2014年9月18日時点

With housing-starts releases, it is usually best to look beyond the headline data and focus on single-family activity. Multi-family data jump wildly from month to month, distorting the headline numbers. Moreover, multi-family units take a lot longer to complete, and both builders and occupants spend a lot more per unit on single-family homes than on multi-family units.

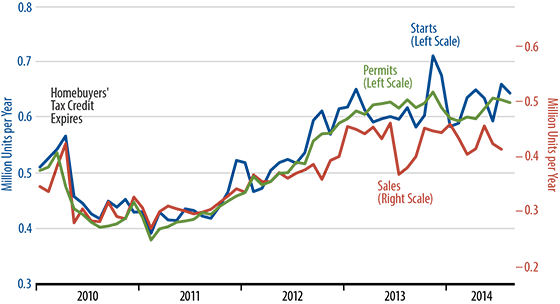

So, while last month’s housing-starts release showed a huge 22.9% increase, that gain was mostly due to a sharp increase in multi-family units, and today’s August data reversed most of the July spike. The real news concerns what is going on with single-family activity, and the accompanying chart tells that story.

Basically, there is no story. Single-family activity has been flat since late-2012, and flat trends have continued recently. (Note that single-family activity went flat more than six months before the June to September 2013 rise in mortgage rates, so keep this in mind next time you hear someone blame housing’s sluggishness on higher mortgage rates.)

The last two months of swings in single-family starts are, of course, much milder than those in multi-family starts. Meanwhile, upon adjusting for coverage differences—as per the chart—(single-family) new-home sales also remain flat, but at a level lower than is consistent with ongoing levels of single-family starts. In other words, builders are starting homes faster than they can sell them, and while home inventories are not oppressively high, they are rising steadily.

While the multi-family market is more volatile than the single-family market (flat since late-2012), its underlying trends are not much different, as it has been flat since late-2013.

As discussed in the last installment of By the Numbers, August retail sales data give some glimmer of hope for faster growth. However, there is nothing in the homebuilding data indicating any such recent improvement.