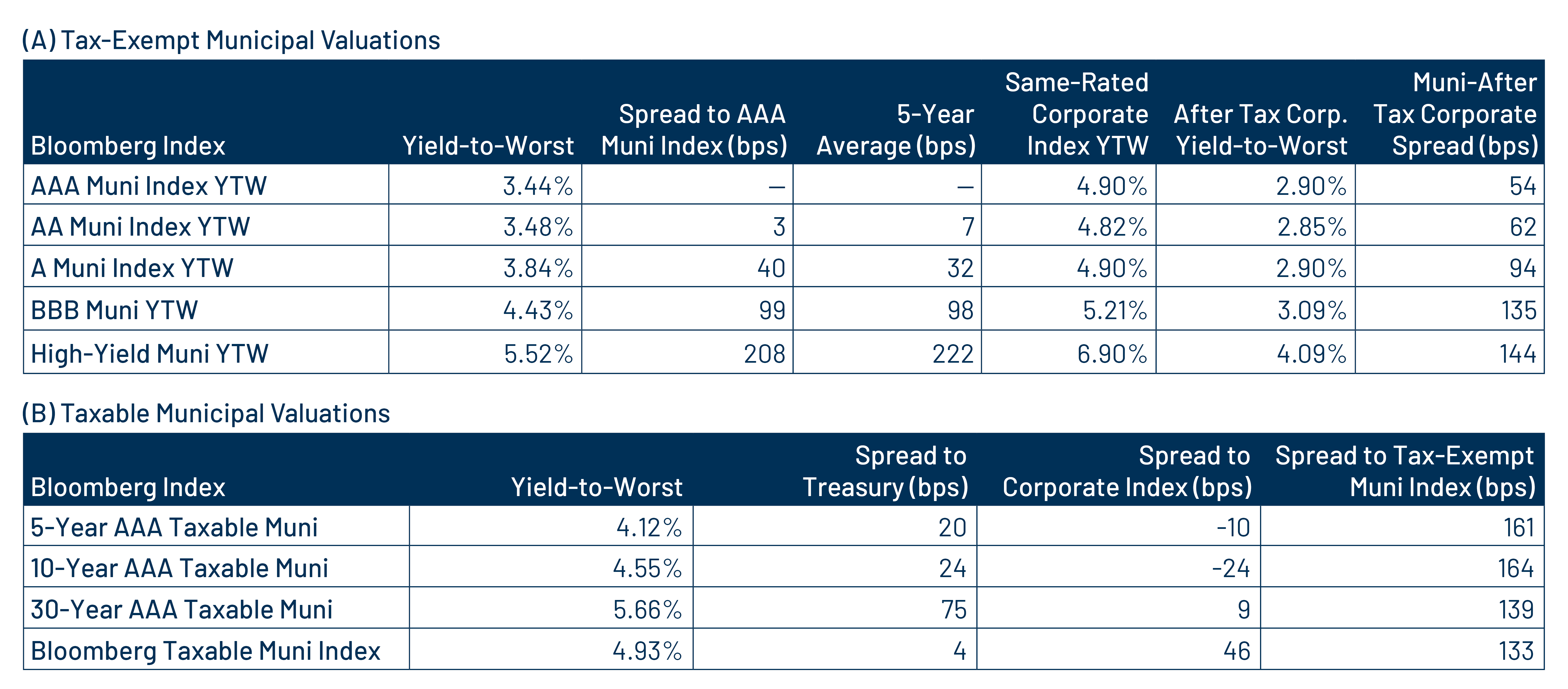

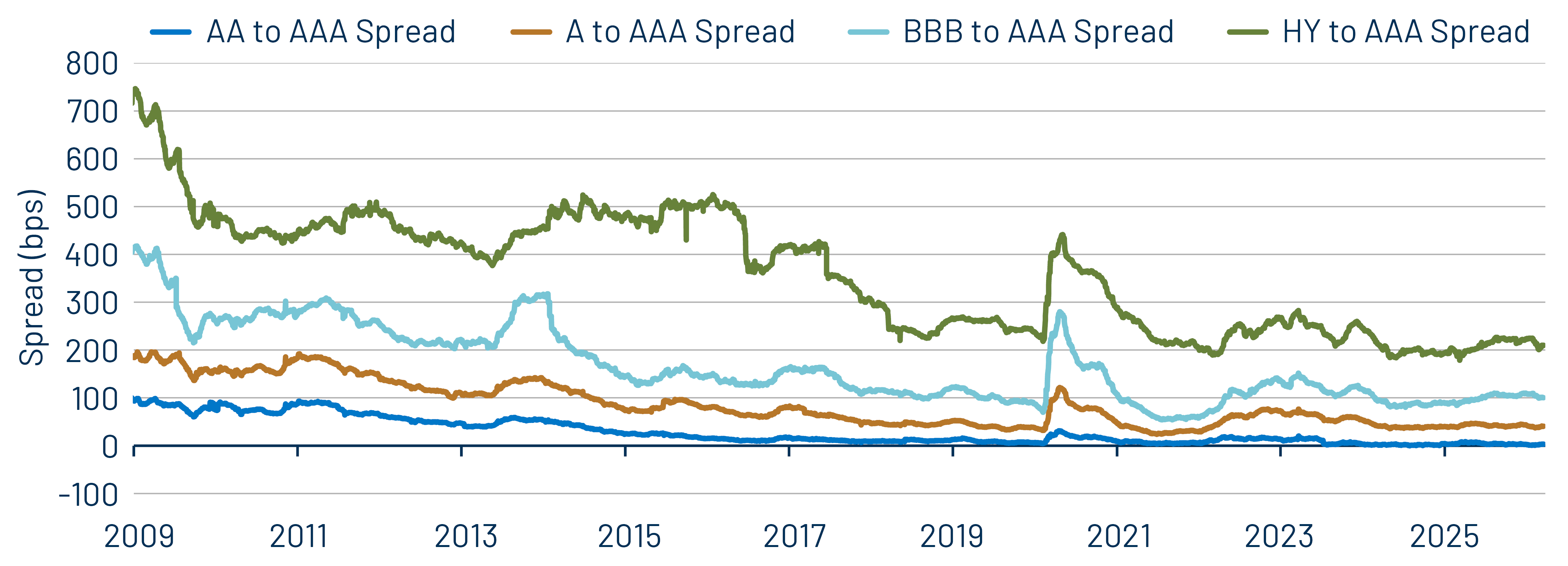

Theme #3: Historically tight municipal credit spreads underscore the importance of credit selection.