2014年7月24日時点

Today's new-home sales release showed nothing going on in the new-home market, with a June sales decline erasing a modest increase in May. While this message might seem nondescript, it is actually of significant interest. Buried in the details was a huge, downward revision (-12.3%) to May data.

The May new-home sales data released a month ago sparked calls in some camps that homebuilding might be perking up after 18 months of torpor. With the May revision and June decline, we can only invoke Saturday Night Live's Emily Latella (aka Gilda Radner) and say, "Never mind."

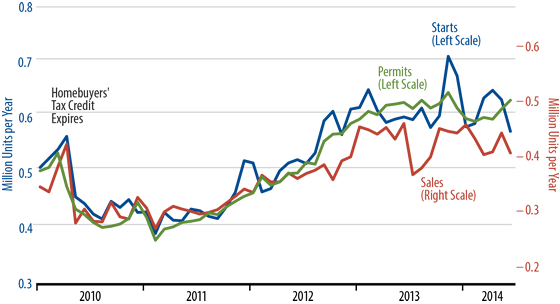

The chart tells the story. Both single-family starts and sales have been trending sideways (or slightly downward) since January 2013, well before mortgage interest rates started to rise.

The chart puts starts and permits on a different scale from sales in order to allow for owner-builds (which show up in permits and starts, but not in sales). By this relative scaling, since late-2012, new-home sales appear to have been proceeding at rates insufficient to match those of single-family homebuilding. Indeed, over the same period, inventories of unsold new housing have risen steadily. So, the rise in home inventories tends to confirm the relative scaling indicated by our graph.

It is commonly claimed that home inventories are "low" because inventory-sales ratios are lower than during the height of the housing bubble (2006–07). It is not clear that this is the proper perspective. Inventory-sales ratios are higher than at any time over 1998–2005, when the housing bubble was gaining steam, and this may be a more telling comparison for home inventories.

Even without any suggestion of home inventories being too high, it is still the case that all the homebuilding metrics in the chart firmly contradict any notion that homebuilding is currently on the upswing. The possibility of inventories becoming uncomfortably high just adds fuel to the "non-fire" that is the homebuilding market. All in all, the range of homebuilding data points to housing activity being steady at best, which is consistent with our outlook for no acceleration in US GDP growth.

Note: By The Numbers will take a summer vacation over the next two weeks.