2015年05月19日時点

April housing starts were better today, with total starts up 20.2% and single-family starts up 16.7%. While these month-over-month gains look fantastic, the fact is they occurred off comparably sharp declines in February, so the April gains leave us only slightly above December 2014 levels. Still, after a torrent of unrelentingly soft data over the last six weeks, today's news is a welcome break.

What does it all mean? Well, when housing starts first weakened in February, the thought was that the drop was weather-related, but when starts stayed soft in March, it started to look as though something more than the weather was in play, that the starts spike in late-2014 was the anomaly, not the winter softening. Today's news points back to the weather story...mostly.

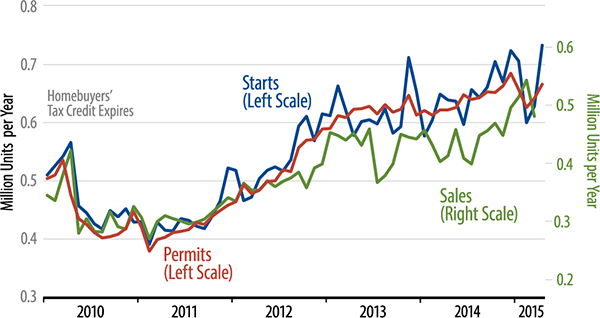

Look at the accompanying chart. Single-family starts (blue line) now look to be holding at a level just above 0.7 million units per year, with the winter declines an aberration. However, developments in housing permits (red line) are not quite as encouraging. Levels there are lower and the April bounce not quite as strong.

Similarly, much of the April bounce in starts occurred in the Northeast and Midwest, where weather certainly was an issue...and if cold weather can understate starts activity there for a month or two, then the relief from that cold weather could well lead to overstated starts for a month or two. In other words, it remains to be seen whether starts level will continue strong or fall back to a lower level.

For now, though, there is no getting around the fact that today's news was a relief. Our concern was that with US manufacturing activity softening, if there was no offset from stronger homebuilding, overall US growth could be downshifting to the 1.0%-1.5% range. The better homebuilding data today give hope that underlying growth rates will continue in the 2.0%-2.5% range that has held over recent years. At present, though, there is no indication of US growth breaking above that 2.0%-2.5% range.