Performance Overview

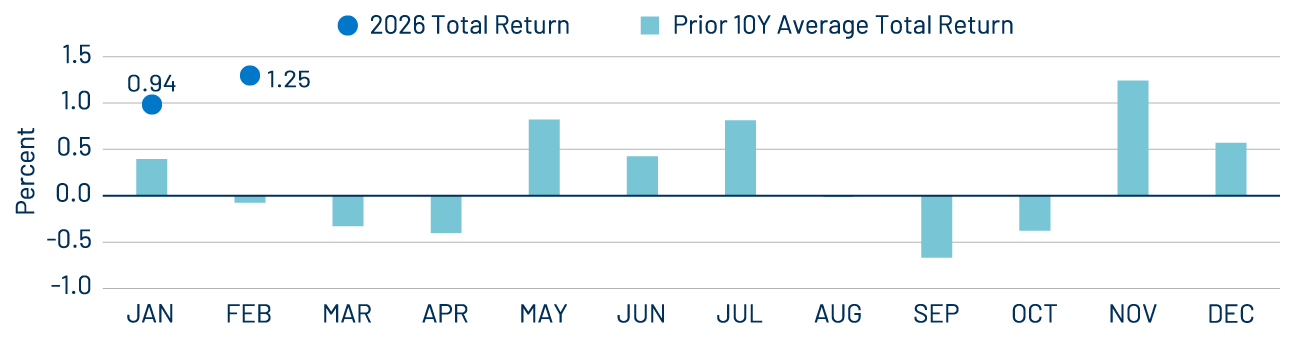

Strong Municipal Performance in February Counters Recent Weakness

In February, market sentiment was shaped by escalating US-Iran geopolitical tensions and sector-specific selloffs driven by concerns about AI’s potential disruption to existing business models. Economic data presented a mixed picture, with January nonfarm payrolls increasing by 130,000 jobs, rebounding from December’s revised 48,000 gain, while the unemployment rate edged down to 4.3%. Inflation data for January eased from the prior month, with headline Consumer Price Index (CPI) falling to 2.4% year-over-year (YoY) from 2.7% and core CPI easing to 2.5% YoY from 2.6%. All told, Treasuries rallied across the curve, and the municipal yields followed suit but generally underperformed the risk-off sentiment. The Bloomberg Municipal Bond Index gained 1.25% leading year-to-date (YTD) returns higher to 2.20%. February’s strong performance counters recent weakness, with the index averaging negative returns in February, largely driven by softening demand ahead of tax season and limited new issuance.

Technicals

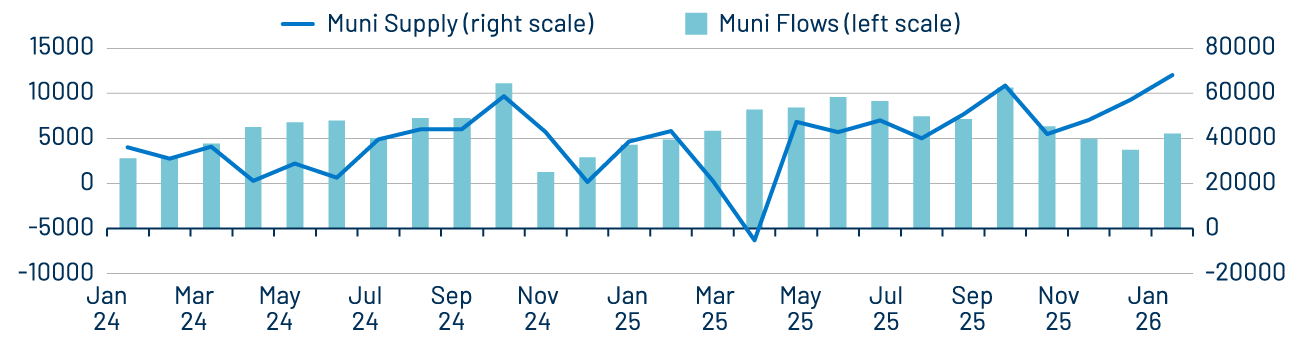

Renewed Investor Demand Bolstered Muni Funds

The strong start of the year has been supported by renewed investor demand, as capital has moved decisively back into municipal mutual funds. Investors appear to show an increasing willingness to capitalize on relatively attractive municipal valuations during periods of elevated market volatility, particularly in longer maturities as the yield curve steepened. According to weekly and monthly Lipper and ICI data, municipal mutual funds and ETFs recorded over $10 billion of net inflows in February. Notably, Lipper estimates that approximately 86% of the $18 billion in YTD inflows has been concentrated in intermediate- and long-duration fund categories. Since January 2024, cumulative net inflows of over $126 billion on top of strong SMA demand have fully offset the $122 billion of net outflows experienced in 2022 and 2023.

Fundamentals

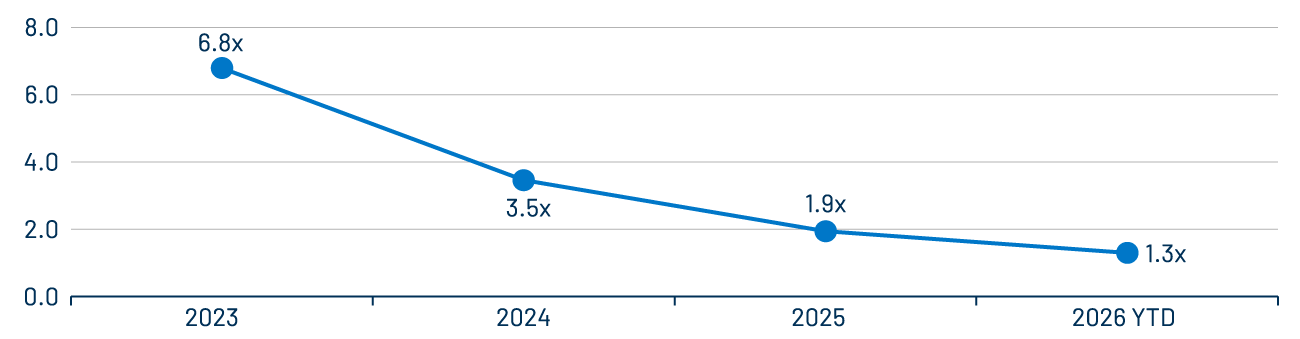

Muni Fundamentals Remained Strong

Municipal fundamentals remained strong, supported by elevated tax collections. However, the pace of upgrades relative to downgrades has continued to moderate. Upgrades have outpaced downgrades YTD by a factor of 1.3x, compared to 3.5x in 2024 and 1.9x in 2025, according to Bloomberg. Notably, Fitch downgraded the city of Chicago during the month from A- to BBB+, while maintaining a negative outlook. Fitch cited consecutive operating deficits and a high reliance on one-time solutions as key drivers of the downgrade.

Valuations

Muni Valuation Disparities Create Tax-Efficient Opportunities for Active Managers

The strong YTD performance also represents a meaningful reversal of the underperformance the municipal market experienced in 2025, and muni supply and demand dynamics have shifted valuations in certain segments of the market. For example, AAA rated municipals maturing inside of 10 years now yield less than comparable Treasuries on an after-tax basis, assuming a 37% effective tax rate, largely attributable to high demand for SMA strategies concentrated in shorter maturities. In contrast, using the same tax rate, AAA municipals beyond 20 years offer more than 100 basis points of after-tax yield advantage relative to Treasuries. We believe these valuation disparities create opportunities for active managers to deliver tax-efficient outcomes.