Inflation globally looks to be trending lower, while a growing number of central banks are nearing the end of their rate-hiking cycles. Looking ahead six to 12 months, what do you expect regarding global bond performance?

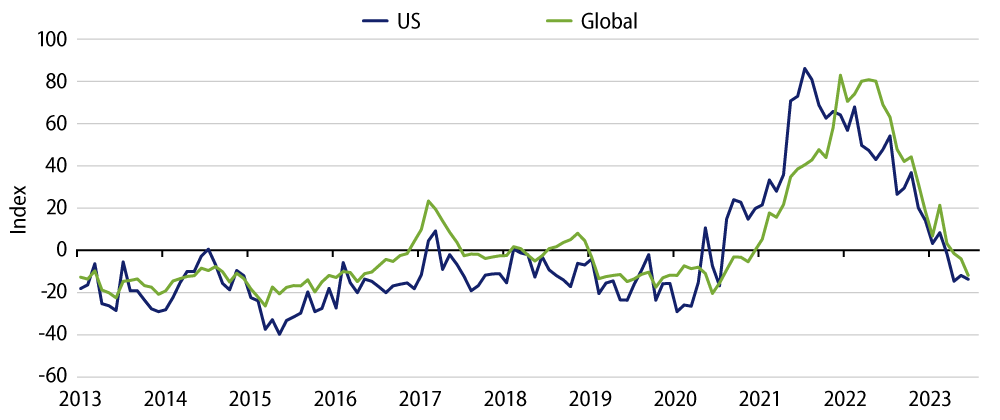

We think the stage is set for global bonds to outperform. First, the most opportune time to invest in a country’s fixed-income market is when its interest-rate cycle is stabilizing or poised to decline. These outcomes are already playing out across a number of emerging markets (EM) and are about to materialize over the next few months in key developed markets (DM) such as the US, Europe, the UK and Australia. Global government bonds are increasingly pricing in these outcomes especially as incoming economic data suggests weaker growth and inflation could surprise to the downside (Exhibit 1).

Second, it’s important to factor in the direction of the US dollar (USD). Last year, the USD surged higher mostly on the back of the Fed’s aggressive rate-hiking campaign. Since the USD’s peak last September, improving global growth prospects and a narrowing interest-rate differential have pushed the USD lower. We see a possibility that the dollar moves sideways from here in the short term, but we expect it to depreciate somewhat over the longer term as the global economy and sentiment rebound. In periods of extended USD weakness, non-US assets have tended to perform well.

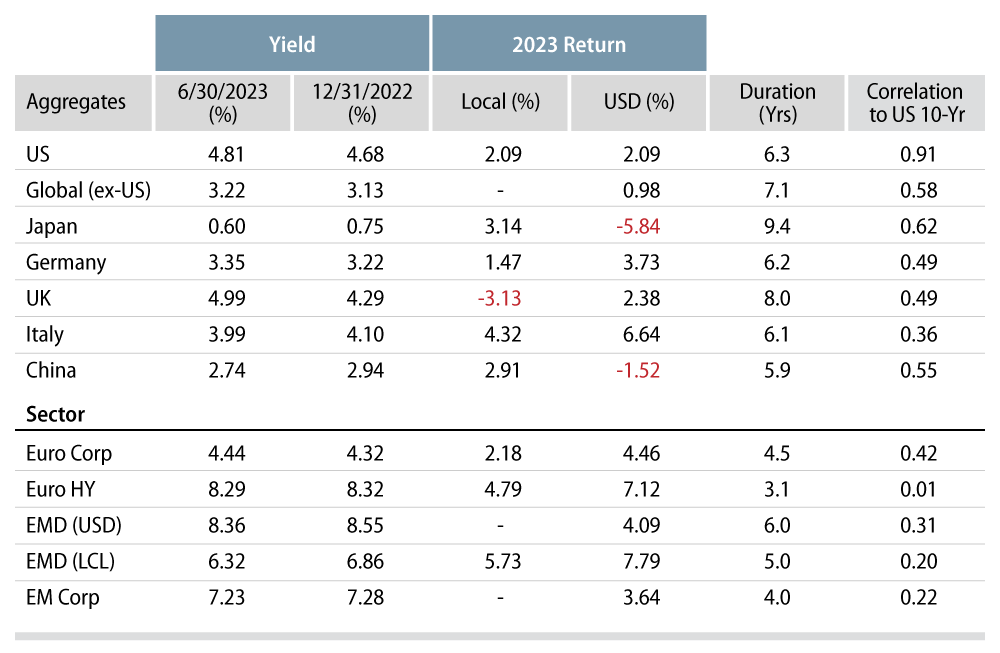

Third, we need to factor in valuations. Global bond yields surged last year due to the sharp rise in global inflation and the aggressive rate-hiking campaign by central banks. Yields, in some markets, moved even higher in recent months on the back of idiosyncratic risks: for example, in September 2022, yields of UK government bonds (gilts) spiked due to mini-budget concerns; in December 2022, Japanese government bonds (JGBs) were roiled by the Bank of Japan’s (BoJ) surprise adjustment to its yield curve control (YCC) framework; and in March/April 2023, short-dated US Treasuries (USTs) exhibited unprecedented volatility due to regional bank turbulence and fears of a possible US default due to the debt ceiling standoff. Each of these episodes offered asset managers such as Western Asset an opportunity to add value for investors by capitalizing on these market dislocations. Exhibit 3 presents a snapshot of the compelling yield, return and diversification benefits currently offered by global bonds.

Which major government bond markets look attractive to Western Asset at this time?

The following list describes our relative value views by global region. For more information on the key drivers supporting our views and our thoughts on other areas of the global fixed-income markets, please refer to our 3Q23 Global Outlook.

Global Market Rates: Relative Value by Region

+/- Canada: With the front end now fully repriced for likely Bank of Canada (BoC) hikes, bonds are again fairly valued versus their US counterparts. The recent gains in the Canadian dollar have put the currency close to fair value.

+ UK: We feel that the market is expecting too much in terms of Bank of England (BoE) rate hikes, and therefore gilts should outperform.

+ Europe: We believe that the ECB runs the risk of tightening policy by too much. Weaker growth and falling inflation should allow the ECB to stop hiking in H2, which will support euro area bond yields.

+ China: We expect the PBoC to maintain low rates in 3Q23 and thereafter shift to a more normalized monetary policy stance.

- Japan: We expect higher Japanese government bond (JGB) yields. If the Bank of Japan (BoJ) adjusts its monetary policy further, the nominal 10-year yield would lead the move higher.

+ Australia: We remain tactical in the 10- and 20-year parts of the curve on further Reserve Bank of Australia (RBA) action.

Based on your view of a weaker USD over the longer term, which DM currencies do you think offer alpha-generating potential?

Here we provide our views on four currency markets:

- Japanese Yen (JPY): We anticipate a stronger JPY. We envision a scenario where new BoJ leadership reviews monetary policy and continues to tweak its set of current policy tools further in addition to the change in July (resulting in higher JGB yields) while the Fed pauses its rate hikes. That would be supportive of the JPY versus the USD. Moreover, we expect the JPY to benefit from a cyclical rebound as Japan continues to reopen its country to tourism.

- Australian Dollar (AUD): We’re anticipating a stronger AUD. We expect the global economic downturn brought about by sharply tightened and concerted monetary policy will eventually lead to stronger risk appetite as markets begin to look past the malaise. In this case, the AUD will be a likely beneficiary while the Australian economy is expected to outperform due to the more cautious approach taken by the Reserve Bank of Australia on tightening.

- British Pound (GBP): We anticipate a weaker GBP. The currency recovered from September’s mini-budget weakness. However, we expect growth headwinds, uncertainty over long-term fiscal support packages and a more dovish approach from the Bank of England in relation to its DM counterparts to reduce the tailwinds for the GBP. A further escalation of the relationship with the EU (though not our base case), could lead to further downside for the GBP.

- Euro: We’re neutral on the euro. There may be appreciation potential over the medium term should the geopolitical risk premium stemming from the war in Ukraine decline, but a protracted reduction/halt of Russian energy flows could entail rationing in the European economy and create downside risks to growth and the euro. That stated, one way to capitalize on upside European growth risks is through the Swedish krona (SEK) which is often driven by global and European economic activity and broad risk sentiment. That has been a headwind this year. Should the growth outlook improve, and uncertainty decline, we expect the SEK to strengthen.

Since all arrows are pointing to more central bank easing and a lower yield environment, shouldn’t investors just take a passive approach to global bond investing?

No. It’s important to bear in mind that economic cycles, fiscal policies and central bank policies don’t move in tandem. There’s substantial variance among the change and movement of absolute yield levels, slopes and shapes of government bond curves, both within and across countries. For example, in the EM world, the Central Bank of Mexico has paused its rate hikes while the Central Bank of Brazil looks poised to make its first rate cut. In the DM world, the Fed looks like it’s nearing the end of its hiking cycle while the BoJ might look to continue tweaking its current set of policy tools further to push rates higher. To complicate matters, market participants are constantly trying to identify catalysts that might influence the drivers and direction of each of these markets, which can sometimes generate bouts of volatility. What all of this means is that investors need to be very thoughtful about which countries to own and where duration is held along that country’s yield curve. We believe the most effective way to accomplish this—while at the same time trying to navigate through periods of volatility—is by embracing an active approach to global bond investing.