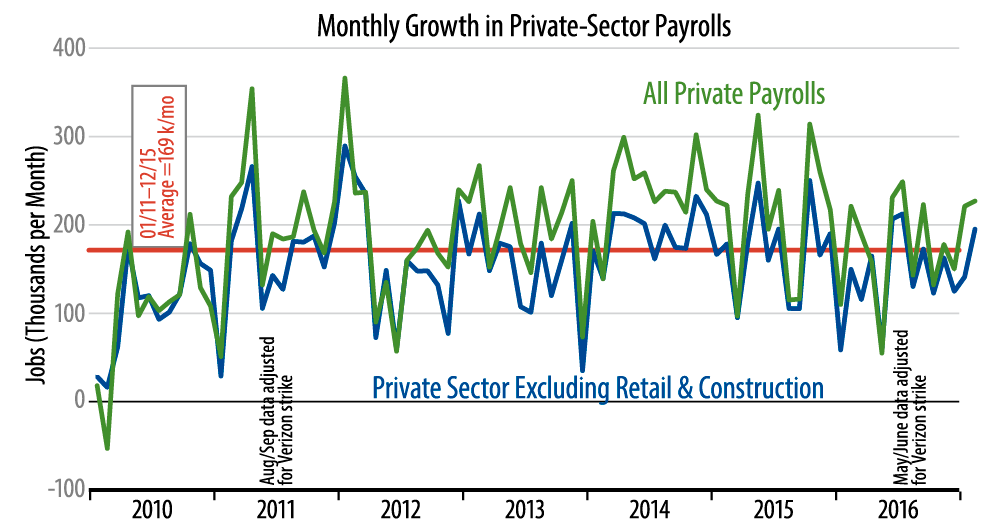

Media reaction we’ve seen is that the February news was favorable, and we have no quarrel with that take. The 195,000 February gain in our favored jobs measure is above the 169,000 per month average seen over 2011–15. Where we part company with common perception is with respect to previous months' data. We have emphasized that job growth had been below pre-2016 trends for most of last year and continued so in January, so we see the February gains as the first decent monthly gain since July.

Whether we are at full employment or not, slower growth in jobs means slower growth in personal income, which almost always means slower growth in consumer spending and GDP, and growth has indeed been slower for the past year or so. Meanwhile, however, market and Federal Reserve expectations are rooted strongly in faster economic growth in 2017. Again, the jobs data through January suggested otherwise, but we have seen a mild break to the upside in February. We'll see if that continues.

One clearly favorable aspect of the jobs news was manufacturing, where payroll jobs rose by a hefty 28,000 in February, 27,000 of those in production worker jobs, and where January data were revised upward by 13,000. A weak manufacturing sector had been the dominant factor holding overall growth down in recent years, so the better activity here is clearly a favorable sign (See also our February 27, 2017 By The Numbers).

In other sectors, construction saw a whopping 58,000 job gain, while retailing lost 26,000 jobs. Again, we would interpret both these swings as seasonal noise. On net, retailing has added a mere 14,000 jobs cumulative over the last four months (spanning the Christmas season). The very strong February gains for construction likely mostly reflect very mild winter weather.

Again, even apart from construction and retailing, overall job growth was better in February, following a string of five subpar months, and the factory-sector payroll data were especially favorable. Hourly wage data were better in February, but not enough to reverse the slowing growth trend of recent months.