Payroll jobs stunned to the upside in December, with the private sector adding 275,000 jobs on top of 312,000 and 240,000 gains in October and November, respectively. The latter two gains represent substantial upward revisions from what was reported last month.

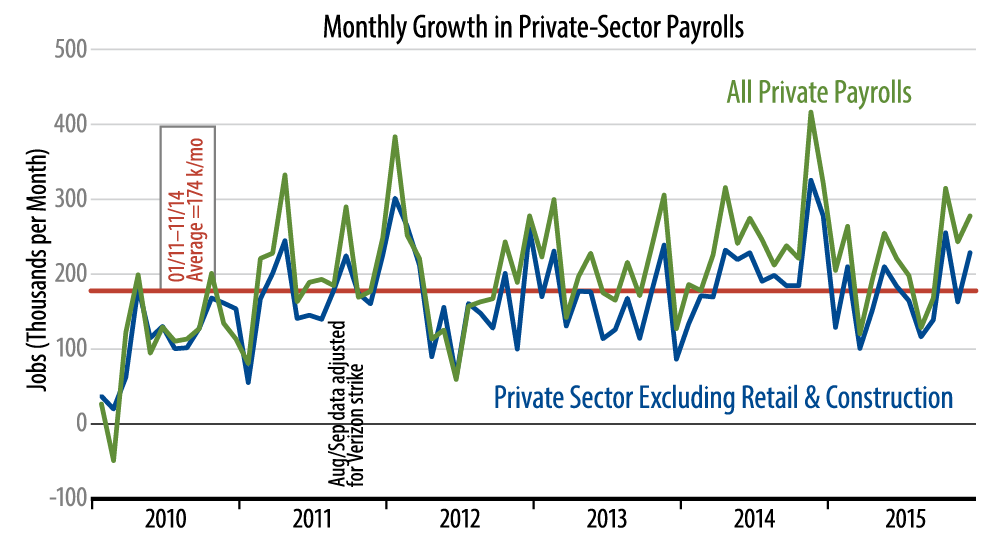

Meanwhile, the measure we focus on, payrolls excluding construction and retailing (the blue line in chart) added 226,000 jobs in December, following gains of 252,000 and 160,000 in October and December. These gains should be compared to an average gain of 174,000 per month over the preceding four years.

For 2015 as a whole, this ex-construction/retailing measure showed average growth of 168,000 per month, slightly below the 174,000 average for 2011–14. Total private-sector payrolls showed average monthly growth of 213,000 in 2015, exactly equal to the average growth rate of 213,000 over 2011–14.

In other words, while job growth finished 2015 with a flourish, overall growth for the year was merely in line with the trends of the last four years. Those who think the labor market is chugging along famously will be reassured by this fact, but those who think something is missing will also find that this fact comports with their position.

It is possible there was some seasonal noise within recent swings. On an unadjusted basis, construction jobs were -60,000 in November and -151,000 in December, before seasonal adjustment changed these to +45,000 and +48,000, respectively. Unusually warm early-winter weather back east may have retarded the pace of winter shutdowns by construction companies, resulting in strong data on a seasonally adjusted basis. Other industries could be experiencing similar “seasonal” anomalies, though to a lesser extent.

We won’t know for sure whether this is the case until February and March, when the seasonal swings start to reverse. (Workers who weren’t laid off for seasonal reasons in late-2015 can’t then be rehired for seasonal reasons in early-2016).

Once again, overall job growth was strong in 4Q15, but average for the year as a whole. This contrasts with other data suggesting that 4Q15 GDP growth will be exceptionally soft, likely less than 1%. Clearly, the connection between job growth and economic growth is sometimes tenuous.