We made a big deal out of the downward revisions to July payroll job growth (see our "By The Numbers" installment from September 7), but while those revisions took a big bite out of monthly job growth, they amounted to only 0.05% of total jobs, so there was only a negligible revision to July personal incomes.

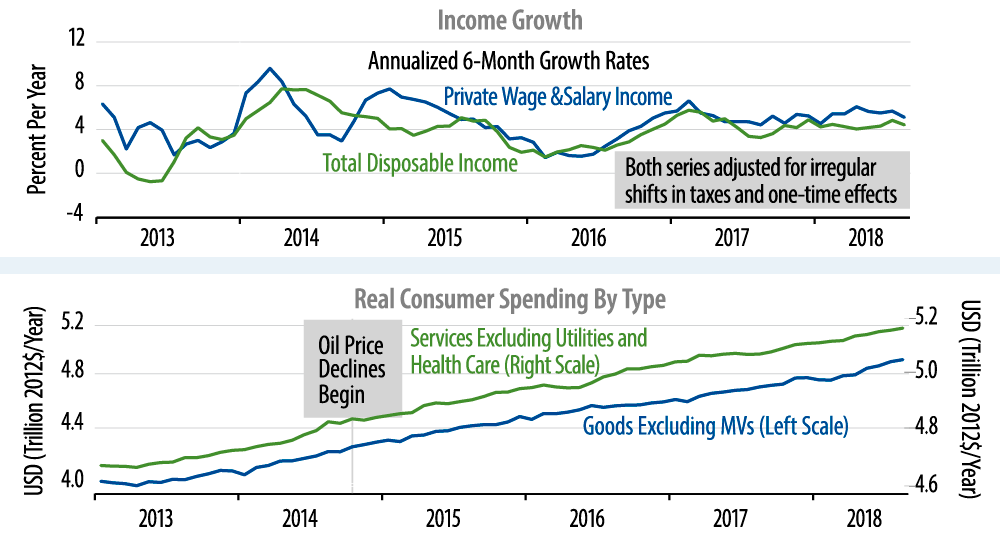

The first chart shows the underlying trends in disposable income and private-sector wage and salary income. The chart excludes the effects of the 2017 tax reform, and that change did boost disposable income growth early this year. Apart from that fiscal policy boost, though, you can see that income growth has been quite steady, which would seem to fly against consensus expectations for faster growth in consumer spending.

As for consumption activity, we have had some nice boosts to retail sales growth in both May and July, and you can see that reflected in goods consumption growth (blue line in second chart). Underlying services consumption, however, has been only steady.

Our outlook for consumption has been less upbeat than the consensus in that we expect steady growth there, at about the same pace as we have seen across recent years. The income growth and services consumption data have been in line with that, but goods consumption has been more buoyant in recent months. We’ll see whether that continues to be the case in months to come.