2014年3月26日時点

Contrary to our forecast of continued languid growth in 2014, the Federal Reserve and most of Wall Street think US growth will accelerate to 3% or better in 2014. Much of this cohort thinks this acceleration already began to occur in late-2013. The better growth is supposed to be driven by faster spending growth on consumer goods, capital goods, and housing.

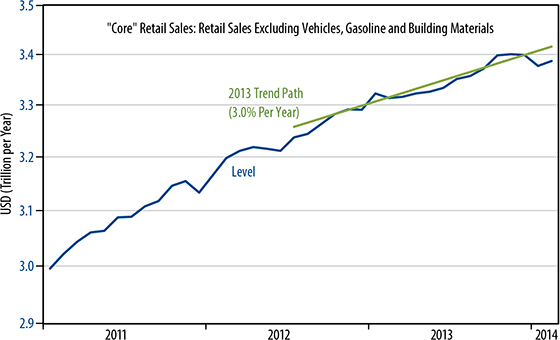

As pointed out in previous "By the Numbers" reports, recent revisions announced to the data have erased any sign of stronger late-2013 growth in consumer spending (retail sales), and revisions to late-2013 data cannot be blamed on 2014 weather. Meanwhile, 2014 data to date for housing have been similarly soggy, even in regions unaffected by the Polar Vortex.

We have similar news today on factory activity in general and capital spending in particular. The factory data in general show continued flat-lining in orders and shipments for both durable and nondurable goods. In addition, within these data, orders for capital goods belie any notion that capital spending is picking up.

The chart makes this point clearly. Excluding aircraft, capital goods orders have been flat for over a year. If anything, there have been declines in recent months.

Aircraft orders are no different. These have been flat but volatile for over two years and also show recent declines. Headline durables orders data showed a February increase due to transportation equipment, led by nondefense aircraft, yet our chart shows a decline. The difference comes from nondefense aircraft parts, where orders have doubled in the last two months. For aircraft in general, as with other capital goods, corporations are replacing worn out equipment, but not expanding capacity. Contrary to the Street consensus, we do not expect a change in this pattern soon.