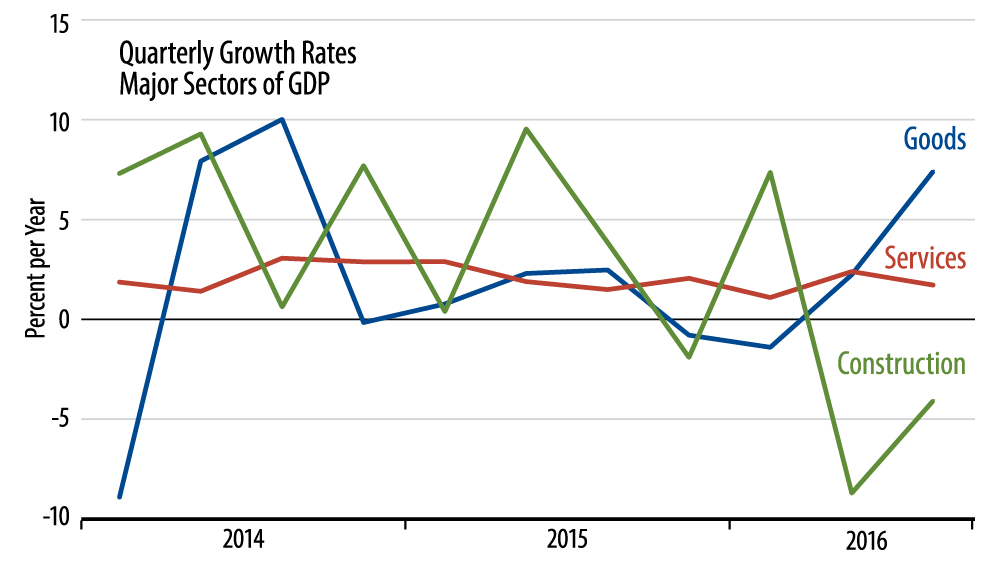

How could GDP accelerate when consumption spending, 70% of GDP, slowed markedly, and fixed investment declined? The data show massive increases in exports and inventory investment. As you can see in the accompanying chart, the 3Q16 GDP acceleration was driven by a sharp acceleration in goods sector growth, to 7.4% in 3Q16 from 2.2% in 2Q16.

Now, the “goods sector” essentially means manufacturing, so the GDP data imply a very sharp 3Q16 acceleration in US manufacturing output. This runs counter to all the other 3Q16 data we received on the factory sector.

Payroll data from the Labor Department show manufacturing losing 32,000 jobs in 3Q16, with total production hours declining. Industrial production data from the Fed show a scant, 0.8% 3Q16 rate of growth in factory output. Factory shipments data from the Census Bureau are on pace to deliver 0.4% growth. Yet, the GDP data imply a 3Q16 explosion in the US manufacturing sector.

A colleague once referred to this as the “space alien effect.” The GDP data suggest a large increase (or decrease) in goods production, but nowhere in the supporting data is there any indication of just who produced this increase (decrease). Maybe it was space aliens!

Suffice it to say that we are skeptical. And no, I’m not suggesting anything untoward or intentional. This is a huge economy, and sometimes, “bad” data just happen.

Whether or not the 3Q16 growth is for real will likely not make a difference for the Fed. This growth pickup is all it needed to sustain its intentions of a rate hike in December. Where the analysis here will make a difference is down the road. If today’s 3Q16 news is as shaky as I suspect, there will be no follow through in 4Q16 or early 2017, and the economy will stay in much the same funk as it has suffered through since early-2015, that is, mid-1% range underlying growth.