2014年2月26日時点

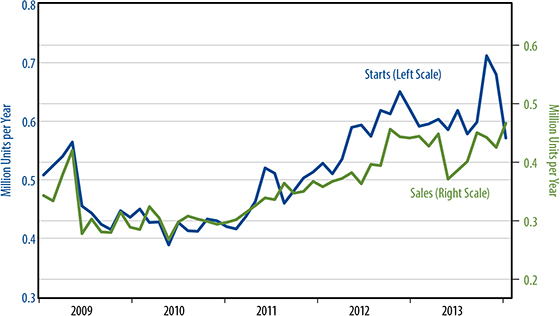

Ultimately, builders won't build homes they can't sell. Last week's piece looked at housing starts, the first step in building a house. Today, we look at the demand side: sales of new homes. The underlying issue is whether US homebuilding will accelerate this year and thus support faster US economic growth. Data on building permits etc. have not been encouraging in this respect, but somehow housing starts surged in late-2013, before the weather-constrained January data discussed last week. So, today, we look at new-home sales to see if the apparent upturn in construction has flowed through to housing demand.

The accompanying chart reprises that from last week, with January new-home sales added in. As you can see, new-home sales are one indicator that did NOT suffer a weather-induced decline. Instead, sales rose, though this hike looks mostly to be payback of November/December declines.

However, as seen in the accompanying chart, this is not (yet) the case for housing starts. Those explosive gains in November and December starts still stand, and, again, it is possible to attribute the January decline to the Polar Vortex. Indeed, the January starts' declines were wholly contained in weather-affected regions, though those are also where the previous jumps occurred.

On balance, new-home sales trends look steady. Maybe the January gains are the beginning of a sustained trend, but more likely they are a random fluctuation within an otherwise steady trend (similar to the summer 2013 swoon).

Now, steady is not bad, but it is not accelerating. Nothing in recent home sales data supports the outsized levels of housing starts seen in November and December. If homebuilding reverts to a steady 2014 annualized pace of 600,000 single-family starts and 450,000 new-home sales, that might be just fine for the housing market, but it indicates zero boost from housing to GDP growth and so zero support for contentions that GDP growth is accelerating and bond yields have to rise. While the housing data are not conclusive on this as yet, that zero boost story seems most likely to us at this point.