2014年4月04日時点

While financial markets were hoping for clarity from today's payroll jobs report, there was little chance they were going to get it. After the wild, apparently weather-induced swings of recent months, job growth was due for a "catch-up," an offset of those weak prints. So, it would have taken an extremely strong gain, something near 300,000 jobs, both to offset previous softness and also to point to the stronger growth trend that the markets and the Federal Reserve are betting heavily upon.

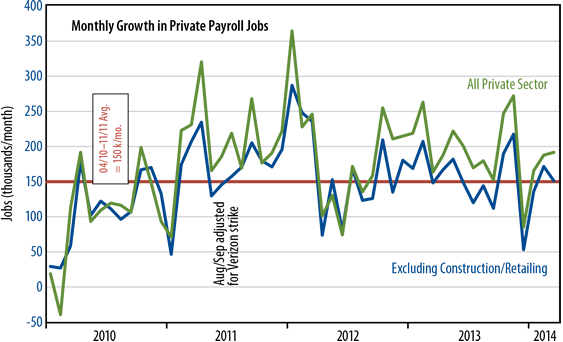

As it was, the actual payroll gain of 192,000 private-sector jobs—plus +47,000 of revisions to previous months' growth—was right in the range of middling growth. Yes, there was some catch-up from the winter softness, but today's gains were not strong enough to even suggest any acceleration in growth trends.

As you can see in the accompanying chart, job growth has been bouncing around a stable trend. The very weak

December number balances the above-trend prints of October/December and February/March.

In fact, looking at the "core" jobs indicator depicted by the blue line in the chart—private payrolls' net of especially volatile construction and retailing—average growth over the last six months has been 154,000 per month, virtually dead on the 150,000 trend that has held since 2010.

So, there actually is some clarity in today's data. Job growth is neither speeding up nor slowing down, but merely wiggling around a sluggish but stable trend. This is no consolation for those expecting an acceleration to 3%+ GDP growth this year. However, it does dispel any latent fears of economic growth weakening. And the stable, sluggish growth depicted by these data is right in line with our expectations.