2014年4月30日時点

Quarterly GDP data are especially littered with various fluke factors distorting growth either up or down. For the 1Q14 data released today, it is well known that the winter blizzards significantly restrained consumer spending, exports, and other GDP components. What garnered less publicity is that there were also a number of "one-time" factors pushing 1Q14 growth higher than it otherwise would have been.

That same winter weather that kept people out of the stores also kept them home with the thermostat turned up, "overstating" spending on utilities just as spending on goods was "understated." Similarly, the rebound from the October government shutdown resulted in a larger-than-otherwise gain in government outlays. Finally, government statisticians have judged that the onset of Obamacare led to very sharp increases in Amercians’ health care consumption.

Together, these factors served to boost 1Q14 GDP by as much as 1.7 percentage points. Even with these "assists," GDP growth came in at only 0.1%, thanks in part to somewhat larger "drags" from the winter effects on consumption, etc. We can expect better growth in 2Q14, but a barnburner number is unlikely, given that both the "boosts" and the "drags" within 1Q14 GDP will be reversed in 2Q14.

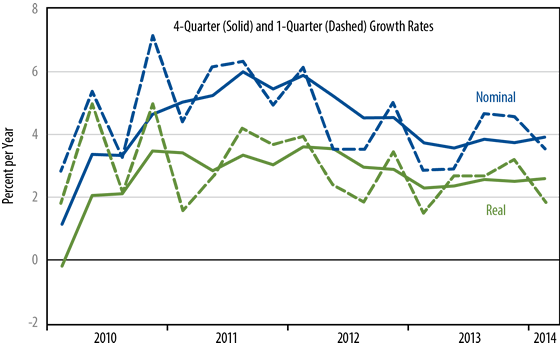

Beneath the noise, the underlying trends in GDP growth do not support the optimism that has recently swept across the Federal Reserve (Fed) and the Street. As seen in the chart, growth in real private-sector demand has actually decelerated over the last two years, and nominal (dollar) private demand has slowed even more sharply. While the drag from government spending may well subside later this year, we are not seeing the strength in private-sector spending that would bode well for rapid overall growth.

Meanwhile, the Fed has widely lamented the decline in inflation over the last two years. However, with nominal spending having slowed so sharply, the decline in inflation may have prevented a more severe slowing in real demand than we actually saw. No, the economy is not falling off a cliff, but neither is it exhibiting even the modest acceleration that the Fed and the Street have been calling for, even when the various fluke factors (both up and down) are accounted for.