Concerns about the extent and impact of Trump’s tariffs, the direction of US fiscal policy, and uncertainty surrounding Federal Reserve (Fed) policy and US Treasury (UST) issuance have once again raised questions about the global appetite for USTs. However, we believe the risk of a buyers’ strike for USTs is overstated, given the diversity and depth of the market’s buyer base as well as the increasing mix of global economic and geopolitical risks that have investors on edge.

In a previous blog post, we noted that although demand for USTs from countries such as China and Japan might decline due to rising yields and a stronger US dollar (USD), other sources would compensate for this shortfall. This is because the USD remains the world’s reserve currency, and USTs are widely recognized as the world’s safe-haven asset. A notable example occurred in 2023 when 10-year UST yields spiked 200 basis points over the year to exceed 5%, triggering widespread fears of a prolonged buyers’ strike in the UST market. Instead, households (which include US hedge funds and personal trusts), mutual funds, insurers and pension funds all stepped in to fill the demand gap left by foreign investors and US banks.

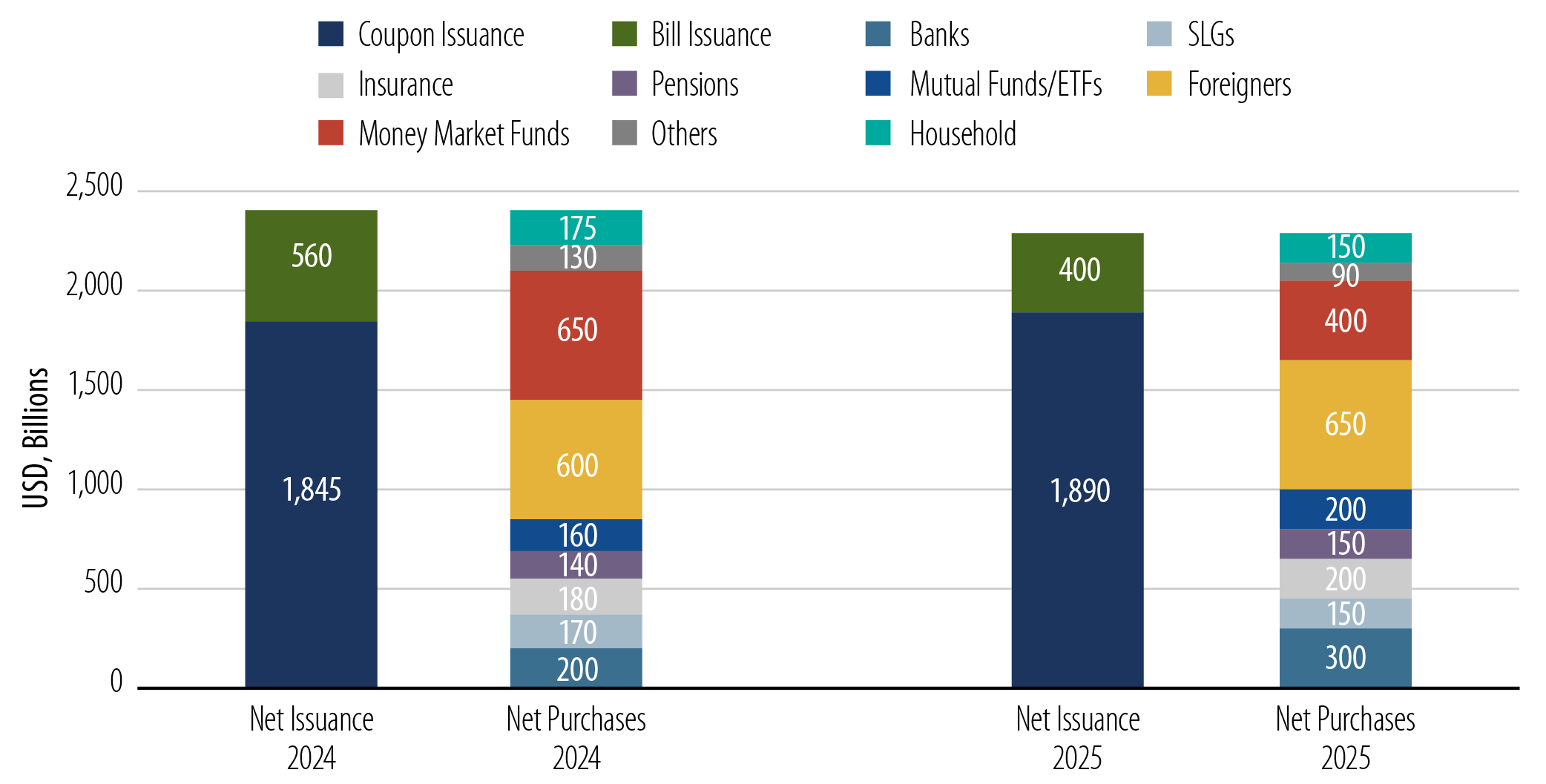

With this in mind, we anticipate that the demand drivers underpinning the UST market will continue to evolve as global conditions change. Exhibit 1 highlights Fed projections for 2025 UST supply and demand. Compared to 2024, net issuance is expected to decline, while foreign investors, US banks, insurance companies and pension funds are expected to surpass money market funds (MMFs) and households in absorbing this year’s UST supply. Let’s take a closer look at the dynamics of some of these market participants.

Foreign Investors

While mainstream media reports highlight a decline in foreign ownership of USTs as part of a broader appetite problem, it’s crucial to understand the underlying factors. The growth of foreign exchange (FX) reserves globally has stalled due to the waning globalization trend over the past three decades and a broader push by some countries toward de-dollarization. These changes have resulted in lower foreign official demand (mostly from central banks) for USTs relative to the pace of issuance, thereby reducing the share held by foreigners.

The trajectory of US policy rates also has a significant, cyclical influence on foreign demand for USTs. In a rising rate environment, which also strengthens the USD, central banks may sell US assets, including USTs, to support their own currencies. Additionally, some foreign private investors might sell US assets due to higher costs associated with hedging against currency fluctuations. Indeed, according to the US Treasury, foreign ownership of USTs has decreased from 50% in 2013 to 33% currently, which aligns with the rise in rates over the past decade.1

Currently, US Treasury officials observe mixed US economic data, sustained USD strength, uncertainty over Trump’s tariffs and cross-currency hedging costs as headwinds for foreign official demand, which also includes activity across entities such as governments and sovereign wealth funds. However, foreign private demand remains robust, driven by price-sensitive investors such as hedge funds domiciled in the UK, Euro area, and the Cayman Islands.2 These investors are motivated to exploit basis trade opportunities (i.e., taking advantage of price differences between related financial instruments) and capitalize on attractive yield differentials. Should UST yields decline due to slower US growth, this could weaken the USD and serve as a catalyst for additional foreign demand for USTs.

Banks

Bank demand for USTs and mortgage-backed securities (MBS) is highly dependent on deposit and loan growth. Over the past two years, a combination of risk management considerations, deposit outflows, unrealized portfolio losses following the regional banking stresses in the spring of 2023, and uncertainty around the timing of rate cuts have stunted UST demand. Currently, Treasury officials note that changes to deposit assumptions and regulatory developments related to capital requirements could see banks allocating away from agency MBS to USTs, with a focus on shorter-dated (2-3 year) tenors versus the belly (5-7 year) of the curve.3 These regulatory developments include changes to the Total Loss Absorbing Capacity (TLAC) and Liquidity Coverage Ratio (LCR) rules, which could make USTs more attractive to banks. Additionally, if the Fed reduces the GSIB (Global Systemically Important Bank) surcharge, that would free up capital and potentially increase banks’ demand for securities, including USTs.

Money Market Funds

Demand for MMFs tends to increase during Fed hiking cycles, as these vehicles can pass on higher policy rates to investors through higher yields. However, MMFs also attract inflows just before Fed rate cuts because they can slow the decline in yields by extending the weighted average maturity (WAM) of their portfolios.4 This makes MMFs more attractive compared to other cash-equivalent alternatives such as short-term bank certificates of deposit. Over the past year, the combined impact of an inverted US yield curve and fixed-income market volatility turbocharged inflows into MMFs. According to the Investment Company Institute (ICI), US MMFs totaled $7 trillion as of February 26, 2025, with $2.8 trillion and $4.2 trillion representing retail and institutional investors, respectively.5 Looking ahead, continued demand for MMFs, along with a controversial regulatory rule around minimum liquidity requirements that may shift assets from prime funds to government and Treasury funds, could provide additional tailwinds for T-bills as well as short-dated coupon and floating-rate notes.6

Pension Funds

Since the global pandemic of 2020, the largest 100 US corporate defined benefit pension plans, as measured by the Milliman 100 Pension Funding Index, have shown a surplus, meaning the market value of these plans’ assets exceeds their future liabilities. This surplus incentivizes pension plans to de-risk by shifting investments from equities to USTs. Higher interest rates help keep these pension plans overfunded, which could further increase their demand for long-term USTs. Moreover, with pension plans’ funded ratios estimated at 106% as of January 2025, plan managers have more incentive to de-risk their portfolios, adding to UST demand.7

In Closing

In any discussion about UST demand, it’s essential to address the recent shift in the correlation between equity and fixed-income. Over the past two years, this correlation turned positive—primarily due to a global inflation shock—marking a significant change after two decades of negative correlation. This pivot reduced the diversification benefits of USTs in portfolio construction and contributed to a rise in the term premium, leading to a decrease in UST demand via household and mutual fund outflows.

However, with further signs of US inflation moving closer to the Fed’s 2% target and historically tight spreads in certain areas of the credit market—all against a backdrop of waning US exceptionalism and geopolitical tensions—we believe investors will increasingly embrace USTs as a valuable risk mitigation tool in their broad investment portfolios.

From a value perspective, it’s worth noting that UST yield levels are currently as high as they have been for the better part of the past 20 years. These levels provide investors with an additional buffer against rising rates and more price appreciation momentum in a scenario of declining rates. In short, UST yields in today’s market offer domestic and international investors a strong incentive to capitalize on attractive carry and total return potential—an assertion that was difficult to make only three years ago.

ENDNOTES

2. US Department of the Treasury (5 Feb 25). Minutes of the Meeting of the Treasury Borrowing Advisory Committee.

3. US Department of the Treasury (Jul 24). Development in demand for US Treasuries.

4. Note that asset managers can’t extend WAM indefinitely. SEC rule 2a-7 imposes limitations of 60 days (and 120 days for weighted average life).

5. Investment Company Institute (27 Feb 25). Money Market Fund Assets.

6. Investment Company Institute (5 Feb 25). Sold Under False Pretenses: The SEC’s Money Market Fund Reform is Causing Damage.

7. Milliman (10 Feb 25). Pension Funding Index February 2025.