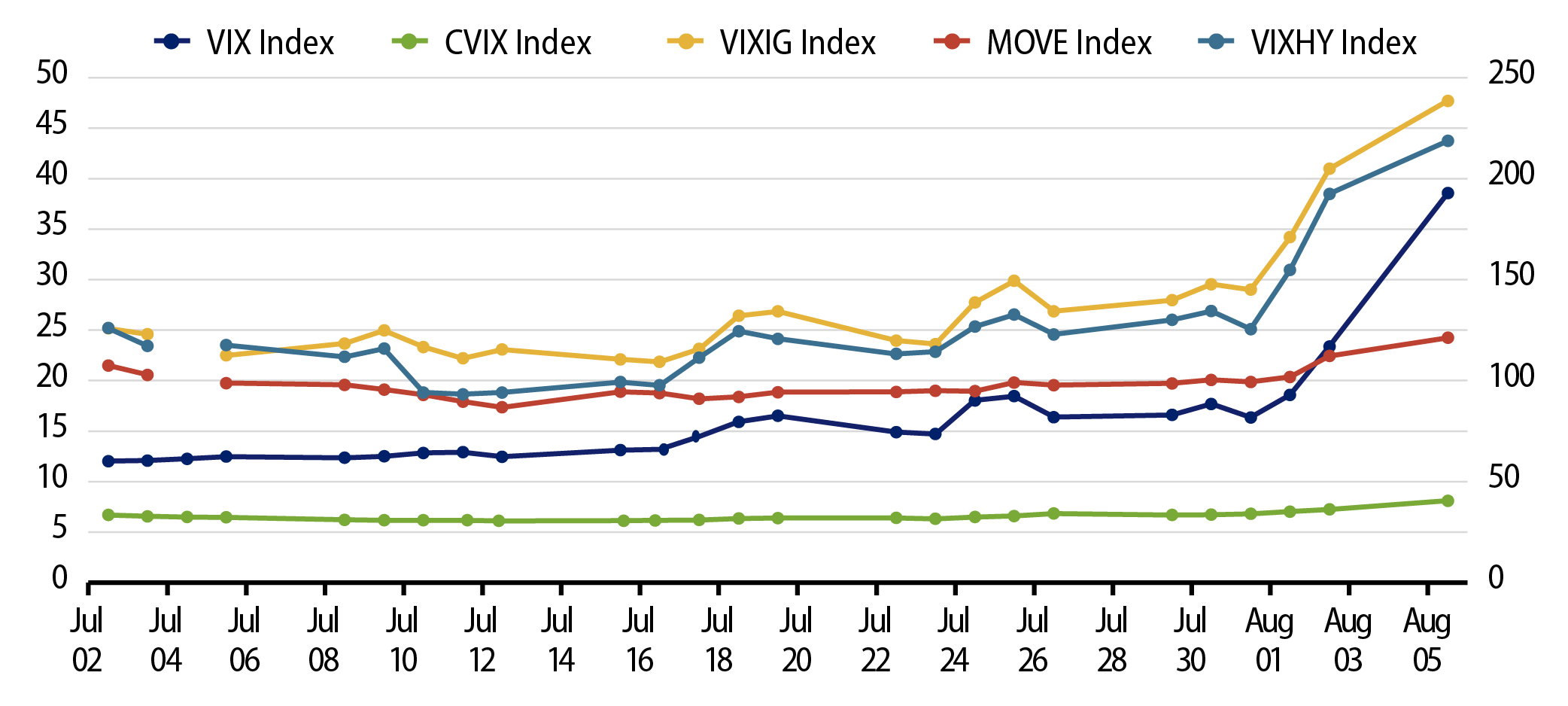

July brought significant factor shifts to markets, triggering unwinds of widely held positions across asset classes, increasing realized volatility, and sending implied volatility in macro markets sharply higher. Global economic data deterioration, major central bank communications, shifting US presidential election odds, and disappointing July US payroll data all contributed to market turbulence.

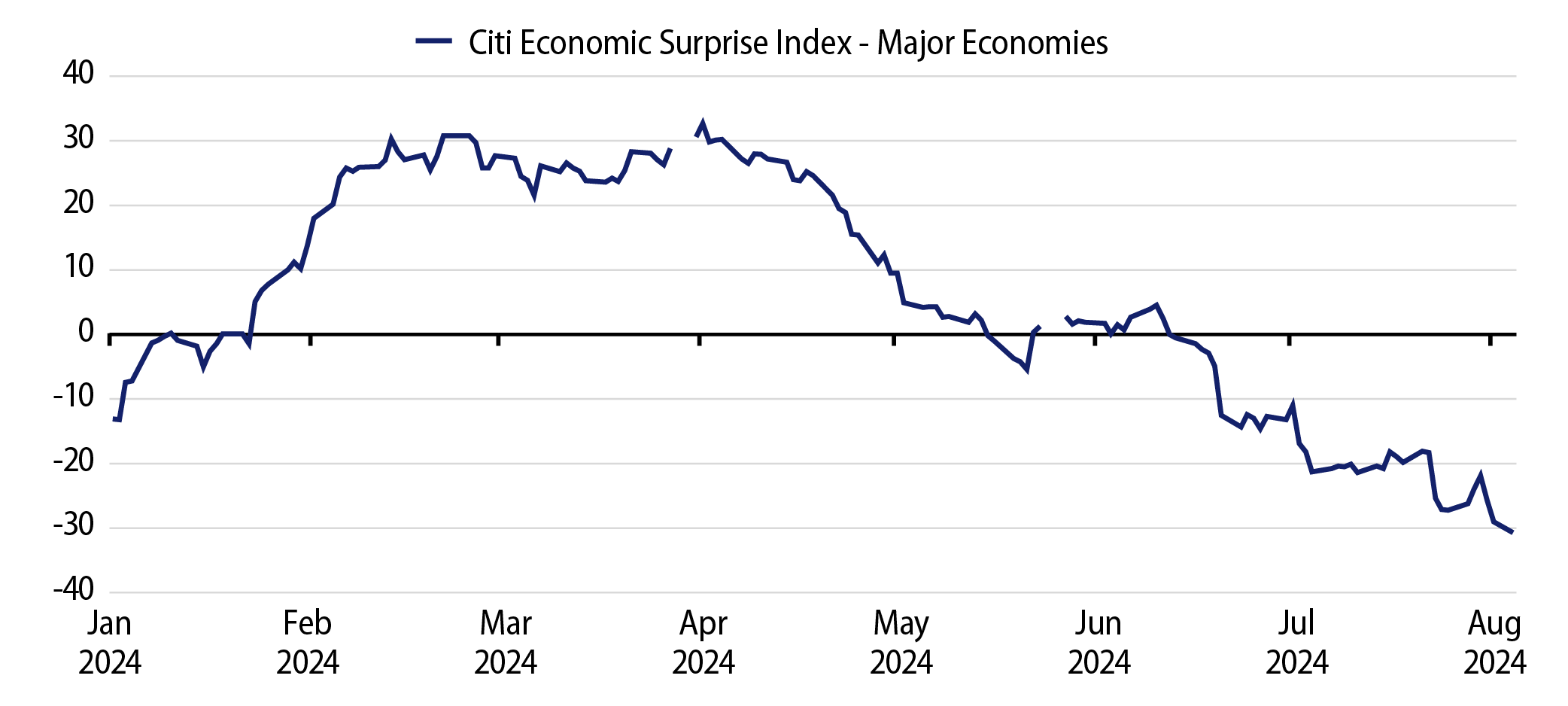

First, economic data from major economies began to underwhelm expectations significantly in July as highlighted by the Citi Economic Surprise Index (Exhibit 2). Notably, China opted to endure economic weakness without injecting fiscal stimulus, which might have supported economic activity amid a housing market adjustment. Elevated rates also likely played a key role in the global data slowdown observed in July.

Second, several major central banks met in July, but it was the Bank of Japan’s (BoJ) rate hike amid a globally deteriorating macro landscape that was particularly significant. The BoJ increased its policy rate from 10 basis points (bps) to 25 bps. Although this was mostly priced in by markets, the move accelerated the unwinding of foreign exchange carry trades. The Japanese yen’s appreciation of over 10% in the past three weeks resulted in the reduction of numerous risk positions, as the yen was central to funding currency carry trades due to its extremely low carry.

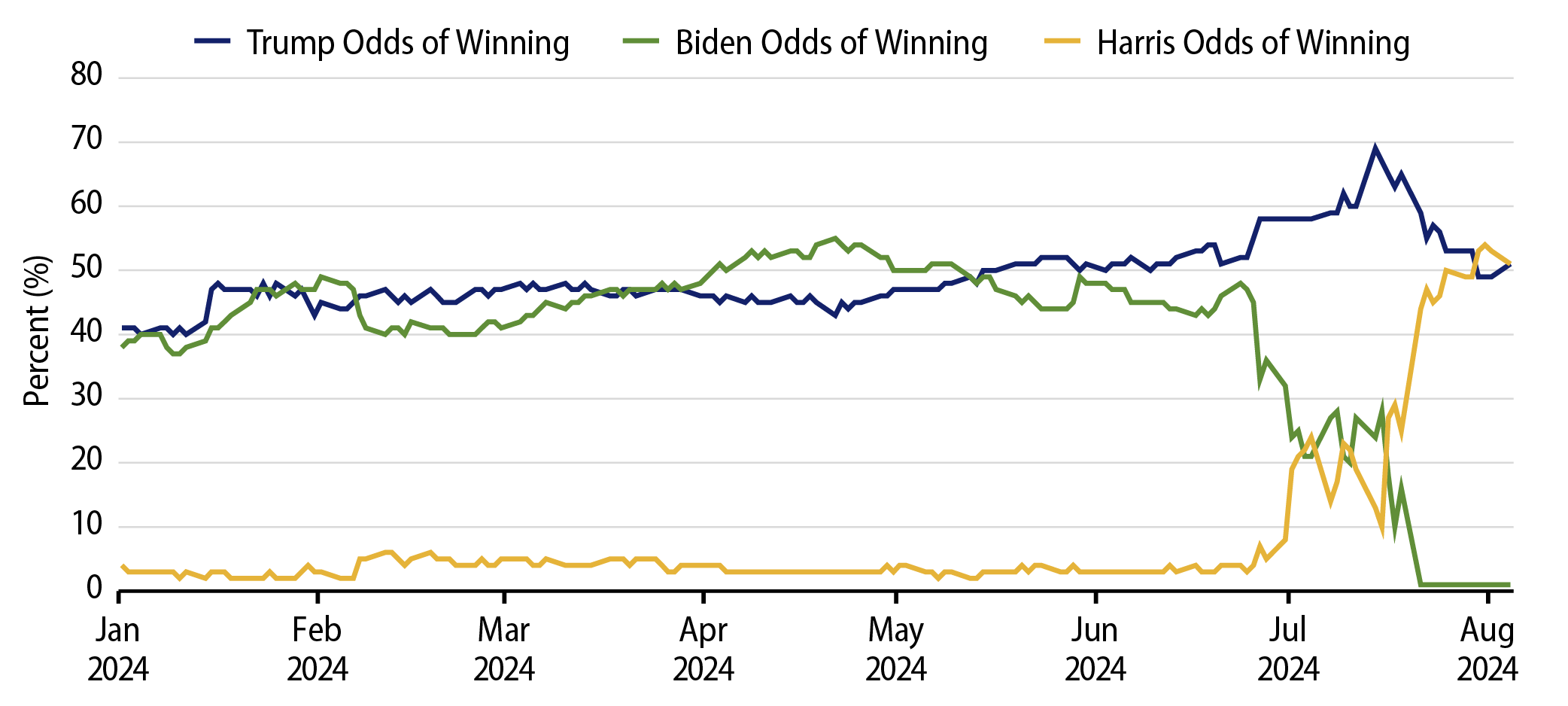

Third, US presidential election betting odds, often used as a simple gauge of candidate lead changes, fluctuated rapidly in July. Former President Trump’s odds of winning surged to nearly 70% on July 19, just six days after a failed assassination attempt during a rally in Pennsylvania. However, President Biden then withdrew from the race and endorsed Vice President Kamala Harris on July 21, leading to an immediate repricing. As of August 5, Harris holds a slight lead in betting markets. Uncertainty about the upcoming administration introduces challenges for corporate capital expenditure assumptions and financial market pricing models, given the candidates’ differing impacts on economic sectors, foreign policy, fiscal spending, and tax policies.

Finally, the release of weaker-than-expected July US nonfarm payrolls on Friday, August 2, intensified concerns about the US employment situation. The US unemployment rate for July rose to 4.3%, triggering worries about economic health, especially with the Sahm Rule coming into play. The Sahm Rule is an economic indicator stating that if the average of the unemployment rate over three months rises a half-percentage point or more above the lowest three-month average over the previous year, then the economy is in a recession. The US economy created 114,000 new jobs in July, falling short of the preceding three-month trend of 177,000 and economist expectations of 175,000 jobs. The impact of Hurricane Beryl on payroll data remains unclear and additional data will be needed for a conclusive assessment. If the next payroll report confirms July’s deterioration, future economic assumptions may require adjustments.

In closing, the collective impact of these factor shifts has been sufficient to unwind and deleverage widely held trades across markets. As an active manager with a long-term fundamental value philosophy, when we observe an aggressive repricing of risk positions during a positioning cleanse, we search for mispricing of assets and investment opportunities.