After a strong beginning to the year, emerging markets (EM) find themselves once more entangled in the web of US interest-rate swings and a robust US dollar (USD). This time, the rise in yields is linked to concerns over the US budget deficit and increased issuance of US Treasury (UST) bonds, which are intended to cover exceptional expenditures associated with the Inflation Reduction Act, student loan forgiveness and the shortage in capital gains tax revenues. The steepening of the UST curve and strengthening of the USD since early August, driven by concerns of a “higher-for-longer” rate environment, have raised worries about the future performance of risk assets, including EM debt.

In our view, the EM story remains compelling. First, economic data in developed markets (DM) continues to support our base case of moderating global growth and decelerating inflation, which should benefit EM fundamentals. Second, EM central banks are nearer to the end of their tightening cycles compared to their DM counterparts, which should boost demand and performance for local bonds in EM countries considered “first hikers.” Third, the possibility of the Fed pausing its rate hikes, combined with ongoing economic stabilization in China, could significantly improve EM sentiment and asset prices.

It’s worth noting that over the past five years, EM has experienced three material downturns, with two of them linked to Fed actions. Exhibit 1 highlights this trend, illustrating how EM (with the exception of the corporate segment) had tended to be more vulnerable than other fixed-income asset classes to macroeconomic factors like growth differentials, monetary policy and geopolitics.

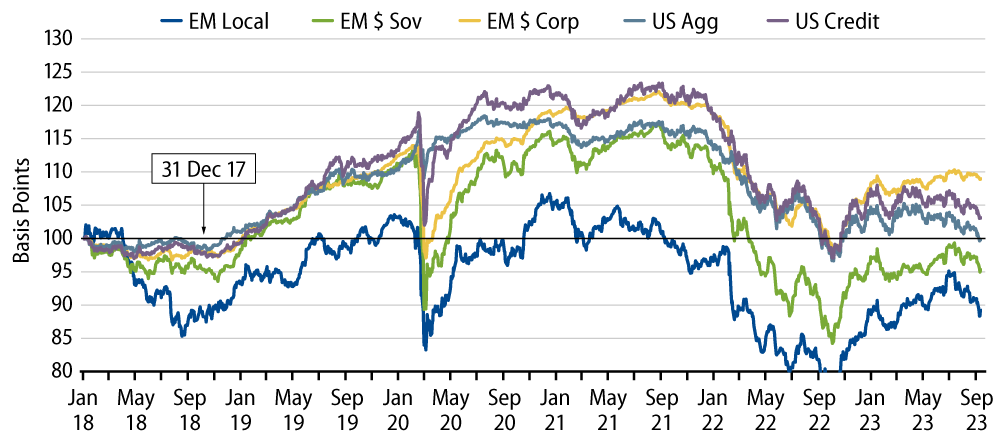

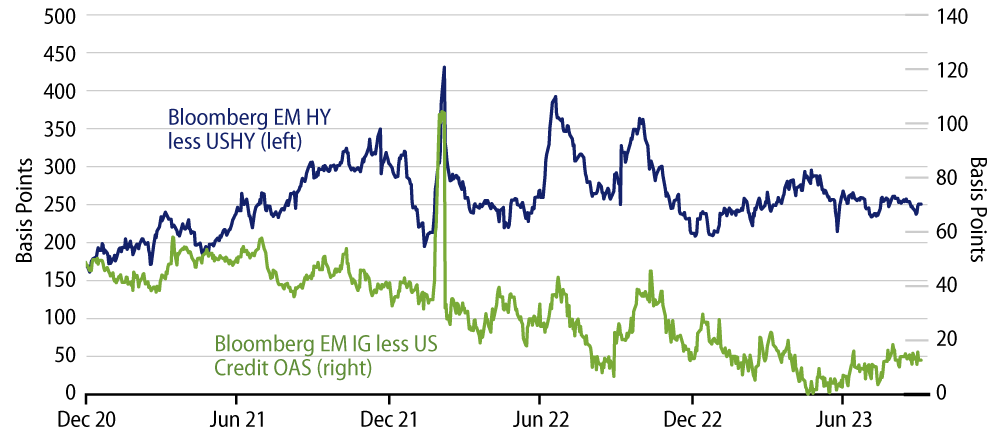

Looking forward, we acknowledge that EM is vulnerable when considering two possible extremes: continued US exceptionalism characterized by stronger growth, higher inflation and higher rates, or a protracted US recession that could lead to increased credit risk and default risk premiums. Either of these extreme scenarios could impact the outlook for EM valuations. Exhibit 2 illustrates how EM investment-grade debt is currently trading at historical narrow spreads relative to US investment-grade debt due to supply dynamics, while EM high-yield debt warrants close monitoring after substantial underperformance compared to US high-yield debt in 2022.

That stated, we currently see local markets and frontier markets as two areas within the broader EM asset class that offer an attractive combination of high carry and total return potential. Here’s a summary of our views:

EM Local Markets

Our focus is on countries with elevated real interest rates, a promising growth outlook and plans to cut rates in the near term.

Mexico (Baa2/BBB/BBB-)

- Disinflationary trends bode well for the economy; a new administration in June 2024 paves the way for more market-friendly policies.

- The central bank is expected to keep rates higher for longer, which makes the local rates carry and Mexican peso trade compelling.

India (Baa3, BBB-/BBB-)

- A strong economic story supported by robust foreign direct investment flows (on increasing friendshoring benefits) and significant foreign exchange reserves (in the top five globally).

- Local bonds and the Indian rupee are expected to outperform given attractive carry relative to peers and strong technical tailwinds associated with EM bond index inclusion.

Brazil (Ba2/BB-/BB)

- Recently upgraded by Fitch, persistent economic resilience even under the leadership of seemingly “leftist” Lula administration.

- The monetary easing cycle has started making rates attractive; meanwhile, still-high nominal and real rates are expected to support the Brazilian real.

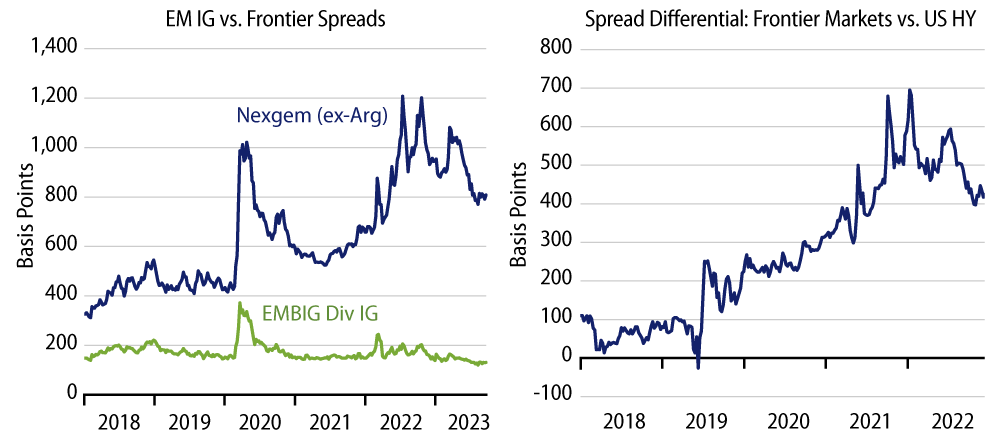

Frontier Markets

We find the risk/reward profile of frontier market debt appealing. Compared to EM investment-grade and US high-yield, valuations in this sector are notably wide from a historical perspective. This makes sense, to some extent, given frontier economies’ relatively elevated sensitivity to external financial conditions, which have presented a constraint for most of the past three years. Yet frontier markets are also a diversified subset of the broader EM universe. In many cases, this sub-segment of the market will also present investors with idiosyncratic and event-driven opportunities to reduce portfolio “beta”—in terms of the overall sensitivity to global macro factors—and capitalize on a basket of less-correlated, fundamentally driven credit inflection points. In a scenario of looser global financial conditions, we anticipate that frontier markets will stand out as key beneficiaries of this shift. Countries such as Nigeria, Ukraine, Argentina and the Dominican Republic are particularly attractive to us in this context.